A New Seriousness

What the Shanghai lockdown and German dithering on Russian gas have in common

Over the last weeks, more signs emerged that we’re likely past the peak of the current economic cycle. Retail inventories are up sharply while consumers cut back discretionary spending in light of soaring energy costs. Both reduces durable goods demand. While this might provide short-term relief for some commodities, freight costs and other supply bottlenecks, the structural composition of Western economies has been altered. A return to pre-2021 settings seems unlikely, even in what appears the first innings of the next downcycle

After a decade of abundance in labor, commodities and capital, policy decisions and inflation in their wake have created scarcity in all three. Labor markets are overheated, commodity inventories decimated and the cost of capital up as central banks raise rates to fight inflation. More so, inflation has empowered commodity-rich nations, many of them outright hostile to the Western model. Taken together, this forces a different mentality in economic and political decision-making. After a period of anything-goes, a New Seriousness is needed, with profound consequences for capital allocation

This post walks through the difficult choices that lie ahead in national security, energy & climate and government finances and how they will be mirrored in capital allocation. It concludes as usual with an outlook on current markets

NATIONAL SECURITY – Economic Growth or Freedom?

With images on social media in real-time, the massacre of Bucha was a seminal event for the Western public1

It puts the resolve of “Never Again” to the test that rightfully has been indoctrinated onto generations of Europeans after the Second World War. Not only was Ukraine the theatre of some of the worst NS atrocities during WWII, the Bucha events also share their date with the Katyn massacre in 1940, where 22,000 Polish officers and intelligentsia were killed by Soviet NKVD

As the conflict escalates, the role of Germany moves to the center of attention. With new atrocities reported on a daily basis, how much longer can Germany - every day - wire 400m EUR to Russia for its natural gas?

The German industry paints a dark picture in case of a cut-off. The CEO of chemicals giant BASF gave an extensive interview, predicting the country’s economic destruction, including mass unemployment

However, not only BASF, but much of the German industrial base has essentially been freeriding on geopolitics, with an unsustainable energy source, an artificially low EURO exchange rate and interest rates much lower than for a stand-alone Germany. One might argue it has overearned for years

This will of course be little consolation to anyone laid off. On the other hand, extreme times have provoked human ingenuity, an the effect from a cut-off might be less bad than feared. Either way, Germany now faces the responsibility of deciding between financing Putin’s war, or hurting its own economy and workers

But this responsibility goes beyond German borders. With global grain markets squeezed, the consequences of Putin’s attack are now felt around the world

Lebanon has run out of wheat. Russia is blocking Ukrainian wheat shipments to Egypt. Is this the genesis of the next European refugee crisis?

Food-inflation related riots broke out in Sri Lanka and Peru. All logic dictates that this is the beginning rather than the end of such events

This is not the only noteworthy story. Moving on to China, the Shanghai lockdown has taken a draconian turn

As previously discussed here, some serious policy mistakes such as the refusal to endorse Western vaccines for political reasons have left China exposed to the highly contagious Omicron BA.2 variant

To prevent cases in Shanghai from spiralling out of control, the government has resorted to truly draconian measures that restricted residents’ movement in an unprecedent way, and lead to famine (!) in the 28-million metropolis

The situation in Shanghai is dystopian

Drones hover above to observe and tell residents to stay inside. QR-codes regulate mobility, families are separated from their children and covid-camps resemble prisons

Yet, the lockdown seems futile and cases keep going up. Unsurprisingly - we know that the virus was transmitted even across corridors in a quarantine hotel in Hong Kong. Shanghai Citizens are required a daily test, just to stand in line for that seems sufficient to get infected

More cases emerge around the country, such as in Guangzhou this morning

China’s economy has many serious imbalances that have been glossed over to maintain economic growth

In addition to the Evergrande crisis, the Omicron outbreaks, the Ukraine war and, as mentioned, a slowing durable goods environment present enormous challenges to growth

The obvious response would be to stimulate the economy with rate cuts and liquidity measures. But global commodity strains put upward pressure on Chinese inflation (see PPI today), which limits the ability to do so

China is probably in its most vulnerable position in decades. Looking at Russia’s example, this is not a good thing. Nationalist tendencies and outward aggression likely increase as a result

The world has become a more dangerous and volatile place. Costly decision that favor long-term ideological goals at potentially high short-term economic cost may be required

ENERGY – Secure the Climate or Secure Energy Supply?

