No Change in Story (Yet)

Some brief commentary on yesterday's US inflation data

The progress of US inflation is currently the most important dynamic for financial markets. With this in mind, today’s post provides some brief context on yesterday’s March US-CPI data, and whether any early signs have emerged that point to a trajectory change

A brief reminder: The question we’re trying to answer is - How persistent is the currently very high US inflation?

This is so important because inflation determines the interest rates on US government bonds. These represent the “risk-free rate”, all Western financial assets are priced off it

If inflation turns out to be persistently high, these rates will have to go much higher. This would in turn drive down the valuation of most other assets (stocks, crypto, housing etc.)

Now, the much-reported 8.5% year-on-year headline sounds shocking, but it’s not informative for our purposes. Why? Two reasons:

First, it only provides a comparison with what happened a year ago. But we want to know what is happening now. For that, we need to look at a much shorter time frame, such as month-to-month (e.g. March vs February)

Second, the headline number includes volatile categories (mainly energy or food). This could skew conclusions. With this in mind, economists focus on a “core” number that excludes these items

Now, let’s put both together and look at month-on-month core. It came in at 0.3%, or ~4% annualised. Much lower than expectations of 0.5% m-o-m, or ~6% annualised

That’s great news, so inflation is slowing, right? Unfortunately not

With the pandemic, another large category assumed the volatile characteristics of energy and food - used cars

As I had written in the last post, used car prices have rolled over in March from very elevated levels (-4% m-o-m). They represent 5% of CPI (5%*4%=0.2%). This explains the miss against expectations

Ok, so what do we need to look at?

Let’s take a quick step back - regular readers will be familiar with two important assumptions:

First: Persistent inflation is driven by an overheated labor market, where wage gains outpace productivity gains - the dreaded “price-wage spiral”

Second: Services are a much larger part of the economy than goods (75% vs 25%), and services inflation is mostly driven by higher wages

So the right metric to judge whether any dynamics have changed is the month-on-month increase in services inflation. With 0.7% or an annualised ~9%, it has not been good:

From the chart you can also see how goods inflation is generally much more volatile. Services inflation is like a big tanker, it takes time to move it, but once it moves it’s hard to stop

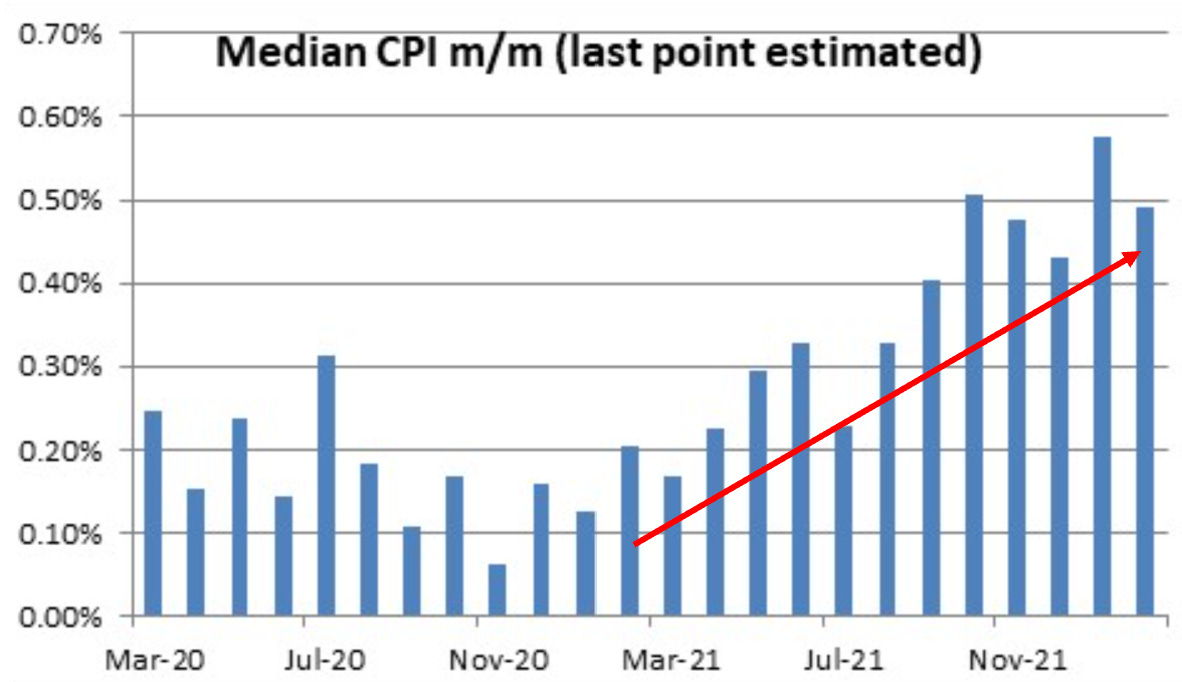

To corroborate this conclusion, let’s look at a few more ways to slice this. For example, median inflation, which removes outliers in either direction…

or let’s exclude used cars in addition to food and energy, a “super core” measure…

…all these tell the same story:

Inflation is still broad, deep and on the way up. There are no signs of deceleration, there is no respite in sight (yet)

What does this mean for markets?

I would like to add the following observations to what’s already been stated in Monday’s post:

For Europe, higher US-rates are a difficult challenge. They attract money flows out of the EURO into the US Dollar, which weakens the exchange rate. A lower EURO means more imported inflation (e.g. most commodities are priced in USD)

To this, the ECB would need to respond with higher interest rates. But Southern Europe has a long history of prioritising inflation over government budget constraints, and with Christine Lagarde at the helm they may be more dominant within the ECB. Likely, the ECB will be slow and hesitant to follow, so expect a lower EURO

I don’t even want to begin to think what higher rates would mean for German real estate, which shows many bubble characteristics. Its mortgage market is also less regulated than e.g. the UK or the US, with many instances of >100% LTV loans. Residential real estate loans represent 35% of German bank lending

Further, I had highlighted in Monday’s post how high inflation likely forces a shift in consumer spending from the indulgent to the necessary. This would express itself in a slowdown for durable goods demand

In this vein, the following headline from yesterday is not a surprise:

In particular, US consumers plan the biggest cuts on “eating out and impulse purchases, along with driving and experiences like concerts and sports” (please see my last post for comments on Luxury)

Yesterday, CarMax, a big US car dealership fell 10% on earnings. It stated declining consumer confidence and affordability as reasons for a slowdown in demand

At this point, I want to repeat my “warning” on the FANGs as perceived safe havens. In my view, the market underappreciates the earnings risk and direct or indirect exposure to discretionary spend (iphones, e-commerce paid search etc)

To conclude, while a decline in durable goods demand will obviously have an impact on goods inflation, as we’ve seen with the move in used car prices, this is a disorderly process where any respite in inflation is driven by crushed consumers

Still from there, it is still a very long chain for goods disinflation to translate first to slower manufacturing orders to changed staffing plans and then finally to a looser labor market, which is unfortunately likely needed to break the price-wage spiral