Crosscurrents

Opposing forces are at work within the US economy. How it likely resolves and what it means for markets

For anyone out for Labor Day I recommend last week’s post “On Reflexivity” which details my framework, it’s been one of my most-read pieces so far

Moving on to present matters, this week’s post checks in on the US economy, where two crosscurrents are presently at work to keep it in a delicate equilibrium. I review either, draw a synthesis and relate it to the rise of US long-term treasury rates, as laid out in “A Warning”

As always, the post concludes with my current views on markets

The most notable recent development in the US economy is the softening of the labor market. Let’s look at some data:

To start, Job openings are declining rather rapidly now, albeit from a very elevated level…

… the rate at which people quit is now back to pre-Covid levels…

NB: This decent lead indicator implies lower wage growth in the coming months, albeit from again still very elevated levels1

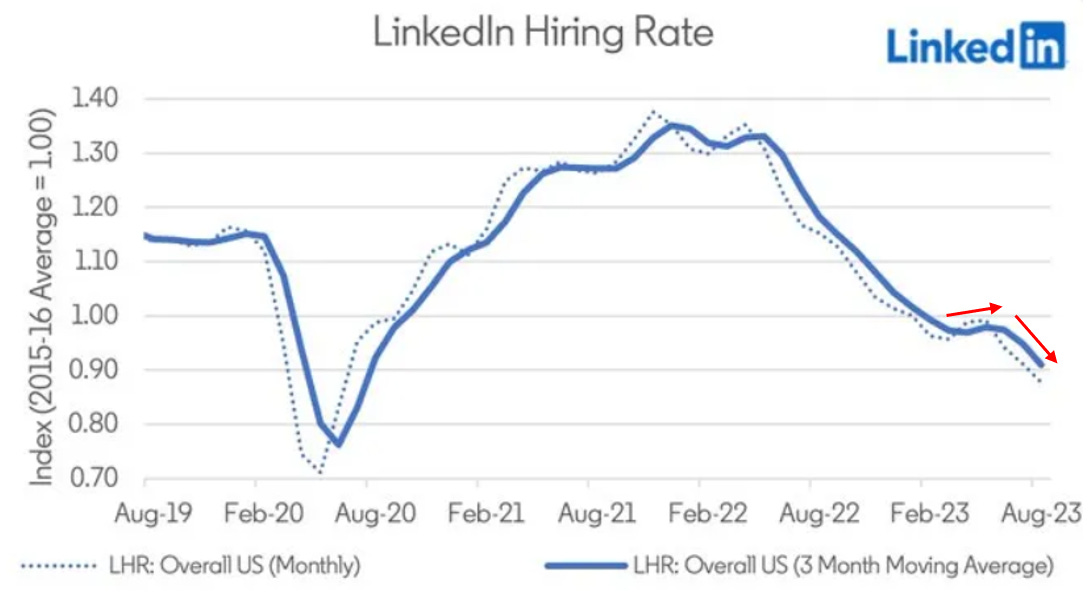

… LinkedIn, which tracks high-quality near term data on the job market, also notices sequential deceleration…

