Service-as-a-Software

A quiet AI-revolution has begun in SMEs. Plus following up on the QRA

Artificial Intelligence continues to captivate the collective mind since the release of ChatGPT in November 2022. Its development has been nothing but stunning, with rapidly improving foundation models released in short intervals. Meanwhile, costs have collapsed, with the current most efficient model, Meta’s LLama 8b, c. 300x cheaper to run than the original ChatGPT

So far, the lion share of AI value has fallen to semiconductor companies, similar to the early innings of previous tech breakthroughs such as internet (e.g. Cisco in ‘98-’00) or mobile/cloud (e.g. Qualcomm ‘10-’12, see chart below). Infrastructure and applications came later, from phones to online shops or SaaS businesses, each often enormously profitable

The expectation is for AI to follow a similar path - semis now, then some infrastructure, and powerful, margin-rich apps later. However, its peculiarities suggest that the outcome could be very different this time. In fact, most of the value likely ends up in consumer wallets, or, wherever pricing power allows, industrial profits

Let’s walk through the reasoning, step-by-step for each layer:

Semiconductors - The compute demand of AI is surreal, and at current model efficiency practically infinite. However, semis are hardware that has historically always been very cyclical. Clients overorder, to then get much more efficient with what they have. At the same time, their shareholders eventually want them to reign in spending, so equipment orders tail off. We may see the very early outlines of that in Microsoft’s or Meta’s lacklustre share price performance since their earnings, as investors perhaps worry about free cash flow in the face of escalating capex - whether now or a few years down the line, semis seem likely to follow past patterns of leaving most value generated to later parts of the value chain

Foundation Models - here we see the first particularity and deviation from historic comparison. While there is only a handful of leading foundation model (GPT, Gemini, Mistral, Llama, Claude, Grok), they compete on both performance and cost, and as mentioned the cost declines so far are formidable. A comparison with mobile phone operators in the 1990s comes to mind. Again, only a handful emerged, but competition was fierce via rapidly decreasing prices, to the benefit of those buying the service - FANG-like monopoly or oligopoly profits currently seem unlikely for this layer

Applications - Given the rapid advances in generative text, it is plausible that AI drives the cost of coding eventually to near-zero, with the recent release of the “first AI software engineer” Devin an exemplary step in that direction. This means the barrier to create new applications will likely be incredibly low, with endless custom solutions possible. Take another example - this week, Amazon introduced Q Apps, which lets users build apps on top of their own internal data with natural language (i.e. no coding necessary) - collapsing coding cost and the corresponding ease of creating new apps should drastically shrink the AI app-layer profit pool

If foundation models and applications don’t take the lion share of the AI-generated profits, who is it then? Exactly - the end user, i.e. corporates and consumers

In competitive industries, ordinary consumers benefit from lower prices and/or better service quality as efficiency gains are passed on

In industries with pricing power, efficiency gains increase margins and with it, the respective industrial profits

Now, let’s break this down further, by company size:

Large and medium sized enterprises are typically already very efficient. They have gone through endless cost cutting programs. If you ever visited, say, a BMW factory, the first thing that stands out is the position of every screw and every tiniest little detail has been optimised to the T. AI-driven efficiency gains will happen here, but these are not companies full of low hanging fruits

SMEs on the other hand are a whole other story…

SMEs are the back bone of our Western economies, they generate ~50% of GDP and are responsible for up to 70% of employment

More so, they are typically very local, owner/founder led and have been around for a few decades. They are well established in their ways, but not exactly role models of corporate efficiency

In fact, with much less pressure to continuously rationalise, and less affinity to latest technology trends, their tech stack is often hopelessly outdated. Especially essential legacy services are often still run with pen and paper

Think of all the plumbers, pool cleaners, HVAC installers, building inspectors or care workers coming to your home to provide a service that is highly dependent on locality and people

McKinsey estimates that these workers spend ~40% of their day on bad routes and paperwork (!). An unbelievable amount of waste, but also gigantic low hanging fruits

AI provides cheap, easy to implement solutions to harvest these low hanging fruits. Some examples:

Scheduling/Dispatch - Many of the services I mentioned have to coordinate multiple stops on daily routes, with differing worker demand for each. Planning these in an optimal way is a math problem destined for AI

On-site Problem Solving - Plumbers and installers often work with a wide range of different heating, aircon or ventilation units that each involve their own set of problems. LLM RAG chatbots, with respective unit manuals uploaded, can be queried on-site via voice instruction, to receive immediate feedback for possible solutions - Check out the screenshot from an on-site HVAC problem solver my team and I have been working on:

Invoicing - Many bills are still written by hand or printed, especially in Europe. Companies like Pennylane offer smart solutions that every SME should have

Marketing - Reminders for maintenance or other regular appointments are an easy way to generate additional revenue, and straightforward to automate

Document Pre-population - From requests for proposal (RFPs) to required documentation, there is a long range of tasks that can be worked off much more efficiently with generative text AI (see more below)

Customer Chatbots - Probably the most well broadcast AI application, chatbots can drastically cut the time and cost of customer queries. Klarna published some phenomenal cost savings recently. While the AI relevance in these was called into question given the previous low-tech version in place, this again reminds of many SMEs who don’t have chatbots at all. I have made very good experience with decagon.ai that seamlessly integrates into other apps (stripe, salesforce etc.)