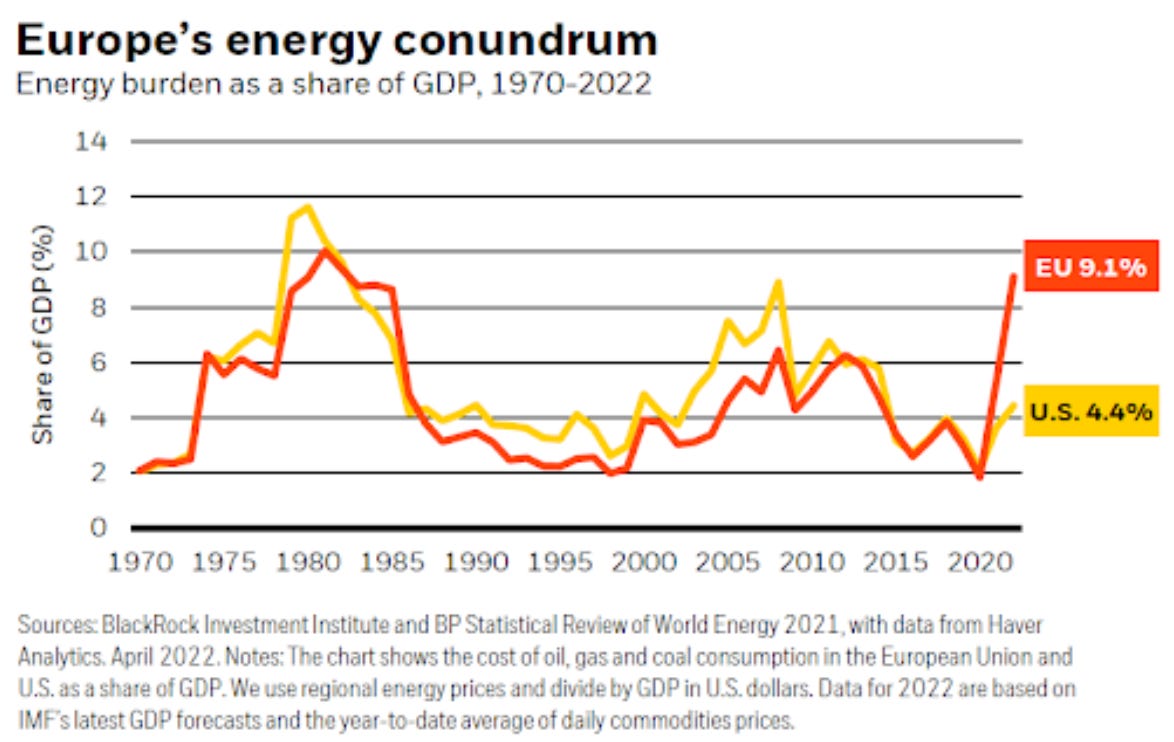

As discussed in “The ESG Time Bomb”, the past decade provided an illusion of easy solutions to the tension between energy supplies and climate change

Europe spearheaded ESG policies and indeed cut much carbon emissions, which was great for the planet and a role model to others. But as most adjustments were made on the supply side (=forcing companies to become “cleaner”) instead of the demand side (= people consuming less), most emissions were outsourced rather than truly erased2

The consequence is, as we know, a stagflationary energy price shock as last seen in the 1970s

It not only Europe, but also the US who took paradoxical decisions

There is plenty of oil in Canada. To get more of it to the US, upgrades to infrastructure are needed, with the Keystone pipeline at the center and a volume of ~450k barrels/day. Keystone was abandoned in 2021 on environmental concerns, both on the pipeline itself and the fact that much of Canada’s oil originates from oil sands from which it is extracted in a messy and polluting way

