Human Nature

Plus ça change, plus c'est la même chose. Plus more on hedge funds

On Wednesday night, the Chairman of the Federal Reserve, Jerome Powell, gave an exceptionally hawkish press conference. Following recent posts, my readers were well prepared for this eventuality. In particular, these statements stood out:

*POWELL: FED'S MAIN FOCUS ON REAL ECONOMY, NOT FINANCIAL MARKETS

*POWELL: ASSET PRICES DON'T PRESENT RISK TO FINANCIAL STABILITY

(Translation: Our goal is to get inflation down for everyday Americans, not to keep asset prices up. And we see no problem in the recent stock market selloff)1

The mantra remains “Don’t fight the Fed” and “Cash is King”. Rallies present precious exit opportunities, or entry points for shorts. The queue of sellers wanting out is long, and the exit is narrow

As mentioned, my conclusions are based on studying the role of liquidity and central banks, which I spent much of the past year on. To study means to look at history. History, as we know, doesn’t repeat, but it rhymes. Largely because human nature stays the same, with all its behavioral trappings

This post provides excerpts from historical sources, and contrasts them to today’s events. They follow narrative rather than chronological order, perhaps illustrating the timelessness of our nature. I hope this provides a useful set of resources that you may go back to at any time to dig deeper

We are herd animals and validate our own actions by looking at others. This creates Fear-Of-Missing-Out, which can overpower reason and drive us to manufacture our own arguments to justify participating

Below are a popular book and a magazine cover, each from the run-up of their respective bubble (Japan 1980s, Tech 1998), each rationalising its existence

As we all know, after 1987, Japan did not move on to rule the world. Instead it got stuck in a 40-year deflationary morass. And the young 1998 traders in their dorm rooms mainly excelled at inexperience of risk, rather than having any insight exclusively available to the youth

Bubbles often follow a similar structure. George Soros beautifully laid it out in a 2014 essay2:

Let’s apply these steps to Cathie Wood’s ARK ETF, the center of the current retail Tech bubble, and we can clearly recognise the same shape:

Ark’s rise and implosion was driven by retail investors, with peak engagement during the COVID-19 lockdown periods, when people were stuck at home. Compare this to the UK bicycle mania in 1895, the excerpt is taken from this research paper:

Staying with bubbles, the next excerpt is from a Vanity Fair story on Microsoft’s travails in the early 2000s. It illustrates the challenges an organisation faces in the aftermath of a crash. Some employees cashed in at the top, they became lottery winners and sat side-by-side to others who missed out and were left with worthless stock options

On the same note, one might wonder how things are going at Peloton, whose share price exploded during COVID-19, with the company worth $50bn at its peak, but never having turned a profit

Insiders sold half a billion USD of stock, mostly to retail investors. These are sitting on 70%+ losses as the stock has cratered. Meanwhile, with the proceeds, the CEO bought a $55m house in the Hamptons. Now McKinsey has come in to lay off people and cut costs, in a desperate attempt to push the company into profitability. Customer engagement has tailed off, but bike prices have gone up 15% on higher raw material costs

Another strong bias we all share relates to recency. We tend to extrapolate from the recent past and expect things to continue the same way into the future

In terms of economics, this means regime changes face doubt even once they’re blindingly obvious

Few believed that the world economy wouldn’t return to the pre-war stagnation after WWII was over (a big boom ensued). Few believed Paul Volcker could crush inflation in the early 1980s and few now believe that interest rates could re-set structurally higher

