Inequality, Politics and a Watershed Moment

A paradigm shift is changing the economic and financial world

We are witnessing a paradigm shift in the way Western economies are run. The change in thinking is led by the US, but will likely spill over to Europe as well. If it prevails, the economic and financial world of the next decade will be very different to what we have become accustomed to in the past.

To understand this statement, we need to first look at the current paradigm. Today, we are living in a world where the benchmark cost of capital in the US is ~0.5% and ~-0.5% in Europe. When deducting inflation, it is about -1.5% for both. It has been in negative territory for a few years now. In other words - you are paying someone to lend them your money

This makes no sense, whichever way you look at it. In 1980, that number was 12%

Money is an expression of what our work and efforts are worth. When something so central to our everyday life is distorted, the effects can be felt everywhere. What happened?

The gradual lowering of interest rates from 12% in 1980 to today’s near zero was an effort by Central Banks to generate economic growth. Whenever the economy went into recession (e.g., in ‘91, ‘02, ‘08 or last year), Central Banks responded with lowering rates

Lower rates made debt cheaper. This allowed governments, corporations and households to maintain existing debt and assume more debt in order to patch up the damage caused by recessions. This was a good thing, as it saved millions of people from personal hardship

Naturally, debt must be repaid. So once the recessions passed, all focus moved to repaying it. This reduced the funds otherwise available for consumption or investments. So after the recession, the economy grew slower than before

To stimulate an economy growing below trend, Central Banks kept rates down, instead of rising them again to pre-recession level

Over time, rates got lower and lower and debt got a lot cheaper. In fact, too cheap for the risks attached. People started using debt for things that in hindsight didn’t make any sense. Individuals levered themselves to buy subprime houses, funds levered companies 15x in buyouts, corporates in highly cyclical industries loaded up on debt to buy back stock

Whenever the next recession hit, they couldn’t repay all this debt. Governments had to bail everyone out to prevent a collapse. And governments used – guess what – more debt to pay for this

After 40 years of a continuous cycle of lower rates – more debt – lower rates etc. we have reached stratospheric levels of indebtedness while trend growth is lower than ever before. Over the same period, asset prices have steadily increased to equally stratospheric heights. This is because all financial assets are priced off of the same interest rates. As these go down, the value of assets goes up. Good for everyone who owns them, not so good for everyone else.

To make things worse for those who didn’t own assets, a concurrent dynamic played out over roughly the same time frame.

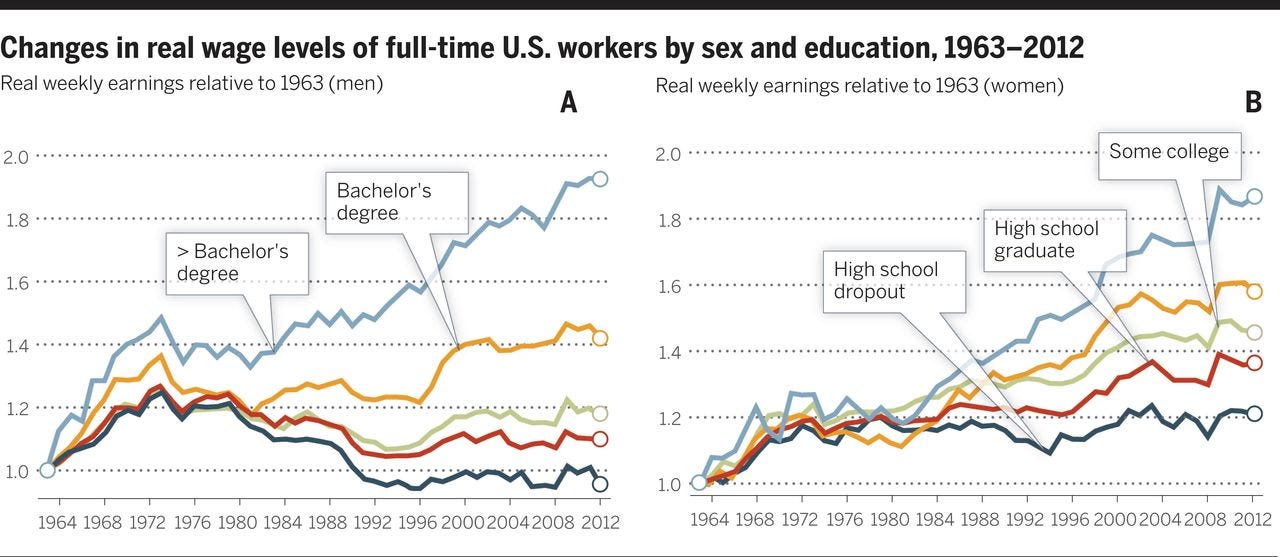

In the late 1970s China opened its economy to the West under Deng Xiaoping and in the late 1980s the Iron Curtain fell. This added 2.5 billion skilled people to the global labour force and weakened wage bargaining power for the Western middle class

As a result, median real wages in most Western countries have stagnated since. In other words, after inflation, many young people make the same money as their parents did 40 years ago

However, because asset prices have risen so much, home ownership - an achievable dream for the middle class parents’ generation - moved out of the realm of possibility

Unsurprisingly, many people aren’t happy about their stagnating lives. Yes, they have objectively improved on an absolute basis. But happiness is closely tied to relative advancement - we compare ourselves to others - be it our parents or other parts of society

On top of that, the austerity imposed by governments to pay back debt (see above) had a disproportionate effect on lower and middle classes. Just think of the school budget cuts in the UK between 2009 and 2019

This brings us to politics.