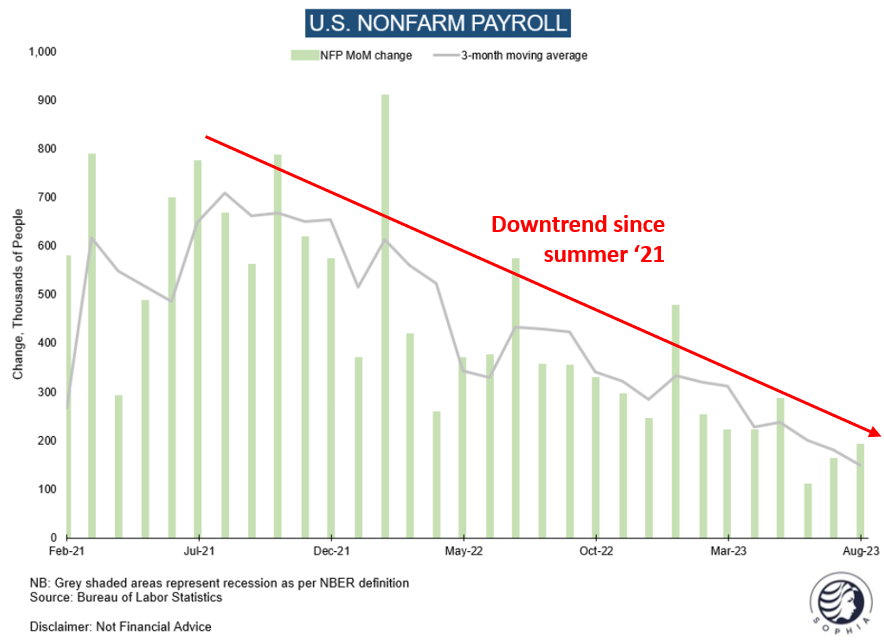

… and the downward trend is further pretty obvious in the lowest quality (as most revision-prone), yet most widely reported labor market metric - Non-Farm Payrolls

Unsurprisingly, Americans are starting to notice. In the Conference Board Consumer Confidence Survey, the share of respondents who perceive “Jobs as hard to get” vs “plentiful” has visibly risen:

Summary:

The US labor market is not weak, but it is definitely weakening. It is positive that it has moved from overheated to balanced. However, we are not interested where the puck is now, but where it’s going. And the trend in all these charts is down

Unless a change in trend occurs, unemployment is bound to eventually rise, probably around 1Q or 2Q ‘24

Now, are there any reasons for this trend to change in the coming months? Let’s look at the drivers currently affecting the US economy

On the positive side:

The goods economy continues to show signs of turning…

… more so, as inflation declines, with wage growth still high, real income is improving, so Americans have more money to spend…

… while the various stimulus programs such as the Inflation Reduction Act (IRA) continue to boost domestic construction

On the negative side:

The Residential Housing rebound seems to have come to an end…

… and automobile production, which took the longest to solve Covid supply bottlenecks, has recovered to its pre-Covid level, which means it won’t provide the same GDP tailwind going forward…

… and while the IRA works as expansive force, other elements of the fiscal impulse likely will be much more tame next year, such as lower COLA adjustments, no repeat of the January ‘23 tax bracket boost and less state spending

How will these crosscurrents unfold? This is my read:

The goods economy rebound likely continues as we’ve worked through the Covid-19 whiplash (Goods spending surges → Goods demand depressed → now back to normal). This is a positive, even if the big automobile component likely follows a different trajectory

The fiscal impulse is likely balanced, with the IRA and higher interest payments to the private sector on one side, and the various other outlined aspects (COLAs, state spending) on the other side

Looking at housing and real income, it gets more complicated. Coming back to the theme of Reflexivity, we likely see important feedback mechanisms at work

With higher real income, consumers likely have the cash to spend, the question whether they do it is a matter of confidence. If the job market continues to weaken, this confidence will be negatively impacted (see Conference Board Survey above). If consumers spend less, a weakening job market is more likely. Etc. and vice versa

So what will decide how the crosscurrents break, which side gets stronger in this confidence game?

The deciding variable is likely the US government deficit, and through it long-term bond yields. But how?

As we know, the US is running a record deficit outside of wartime and crisis

Government deficit spending has offered tremendous support to the economy this year, very likely keeping it from falling into recession as the hangover from the Covid spend-fest set in

Now, in a simplified way, that money has been spent already, but it hasn’t been financed yet, as the Treasury used the $900bn in its General Account from Q3 ‘22 to Q2 ‘23 instead of issuing new debt.2 This has now been used up (see detailed elaboration in “A Free Lunch?”)

More so, historically, a high deficit was usually financed by the Fed (ie by the printing press), justified by - exactly - wartime or crisis (e.g. WWII, GFC, Covid, etc). But now the Fed is doing the opposite, it is doing QT, so the private sector has to finance it

As a result, long-term yields are going up - the demand for government debt needs to be incentivised, something I had described in “A Warning” recently. It is practically certain that these higher yields will weigh on the economy, the only question is the level and timeline. Why is that?

Simply speaking, with its enormous debt issuance, the government puts itself in competition for capital with the private sector. So over time, it crowds out private sector projects as investors choose to allocate to government debt

Sure, in the long run, the government also spends that money, but usually less efficiently than the private sector, which is why high deficits are generally perceived as inflationary and a feature typical for many Emerging Markets

So what is the level at which damage will occur, and how quickly will rates get to that level?