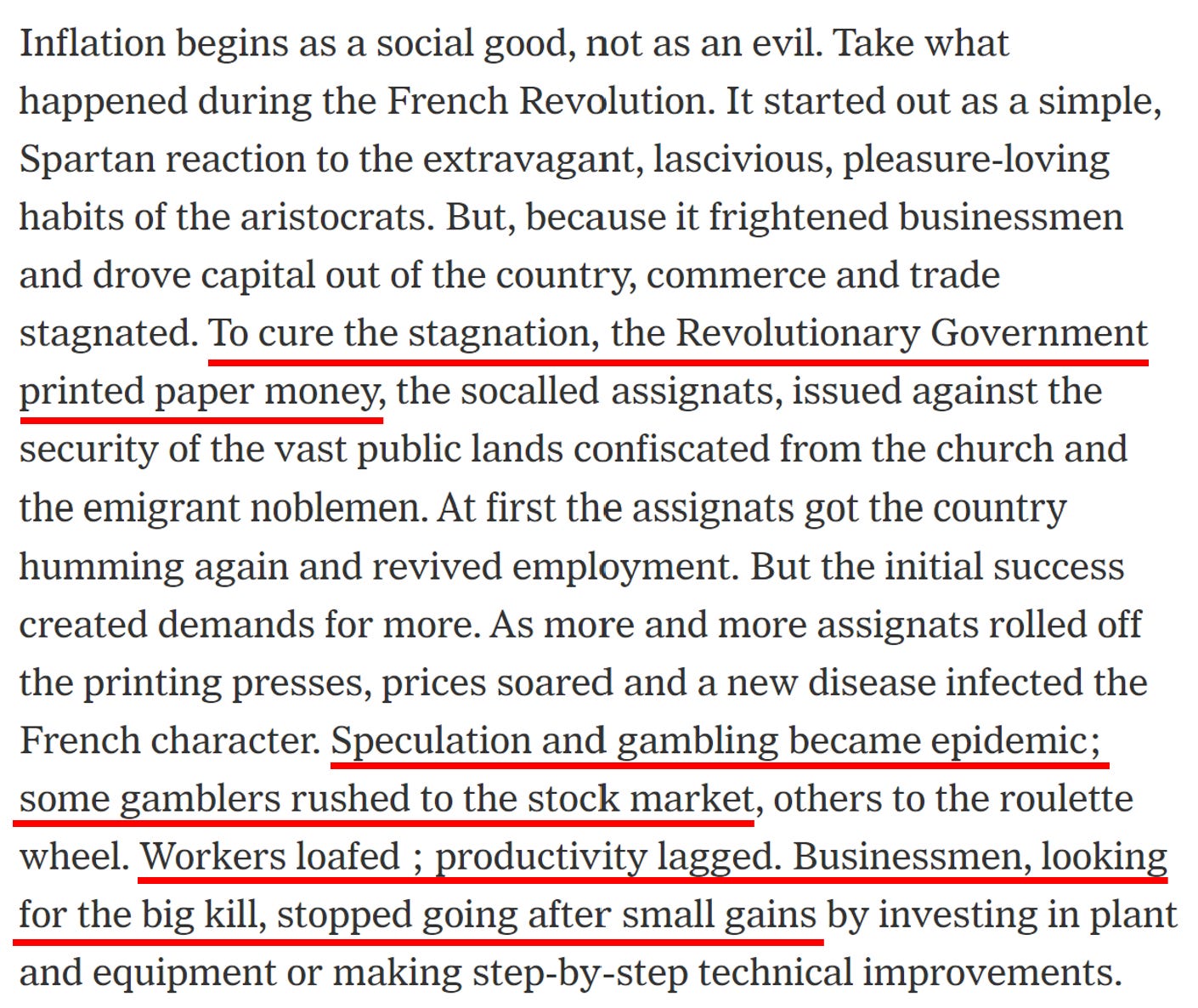

Furthermore, we are inherently lazy, because energy is scarce and we want to conserve it. We’re Janus-faced, every positive character trait has a nasty twin that comes out if we’re too comfortable (e.g. ambition to greed, indulgence to gluttony etc.). When we get stuff for free and don’t have to work for it, it fuels our vices, unfortunately. Take the excerpt below about the French revolution:

Similarly, in a 1979 seminal paper Arthur Burns, who chaired the Fed during the inflationary 1970s, elaborated on the effect of too much money on collective work ethics:

Gambling, stock market speculation, people leaving the labor force, sounds familiar? History rhymes… Take these two recent stories, with countless more examples:

As New York rental aid program ran dry, contractor boasted of ‘38 percent margins’

The $800 Billion Paycheck Protection Program: Where Did the Money Go and Why Did it Go There?