It is easy to realise that this dynamic was unhealthy. When people are unhappy, they want change, and whoever promises change will have their ear

Those who offered a break with the status quo thrived in elections. Trump promised to “drain the swamp” and became a working-class hero. Brexit promised bright new pastures and was a success in Labour strongholds. Marine Le Pen scolded the establishment and is revered in industrial northern France

Because the US doesn’t have a social safety net, the negative effects from these dynamics were felt more strongly than in Europe. So people were angrier, and a shift in thinking happened sooner

This shift was already visible in policy actions of the late Trump administration, such as the unconditional stimulus cheques and unemployment support in 2020

But when stock markets reached record highs that same year because monetary support related to the COVID-19 shock pumped up asset prices even further, the shift really gained momentum, especially as unemployment sky-rocketed at the same time

The distortions had become both glaringly obvious and unbearable to anyone who dared looking

So what is this shift? What exactly has changed?

The shift can be summarised in a few words. They are: Deficits don’t matter

For decades, government finances were run with the aim of achieving a balanced budget. Whenever debt increased after a recession, expenditure was cut afterwards to save and repay

Yes, a balanced budget is sound economic policy in a healthy economy. But with aggregate (household + corporate + government) indebtedness at levels beyond repair, it has become a hopeless endeavor to ever get rid of the debt again by cutting expenditure. A reset or restructuring would have been needed

Instead, the same cuts depressed trend growth further in a negative feedback loop, and at the same time increased social tensions

Today, austerity is in the rear-view mirror and the aim is to break out of the “low trend growth ghetto”. In light of social tensions and stagnating median real wages (above), the focus is on “inclusive growth”, in other words, growth that reaches every layer of society

Specific decisions from both sides of the aisle in the US illustrate this new direction:

The 1600 USD cheques sent to every American by the Republican Trump administration in response to the COVID-19 shock in April ‘20

Trump’s subsequent request to send another 2,000 USD to every US citizen (both can also be seen as a giant experiment in Universal Basic Income)

The Democrat Biden Administration’s 1.9tr stimulus package, including up to 7,000 USD cheques to families of four below 150k household income (at a cost of ~10% GDP)

The planned 3tr USD infrastructure programme (cost ~15% GDP)

Public support is overwhelmingly positive, with 80% in favour, irrespective of party affiliation. Congress popularity is at its highest in more than a decade. In comparison, only 40% were in favour of Obama’s stimulus plan in 2009, even though the economy was in much worse shape and the plan was half the size

Frequent comparisons are drawn to Roosevelt’s New Deal and L. B. Johnson’s Great Society, transformative efforts that also changed the economic trajectory

Politics and public support have shifted, but what about the Central Bank? After all, it was monetary policy that got us to where we are today?

US Central Bank policy has also shifted materially. Over the course of 2019, the Fed conducted a series of “Fed Listen” events, where Fed members met with the broader public, including many lower-income groups

The results from this series resulted in changes to its employment mandate. It is now seeking “inclusive employment growth” that goes beyond full employment. In order to achieve this, it has moved its inflation tolerance upwards

In general, recent communication by the Fed features wording around inequality and inclusivity much more frequently than before. The Fed is very cognizant of its role in generating the distortions discussed here

This stance also translates into action:

The Fed is keeping short-term rates low in order to support the recovery. But it has made it clear that it has no issue with letting long-term rates rise

This is important: Higher long-term rates mean lower asset prices, as assets are priced off long-term rates.

This way, the Fed can seemingly achieve both goals, support the economy with low rates on the short end, and reduce some distorting effects on inequality by allowing the long end to rise

The US government can still fund its enormous debt pile in this scenario, as the average maturity of its debt is short with 5.5 years. It can shorten the maturity further by issuing more short term debt

So both politics and monetary policy have clearly shifted. Whether good or bad, it will be transformational, but what does that mean going forward?

I will share my views on each of the below in future posts, here is a summary already:

For the US economy: GDP growth will be higher, median wages may grow again, inequality will be reduced

For the European economy: Europe has not participated in this paradigm shift yet. It is moving slowly and still stuck with the old deflationary forces. However, as the change in direction in the US becomes more visible, it will likely follow

For Asset Prices: US government debt will offer yield again. This will reverse the search for yield and drain liquidity from areas that were used as alternative store of value, e.g., real estate or long duration equities. This will be a globally-felt effect, as the USD is the world reserve currency

For Tech and VC: In a no-growth and too-much-capital world, anything with growth unsurprisingly achieved astronomical valuations. If growth comes back with less capital around, what has become a big bubble will likely deflate. However, tech will still change the world and provide more innovation than ever before

For Politics: The political debate will likely become less divisive as more inclusive growth reduces societal anxiety. Thus, the pendulum likely swings back from extreme partisanship to something more centric

For Inflation: There is no free lunch in economics. If excessive deficit spending is maintained for many years, inflationary pressures will build, and inflation will be higher than before

Great post!

Great post!