However, over the current energy crunch, the US administration has opened the door again for Venezuela’s corrupt regime. Many US states have provided fuel subsidies. There are few efforts to reduce oil demand

The negative PR for oil & gas has lead to a record-low number of people working in, or interesting in working in that industry. But again, oil demand did not decline. Now the administration wants its domestic suppliers to increase production, but there is not enough staff to do so

Energy policy around the world is full of these paradoxical decisions, with the common thread the avoidance of hard choices. Meanwhile, climate change hasn’t gone away

Both Antartica and the Artcis have undergone aberrant heat waves this Spring, with temperatures 30-40 degrees warmer than seasonal average. Australia has seen both record heat and record rain since the beginning of the year

The tension between climate change and energy security will require costly decisions, with the most obvious way seemingly the reduction of demand

GOVERNMENT- Deficit Spending, Tax Increases or Both?

After the 2008 financial crisis and the 2011/12 Euro crisis, governments spent too little, practised austerity and exacerbated deflationary tendencies. The recognition of these mistakes ushered in a different, more spendthrift mindset when COVID-19 hit

It is no coincidence that Stephanie Kelton’s MMT bible “The Deficit Myth”, (which as per the title declared the irrelevance of government deficits) was published in June 2020, the multi-decade low for US interest rates

While MMT represents the extreme version, the Western government finance debate is still very much influenced by this point of view

COVID-19 has created many social issues, from food, fuel and rent inflation to decaying infrastructure and gaps in education. There are also always elections, such as the midterms in the US this Fall. The temptation is huge to spend on debt, it’s the path of least resistance

However, in an inflationary world, government deficits contribute to more inflation. Deficits are by definition debt-funded, and debt is newly created money

But when there is literally not enough stuff around, government projects run into serious challenges:

Last month, a Italian €163m tender for a bridge over the river Tiber found no takers, as construction companies refused to assume the risk of rising steel prices

Germany has pledge a €100bn package to increase its defence capabilities. This will involve a lot of basic materials and manufacturing, where will it be sourced from?

Governments will have to be much more mindful with their spending, separating the necessary from the unnecessary

Take the extension of student loan forgiveness in the US as an example. It sounds like a good idea, but in reality is a $100bn stimulus to higher income households. Is this really what’s needed now? Could the $100bn not be spent in a better way, on infrastructure, schools or healthcare?

The most obvious way to keep necessary government expenditure from being inflationary is higher taxes. My guess would be that we’ll see more of that in the next few years

It seems unlikely that governments will be able to resort to excessive deficit-spending much longer. They will either have to accept more inflation, cut back expenditure or raise taxes

CAPITAL ALLOCATION - Dreams or Needs?

All of the above sums up to an environment that is more volatile and carries more risks. For businesses and their fragile global supply chains, this means to move from Just in time to Just in case, with the following consequences:

More capex: Securing materials and providing buffers between production steps requires more plants, machinery and equipment. And indeed, capex now runs at much higher levels than in recent years

More inventory: Resilience to shocks requires higher inventory levels. This provides for a more volatile business environment as inventories amplify boom and bust cycles. And yes, inventories have gone up since 2019

Lower margins: Corporate margins have expanded for two decades, in logstep with waning labor bargaining power, consolidation and deflationary input costs. Firming up supply chains will pressure margins, as will higher labor costs and structurally higher commodity prices

A volatile environment shaped by higher capex, higher inventory and resource scarcity shifts excess returns to the “necessary”, in contrast to the “dreams” of the past years

Let’s take the electric vehicle industry as an example

At the current pace, copper inventories will run out over the next few years. Most copper mines are old, some even centuries’ old and it takes 10-15 years to build a new one. Yet, the transition to electric vehicles will lead to significantly higher copper demand going forward3

As long as EV-concept companies such as Rivian or Lucid still carry $35bn+ market caps with no revenue and no proven cost structure, higher returns will likely be found in the raw materials part of the value chain, while the “concept part” likely continues to deflate

But importantly, this is not a statement against Tech. Many new solutions may emerge that help what is needed. They’ll just likely be different to what dominated the most recent paradigm

What does this mean for markets?