These were well intended support programs, funded with printed money, but much/most of the economic value ended up with middlemen…

Further, we overestimate our own capacities. We have the smartest economists in the world centrally planning our economy. They often fail, yet they are convinced they don’t

I’m talking about central bankers, their role has become so important, even Rapper Snoop Doggy Dog a.k.a. NFT-collector Cozomo de’ Medici watched Jerome Powell’s Wednesday press conference:

A brief selection of Fed Chair quotes over the years:

Janet Yellen in 2021: ““Inflation levels will return to normal next year” (Link)

Ben Bernanke in 2010: “We will not allow inflation to exceed 2%” “My confidence in my ability to control this is 100%” (Link)

Alan Greenspan in 2005: “A bubble in home prices does not appear likely” (Link)

Greenspan wasn’t quite right. Two years later, in 2007, the subprime housing bubble began to crack, creating the biggest financial crisis since 1929

To be fair, in 1994, Alan Greenspan successfully averted inflation by raising rates from 3% to 5.5%

A big bond market tantrum ensued, wiping $1.5tr off global bonds and triggering the Mexican Peso crisis in its wake. It was the first time the Fed had raised rates since 1989, so in 5 long years financial markets got used to the status quo (see recency bias).

However, importantly, the economy remained resilient and didn’t crash. One might wonder/hope that this a template for 2022?

You can find an extensive recount of these events from Greenspan’s perspective here

Finally, tying all these fragments together (rates going up, valuations extreme, inflation, bubble characteristics), one conclusion is looming large - that of a generational top in equities

We have been there before, in 1972 and in 2000. It took 8 and 13 years, respectively, for the market to reach that top again, even though corporate earnings went up 140% and 65% over the same time. There’s even a magazine cover for it, from 1979:

Who knows whether this is what we’re facing now; whether it will be another decade to go back to the January 3rd 2021 all-time-high. However, it’s a possibility, and it’s best to be prepared

ON HEDGE FUNDS

Speaking of bubbles, the January results for hedge funds are coming in, and it’s not looking great, in particular for long/short managers, the biggest category by AUM

After a weak 2021, where the average American L/S generated ~+7% vs.+29% for the S&P 500, (keep in mind, most run their books 40-60% net long), this year has gotten off to a bad start, with the average L/S fund down ~7%, similar to the S&P 500. So the “downside capture” is running at ~90%3

This is not because hedge fund managers are stupid. It’s because the business model has run its course. The necessary skillset has changed and moved to the macro level, but a fund cannot just change its mandate or structure overnight. And with high fees coming in every day, the incentive also often isn’t there

It has been years in the making, the effect has been well researched. While hedge funds protected investors’ portfolios in the big bear market of 2000-2002, they increasingly failed to do so afterwards

In order to gloss over these structural issues, funds jumped on the Fed bandwagon and went long the highest-beta to easy money policies. The most popular setup was long Tech/FANG and short Old Economy/fads/frauds. Hundreds of Billions of AUM are now stuck in these positions, as the macro regime turns

More so, this is before the gigantic landmine which is mark-2-market of private growth investments has gone off

There is still considerable alpha on the short side, but alpha-shorts are size constrained, often in smaller markets caps, and often in Europe which is less liquid

In my view, the most successful ways to avoid this are niche strategies, small/midcap funds and platforms. However, the latter have become very big, and given their high leverage will face some challenges as short-term rates go up

As I had mentioned before, I believe the biggest hedge funds issue is that strategy alpha is not consistent anymore4. Instead, if it hasn’t been eroded entirely, it migrates from strategy to strategy, often in-sync with central bank policies

But if you are a Tech fund and Tech doesn’t work anymore, you cannot re-write your documents and become a Value fund. If you are an Event fund and there are no more events, you cannot overnight become an Energy fund, etc.

The Fed has become the key driver for most hedge fund strategies. The industry needs to adapt and change its model. Time will tell what this model will be

For anyone interested in the technical details, the FOMC also left the option open to, within Quantitative Tightening, prioritise a sale of its MBS portfolio. This is clustered around long durations, so selling these bonds would steepen the yield curve by bringing long-term rates up

On another note, in this short video Soros explains how low leverage is essential to trade a bear market, which is an alternation of fast declines and aggressive snap-back rallies

All estimates from Goldman Sachs Prime Broking