Don't Fight the Fed

Why most asset prices will likely fall from here

Over the past decade in financial markets, I’ve observed a trend that became more pronounced every year. As a consequence of the improved flow of information and increasing amounts of capital, most investment strategies (hedge funds, private equity, venture capital etc.) would become ever more efficient. With more efficiency, the individual “alpha” would shrink, and the role of a particular financial actor would become ever more important in determining the success of any of these strategies - the US Federal Reserve.

So, I’ve spent the best part of the past year understanding how the Fed’s decisions on interest rates and liquidity would affect markets and the economy. My posts are a documentation of this work. I had written on the risks of rising inflation as early as April and September last year, on the emerging bubble in Tech and VC in April and again December, and how European banks and commodities would outperform in this environment in October. In my last post, I highlighted a significant recession risk for 2022 (unfortunately!).

Today’s post is a continuation of this work. The Fed is the biggest single driver for most asset classes around the globe. Now, in its convoluted language and process, it is very loudly telling us it wants asset prices to fall.

I lay out the details below

Recent data confirms an accelerating, highly inflationary environment

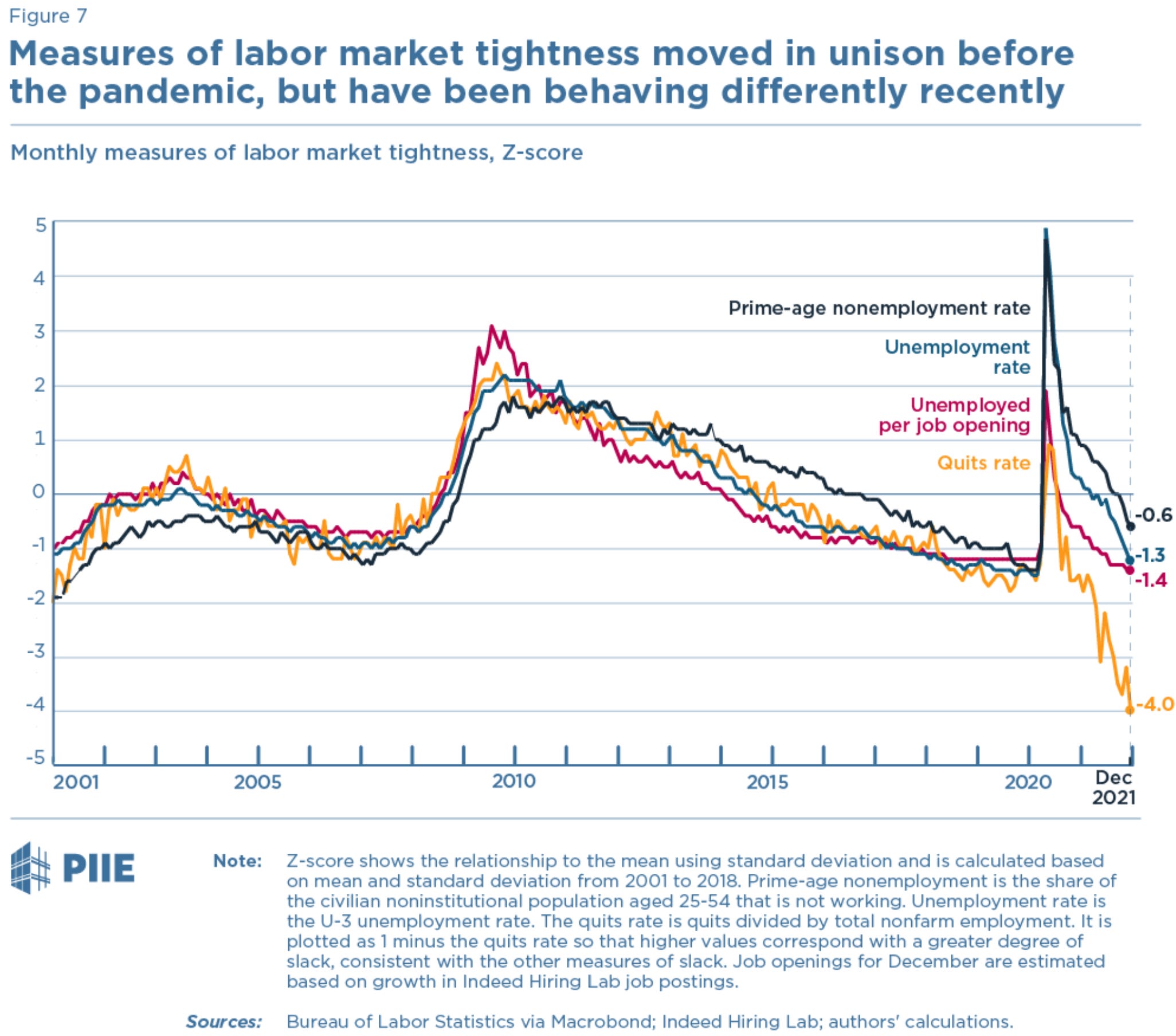

Last Friday’s US employment data showed the price-wage spiral I mentioned in my last post in full swing. The unemployment rate hit 3.9% which is a cycle low and the vacancies-to-unemployment ratio is now the highest on record. Wages grew at an annualised 7-8% and accelerated