The context of this New Seriousness has concrete effects on markets today. In particular, consumer behavior likely to shift towards the necessary after a period of more indulgent spending. This will likely be most visible in durable goods, where a built-up of inventories coincides with weaker demand

I had mentioned Trucking in my last post as a short. The sector is hyper-cyclical and most exposed to inventory changes. It has fallen off a cliff since, so the risk-reward is more balanced now, but I don’t think it’s done yet (KNX, JBHT, R, WERN)

Luxury seems an obvious industry facing a more difficult backdrop now. With the average energy bill going up >50%, asset prices going down and war headlines everyday, this seems not a time for discretionary spending; even if you can afford it, the mood is different. Add to that China’s woes, and purchases that have likely been brought forward last year. This is a high multiple sector, so higher interest rates have a negative effect here, too (MC FP, KER FP, RMS FP, BC IM, SFER IM)

Hospitality may see similar effects, while pent-up demand from COVID-19 works the other direction. However, it is noticeable that US hotel visits are down last week vs 2019, and Trivago also reported slightly lower demand for Europe

I believe the risk/reward in Oil/Commodities to be more balanced now and possibly even skewed to the downside near-term, in particular in oil. The US SPR release of 1mbbl/day for 180 days is huge, while most of Russia’s oil still finds its way into the market. In general, if the peak of the economic cycle is in, most of the gains have likely been made

With regards to US Tech, I had outlined since late last year how the Fed’s quest to fight inflation likely weighs on high-duration assets such as the Nasdaq. I also highlighted a short term bottom from where a bounce was likely. Then, in the last two posts, I called for the Nasdaq to resume its downward trend

As discussed, the recent up-move in stocks had loosened financial conditions. Thus, the market challenged the Fed, which wants them to tighten, and Fed has responded. Fed Vice-Chair Lael Brainard gave a very hawkish speech, and the FOMC guided to a balance sheet run-off capped at 95bn USD, a significantly higher than expected number

Further, the earnings risk in US Large Caps in my view remains underappreciated. The market extrapolates from earnings performance during COVID-19, which was a 1-month recession followed by an unprecedent spending boom. Iphones for example are expensive luxury items, I don’t think the same will repeat

Again, the Fed follows politics. The most pressing issue for most Americans is inflation, so politics wants inflation down, so the Fed fights inflation. With this in mind, I’m tracking the progress of various inflation indicators closely

Housing is the biggest part of the supply side of inflation, and higher interest rates have doubled the cost of mortgages vs 2021. Inventory is up sharply in some markets such as Denver or Phoenix, albeit from depressed levels. However, rents accelerated again to 0.8% m-o-m in March (~10% annualised)

Used car prices rolled over, with the Manheim index down 4% in March. This will be a ~0.25pct drag on March month-on-month CPI. There a plenty of reports of full dealerships and lack of demand (again, is this a surprise at these prices, in this environment?)

But the key metrics to watch for inflation, wages and employment, are still firmly overheated. The vacancies-to-unemployed ratio has reached unprecedent tightness and wages are again up 6% in March, so I don’t expect a relief in core inflation (ex. energy, food, cars)

One has to be careful to judge war reporting, and there have been previous examples where misreporting of war crimes was used for propaganda purposes, including by the West (cf. this story during the 1990 Kuwait conflict). There have also been reports of violations from the Ukrainian side. I’ve tried to verify proceedings around Bucha as much as possible, and several indications give me enough reason to believe that much of it did happen as reported, in particular Russian army radio intercepted by the German secret service, and detailed eyewitness reporting from sources I deem credible such as the WSJ or economist

E.g. by European companies selling “dirty” assets to companies abroad, or foreign production of goods destined for Europe

Cars represent ~25% of global copper demand, and EVs consume 5-6x more copper than traditional ICE vehicles