Be Fearful When Others Are Greedy

Latest data suggests the Fed is likely right to worry about growth

In recent posts I outlined a constructive stance on the economy and markets, with the key risk corporate margins as they could get compressed by slower top line growth while their cost base still grows

Latest data has lead me to re-asses that risk and assign a higher weight to it. Paired with very frothy markets that are now driven by retail mania (cf. Solana coin +100% in two weeks), I’ve accordingly moved to a more cautious stance

So what is this about?

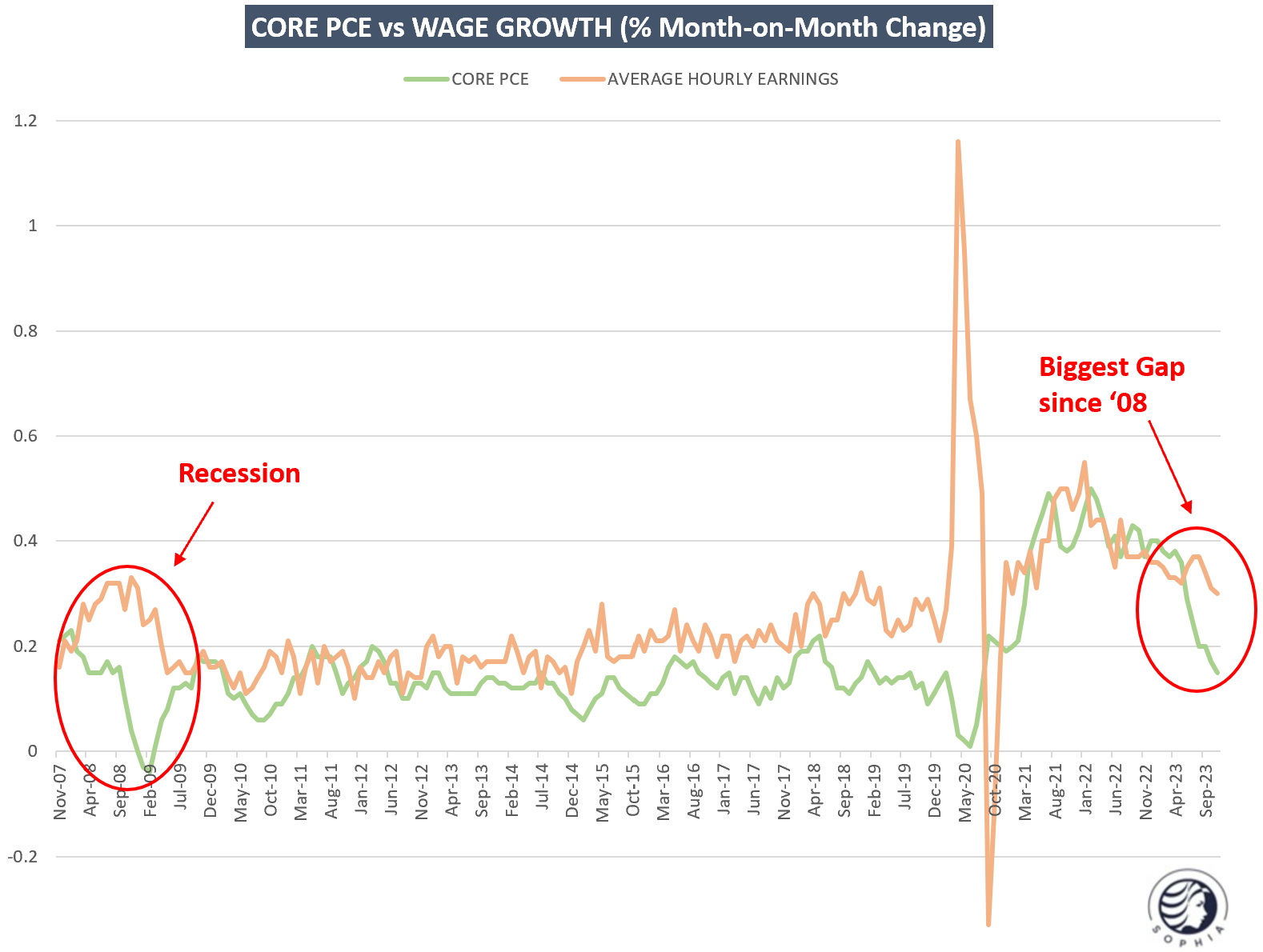

The Friday before Christmas the Fed’s favorite inflation measure was released, a metric called “Core PCE”. It aims to provide a more comprehensive measure than the broadly know Consumer Price Infation (“CPI”). Core PCE can be perceived as a good proxy for the aggregate pricing of all corporate products (excl. energy) - it gives us a good window into corporate revenue growth

The November reading for Core PCE came in “ice-cold”, at 0.1% month-on-month. More so, if we look at the 3-month or 6-month average, it has now been running below the Fed’s 2% inflation target for some time, with a strong downward tendency

Why is this important? Core PCE is a mirror image of corporate revenue growth , and tells us that has stalled. Corporate cost growth on the other hand has not stalled. In particular labor costs are still running at a very brisk rate