The rate at which people are quitting their jobs is off the charts. The “quits-rate” is also the best predictor of subsequent wage inflation. This is because in absence of broad union contracts (like the “Tarifvertrag” in Germany) Americans “negotiate” higher wages by switching jobs

Despite the extraordinary demand, only 199k new jobs were created (vs >600k expected). The economy has literally run out of workers. And higher wages may sounds like a good thing, but in a price-wage spiral all these gains are consumed by inflation

There is also no end in sight for many goods bottlenecks, e.g. for cars and chips. Either way, services are a much bigger part of economy, and they are driven by these escalating labor costs. For every 1% rise in service prices, goods prices would have to fall by 5% to keep inflation even

The Fed has recognised the problem and pivoted from its ultra-accommodative policies to a stance that is firmly committed to fighting inflation

The pivotal moment was President Biden’s speech in November declaring the fight against inflation his number 1 priority (see post from Nov 17th)

Fed Chair Jerome Powell agrees, at a news conference last month he declared that “there’s a real risk now … that inflation may be more persistent and…the risk of higher inflation becoming entrenched has increased”.

More so, several dovish Fed members have pivoted and now regard inflation as the main problem (e.g. Mary Daly, Neel Kashkari)

Political dynamics were also at play. Independent-minded Democrat Senator Joe Manchin from West Virgina only agreed to support Jerome Powell’s re-election as Fed Chair after being reassured by Powell himself on his commitment to fight inflation

Ok, so the Fed is now firmly, unambiguously set on reducing inflation. But what are they going to do?

The Fed has two levers to reduce inflation

First, the Fed can raise interested rates. This slows the economy and reduces pressure in the labor market

By increasing interest rates, the Fed increases the cost of capital across the economy. A higher interest rate makes investments more expensive. As a result, corporates slow their expansion plans, leading to an eventual cool-down of activity

This effect takes about 12-month. A considerable amount of time, given how acute inflation is right now. More so, with so much cash in the accounts of American households and corporations, rates would likely need to be raised significantly to make a difference

As discussed in my last post, historically, there is no example of a central bank removing inflation without causing a recession

Second, the Fed can reduce asset prices. This is done via a process called Quantitative Tightening (“QT”). The opposite of Quantitative Easing (“QE”), which was the hallmark of monetary policy over the past 13 years

Let’s briefly recall what QE is about:

Within Quantitative Easing, the central bank creates (“prints”) new money, and uses this money to buy government debt.1 This way, it removes assets from financial markets, thereby increasing competition for all other remaining assets

First introduced on a large scale in 2009, central banks worldwide have since bought $25 Trillion (!) of government debt for QE programs

By removing $25 Trillion worth of assets from financial markets, central banks pushed up the price for all remaining assets, including stocks, houses, art, fine wine, bitcoin or vintage cars. The riskier, the more upwards

This was called wealth effect, as it made people who owned these assets wealthier. It was the Fed’s goal to create this effect, as its original mastermind, Chairman Ben Bernanke explained in 2012. If people’s wealth had increased, so the idea, they would feel more confident and spend more. This would stimulate the economy to everyone’s benefit

As with many centrally-planned ideas, the second order effects were enormous. In this instance, a dramatic increase between haves and have-nots, and distortions in debt markets, zombie companies, bubbles etc.

Quantitative Tightening is, simply, exactly the reverse

Instead of buying, the central bank is selling its holdings into the market. This increases the supply of financial assets. All else being equal, asset prices decline, the wealth effect reverses

During COVID-19, QE policies were dialled up to the extreme, with almost half of the $25 Trillion spent over the past two years. As a consequence, asset prices went ballistic in absolute terms and as a % of the economy

The chart below shows the market cap of the broadest US stock index (Wilshire 5000) against US GDP. It is literally off the charts

While the soaring stock market in face of COVID-19 mainly stoked the inequality debate further and added to the lingering sensation of societal unfairness, it is soaring real estate prices that have a dramatic negative effect on people’s everyday live

The QE wealth effect outlined above was enough to drive real estate prices up. But in addition, every month since April 2020, the Fed bought $40bn of mortgages to lower the cost of mortgages for new buyers and create an additional wealth effect by allowing people with existing mortgages to refinance to lower rates

As a consequence, real estate prices in the US exploded. Lower and middle class buyers can’t afford to buy anymore, so they have to rent instead. In turn, this lead to a dramatic increasing in rents