I have no definitive answer as to where that level lies. I don’t think anyone knows with certainty. However, I do not think it is far off - as outlined above, the economy is in a delicate balance, so it won’t take much to tip it over

One can backsolve where demand was found in a similar growth context (e.g. 2003/4), but the deficit and thus issuance at the time wasn’t nearly as large. Another way to argue would be to require a positive term premium, or that rates should match nominal GDP growth. All this points to >4.5-5.0 for the 10-Year and somewhat higher for the 30-Year

Given the huge issuance, I see no reason for bonds to be properly bid until either economic data turns bad, or until the government intervenes, or both. Right or wrong, the market perceives the supply as an issue, and the high deficit as indicative of an inflationary future. So rates likely just keep going until there is reason to change the narrative

Whenever the level is reached that shows that the economy is harmed by higher yields, the US government will likely act to provide support. This could be via allowing banks to hold more bonds, by raising the issue composition in favor of even more bills, or even more dramatic measures such as Yield Curve Control

Conclusion:

The US labor market is not weak, but it is weakening. At the current pace, unemployment likely rises in Q1 or Q2 ‘24

Under normal circumstances, a rebounding goods economy, the IRA and real income gains could create the conditions necessary for a trend change in the labor market

However, a new weight is imposed on the economy - higher long-term yields caused by treasury issuance to finance the deficit. This likely, eventually tilts the balance in favor of negative drivers

When the inflection point for yields is reached is unknown. It is likely not too far off, as the economy is at a crossroads and not much is needed to push it in one direction

When that moment arrives, the US will likely need to decide between price stability and unemployment. I believe the market will force it to choose the latter, accept a higher inflation target and engage in measures that suppress long-term yields

What does this mean for markets?

The following section is for professional investors only. It reflects my own views in a strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please see the disclaimer at the bottom for more details and always note, I may be entirely wrong, may change my mind at any time and this is not investment advice, please do your own due diligence

How does the above all fit together?

I believe that as long as higher bond yields don’t yet cause economic harm (which would be visible in the data), the stock market will likely assume the positive side wins. In that case, earnings estimates likely drift further upwards and equities do well, or at least better than bonds

I expect us to still stay in this regime for a some time longer, where bond yields spike → equities dip → bonds steady → equities rally

But eventually, economic data will show weakness, then the relationship changes. Bonds should then do better than equities (though not great), as earnings re-rate down while bonds are bid as growth expectations decline. When this inflection point comes is uncertain. I would expect the moves to gradually become more violent to the up- and downside until the tipping point is reached

As I’ve laid out last week in detail, for investments I mainly look to fade the crowd at extremes, and I would expect several more extreme moments to crystallise across asset classes in the coming months. This is why I am running a high cash position now, to be able to act

Until then, I am content with the big dislocation I see in China, where I managed to bottom ticked the recent sell-off. More measures have been introduced since the lows. Child care credit has been retroactively expanded, amounting to a de-facto stimulus cheque for families. Housing traffic has jumped in large cities following looser mortgage rules and Manufacturing PMIs appear to have turned. I see local parallels with 2009 or the Covid-lows, where everyone was convinced the economy would remain depressed for years, and then it turned out differently

As laid out last week, China Tech remains my largest position right now, in addition to some US Regional Banks, some Energy and cash

Some further thoughts

Real rates - I had mentioned TIPS and Gold last week and how both look attractive, with real rates at 15-year highs. I have held back so far, as long-term real rates currently act like a high-beta version of long-term nominal rates, and I expect the high for the latter to still not to be in. I am waiting for that to happen before I’d do anything in this area

US Dollar - With very high real rates, a better economy than Europe, an adverse US liquidity context and the rates differential likely growing, the Greenback should continue to be bid

Finally, there are some stunning and encouraging developments in Healthcare, which may be one of the most promising areas for AI-application. I hope to share more on this soon

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

The AtlantaFed Wage Growth Tracker which does not suffer from compositional issues still runs at 5.7%. Wage growth is also still very high for low income earners which have the highest propensity to spend

The debt ceiling, T-bill issuance and the RRP have played and still play a large role, but again, this is simplified, for details please see “A Free Lunch?”

Excellent explanation and analysis! Thanks for sharing this.