From below chart the consequence is easily spotted. If these dynamics persists, costs will keep growing while revenues fall flat. The result is a corporate margin crush that historically has been responded to with cost and job cuts

Indeed, we see some early evidence of this in the earnings of Fedex and Nike, both bellwether stocks that report off-cycle. In each case, late last week they confirmed the margin crunch dynamics I outlined above

I’ve been critical of the Fed’s early dovish pivot. However, in light of recent data I have to acknowledge the risk rapid disinflation presents via the corporate margin channel is higher than previously thought

Further, while interest rates have come down across the yield curve, there is still no pick up at all in bank lending. In absence of QE, and aside of the wealth effect of higher assets prices, bank lending growth would be the key vector to stimulate the economy and provide it with new money. Why are corporates not borrowing, even as rates come down?

The choice is not an easy one for the Fed. As discussed, lower rates instantaneously send US house prices higher. With some lag, rent inflation likely follows

It remains to be seen to what degree a reinvigorated housing market can stimulate the remainder of the economy. An ailing housing market in ‘22/’23 did not slow economic growth, so the inverse could also apply going forward

Equally, rates may need to be cut quite heavily to incite credit growth, which especially on the consumer side may not be in demand. Everyone refinanced their mortgages at secularly low rates during Covid-19, so that channel has been used up

At the same time, easy money policies may bring back higher commodity prices, as the goods economy has destocked, inventories across the global value chain are now low and investors rush into real assets

Finally, I do note that Wall Street’s biggest bear, Morgan Stanley’s Mike Wilson, has thrown in the towel last week and pivoted to the bullish side, a behavioral signal that tells me to pay much more attention to downside risks from here

Keeping with the theme of Reflexivity, economic downside risk are likely much higher when everyone dismisses them, as the collective forces to work against them are weakened

Conclusion:

Recent core PCE data and corporate results suggest there is more merit to the Fed’s worry about growth and employment than commonly thought

Should these worries materialise further in the coming weeks, the Fed may be in a tricky spot, as cutting rates aggressively could stoke house- and commodity price inflation, while the stimulative effects especially on the consumer side may be limited

Wall Street has collectively given up on downside risks, telling us that now may be the time to pay more attention to them

What does this mean for markets?

The following section is for professional investors only. It reflects my own views in a strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please see the disclaimer at the bottom for more details and always note, I may be entirely wrong and/or may change my mind at any time. This is not investment advice, please do your own due diligence

In light of these developments, I have moved to a market neutral stance, selling the racier parts of the book in high beta and unprofitable Tech while adding index shorts to the existing commodity long exposure

I am aware that possible economic slowdowns are typically not an environment where commodities thrive. But positioning across the space remains very washed out, while this economic cycle has defied historic precedent

We could see a commodity price recovery as destocking abates and lower financing cost make it easier to carry currently depleted inventory, while at the same time economic growth continues to slow. Basically the inverse of the past year, when the US economy grew strongly while the goods economy languished

Finally, I see plenty of very bullish 2024 S&P 500 targets go around, with the reasoning anchored in an overheating economy amidst a fiscal dominance regime

Equity markets are currently in an advanced mania stage, which often comes with lofty price targets (“Dow 36’000”, “Bitcoin $150’000” headlines etc.). It is impossible to time its progression, but the proverbial “rug pull” risk is now very high, and could bring with it some nasty and sudden declines. I bought some February put spreads to play for said risk. As always, I could be wrong, and the advance could just continue unabated

I believe that that for now the trajectory of corporate profitability suggests a very different path to the “crash up” scenario of Emerging Markets fiscal dominance. Next year may more likely follow the typical re-election year since 1956, which is essentially chop until the presidential election passes

As always, I remain open minded about any outcome and will continue to listen closely to the market and incoming data for any further clues

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

It is quite curious to me that Powell pivoted so hard given the absence of data indicating the economy is slowing rapidly. while you make an excellent point regarding corporate margins, I fear that is a level of thinking that exceeds the central bank's capacity, or certainly is absent from their reaction function.

FWIW, and that's probably not much, I see H1 of 2024 as a continuation of the current rally as the market continues to buy with abandon, especially if inflation rates continue to slide, however, unlike you, I am in the camp of sticky inflation, where housing prices writ large remain supported, especially if the Fed were to cut, and as such, my greater fear is more of a stagflationary environment in H2 and in 2025 as inflation remains well above the 2% target but growth slides back <1%. in that scenario, I think the rug pull happens in late summer or early autumn and will be quite ugly for many, not least for Biden as it will weigh further on his reelection opportunities.

Ding ding ding. Inflation was holding lots of things together, including corporate profits.

Nice write up, though regarding "lower rates instantaneously send US house prices higher." Tell me what you think about this possibility. Lower rates unleashes existing home inventory, on top of near record spec new builds, at the same time that the lower rates (a sign of a slowing economy) indicates a heightened credit risk re:borrowers. So, could lower rates send home prices lower?