Rents are the biggest contributor to consumer price inflation (CPI). They squeeze the lower and middle class and are a big problem for many. With inflation in the crosshairs, it would only be logical that the Fed reverse the wealth effect - i.e. embark on QT. And this is exactly what the Fed is doing now

The Fed communicates with markets by drip-feeding its policies, rather than by big bang announcements. This is in order to prevent negative surprises that might lead to market shocks

And indeed, QT is now being drip fed. First, via a leak to the press with this inconspicuous article in the WSJ early last week. Then followed by various Fed members publicly introducing their positive views on QT

In summary: Quantitative Tightening is coming, and with it the negative effects on most asset prices

The effect will be global as the USD is the world’s reserve currency and our financial system is built on it. More so, Fed decisions will force other central banks to act in order to avoid currency depreciation and thus more inflation

In Europe, as usual, the debate has arrived with a three-months delay. And while Christine Lagarde still publicly ignores inflation, ECB board member Isabel Schnabel just hinted at rates increases. A recent comment in Sueddeutsche Zeitung also caught my eye

The following is very important:

Markets typically anticipate real-economy developments as they take shape on the horizon. Quantitative Tightening is the word no one wants to hear, akin to Voldemor in Harry Potter. To remain with a movie metaphor, it is Cryptonite for financial markets

Markets will likely react and sell off, possibly heavily, probably soon. 20% downside for the S&P 500 is very much possible. But inflation won’t come down as fast, it acts with a significant lag, as discussed above, with policy changes taking ~12 months to take effect

This will put the Fed into a difficult position - will it stand by the markets and provide support by aborting its inflation fight? Or will it let markets fall further and stay course on fighting inflation?

A not so unlikely scenario is that markets will push down until the Fed has to react for financial stability reasons. However, given the bad experience with the excessive interventions following COVID-19, this time, the bailout measures may be aimed at the real economy instead of the stock market

The future is complex and uncertain, and there are many ways where I could be wrong. In particular:

Inflation could for whatever unexpected reason prove transitory, e.g. because higher wages do not feed into higher prices, or because secular trends like demographics2 override near-term dynamics

The sensitivity of the economy to asset price declines could be much higher than thought. A small decline in the S&P 500 could already be sufficient to cool demand (both from corporates for new hires and from consumers for new goods and services)

Markets could ignore the issue and keep rising. This however would only require a more forceful Fed reaction later on

Assuming the view I have laid out is correct, below are my recommendations:

If I’m right, there will be few places to hide. In such a scenario, cash is king. It allows you to buy at lower prices, when other market participants might be forced to sell, which is typically the culmination of a sell off. (Importantly, cash held for asset purchases does not lose value in an environment where asset prices decline3)

Some market-neutral investment strategies make sense in this environment. I had highlighted stablecoin-based lending before, which allows crypto market makers to arbitrage prices on the >250 different crypto exchanges. Merger arbitrage is also a good place to park cash, however, only in safe deals with high quality acquirers. Lower quality deals often get cancelled in turbulent markets

Publicly listed growth stocks have come down a lot. I believe there is still considerable downside in many of them. But markets typically throw the baby out with the bathwater, and at some point phenomenal companies will be for sale at great prices in this area (but not yet)

The downside in high-growth private markets is huge. Current early-stage funding rounds have pyramid-scheme features with participants choosing to ignore the reality already taking place in high-growth public stocks (see “House Money”). If you have exposure to some of the excesses in this area and you can sell, I recommend doing so

The largest US stocks (Microsoft, Google, Amazon, Apple and Facebook) are seen as immune to a sell off and a good “hideout”. However, they are not cheap anymore at all, and in my view the market underestimates their exposure to VC-funded revenues. Google Ads, AWS, Azure etc. are all heavily used by start-ups whose funding might dry up, and the start-ups might have provided the marginal demand that also sets the price

Cryptocurrencies are extremely vulnerable here. Bitcoin was essentially the horse of choice for the “money-printing” race. If the “money-printing” reverses, the effects on Bitcoin should be self explanatory

The biggest winner from higher rates are banks, and I had highlighted European banks in particular in October. They have done very well since, but keep in mind, in a recession they would also get hit

Finally, real estate is a levered asset class. As such it is sensitive to higher rates. More so, a lot of people have rushed into real estate over the past year which has likely brought demand forward. It brings me back to the first point - few places to hide, cash is king

Conclusion: The Fed is the biggest driver for asset prices. The Fed wants asset prices to go down. Don’t fight the Fed

To be precise, the central bank creates reserves which don’t bear interest. It then swaps these with several registered dealers in New York for interest-bearing government debt. The dealer-banks have thereby lost a source of income, which they subsequently seek to replace by acquiring new interest-bearing assets. Whoever they buy these from has to in turn buy new, riskier assets from someone else, creating a positive ripple effect across financial markets

However, with many early retirees during COVID-19, demographics have so far in fact been inflationary

This is obviously different to cash held for consumption purposes. Asset prices can decline while consumer price inflation goes up