While these improvements seem material low hanging fruits, very few companies so far have centered their business model on proactively picking them. Worth highlighting are:

Cera - Outpatient care aggregator in the UK and Germany that increases the margins of its acquisition targets ~3x via implementing its own tech stack. Examples include cutting recruitment cost by 80% via digitising the process, and using GPT-4 to convert conversations recorded on care assessors’ phones into a care plan, cutting its preparation time from 12 to a couple of hours (see document pre-population above). Cera last raised $320m in late-stage funding in ‘22

Odevo - Private-equity owned Swedish property manager aggregator with its own tech stack that automatises the many menial tasks involved in the business

Pipedreams - US-based HVAC rollup that upgrades the tech stack of its acquisition targets and boasts of 100% local sales growth within 24 months. The company just raised a $25m Series A

Importantly, many of the essential services SMEs share in common that they rely on skilled labor, which is increasingly scarce, especially in Europe. AI tools can significantly improve service quality for their customers, but cost efficiencies go straight into margin as these businesses maintain pricing power. Typically they see more demand than they can fulfil

Margin gains added up across the vectors above can be significant. This brings me back to the post title, which is a word play on the Software-as-a-Service companies that dominated the 2010s. Will we see an attention shift from SaaS to essential legacy services with software-like margins as they implement tech? The ease of AI tools puts this proposition within reach

However, one big problem remains. SMEs are notoriously hard to sell into, and very few vertical market software vendors have cracked this segment

It is easy to see why - SMEs are often local, owner-run businesses established many decades ago. Once these companies are humming along, and as many founders now reach retirement (over 300k in Europe alone over the coming years!), there is often little appetite to go the extra mile necessary to elevate the business further

The solution is simple - it is the path that Cera and Pipedreams have chosen. The easiest way to get an SME to upgrade its tech stack is to buy it. VC investor Elad Gil also sketched this out recently and termed the strategy “AI Buyouts”. This approach unites several other highly advantageous features:

SMEs are the final frontier of investing in a world where institutional strategies have penetrated almost every possible niche, and public markets have become a knife fight between quants over basis points

Due to size constraints, Private equity firms typically avoid the market below $3-5m EBIT, which ironically now sees an avalanche of sellers due to demographic change. The few that participate via platforms or buy-and-build see astronomically high returns such as Shore Capital’s >50% IRRs. Lots of sellers, few buyers = high returns

With the substantial supply/demand mismatch and little institutional participation, it comes as no surprise that the average search fund investor (one of the rare strategies participating in SMEs) yields a return of 32% p.a., despite c. 40% of search funders failing to find a target (!). Again, a staggering result in a world where the search for yield has arbitraged almost everything away

In other words, the SME supply-demand asymmetry provides ample return even before any tech stack upgrades are implemented. Just imagine the additional upside

Now, there is plenty of prejudice out on SMEs, from a perception of low-quality to founder dependency or excessive economic sensitivity

Having reviewed hundreds of them myself over the past months, I can confirm that these views are unwarranted. Sure, many SMEs are not exciting. But given the abundance of supply, these is still a huge number of high quality businesses full of opportunity, available at multiples that large business buyers can only dream of

In my view, upgrading the SME tech stack via acquisitions is a generational opportunity whose time has come. Capturing it will involve an unusual mix of skills that includes investing, operations and AI

Current market views

The following section is for professional investors only. It reflects my own views in a strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please see the disclaimer at the bottom for more details and always note, I may be entirely wrong and/or may change my mind at any time. This is not investment advice, please do your own due diligence

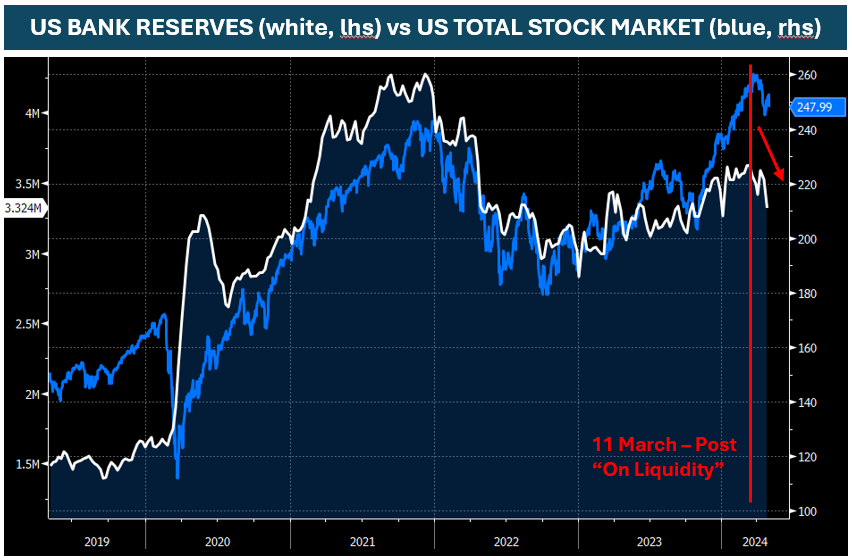

As I frequently stated in the past, liquidity is the most important, and likely least understood variable in the current period of high financialization and excessive government deficits. Measured by proxy of US bank reserves, we can see these declined recently as I had forecast in my 11 March post. With it, global equity markets rolled over, and this past Wednesday’s QRA details suggest no near-term change to this story

Very few investment houses focus on these relationships that now dominate global capital markets. I notice Ruffer spelled out some similar dynamics, even forecasting a 1987-type equity meltdown, however this seems unlikely to me. Why? Liquidity is essentially set by the government, thus the Treasury and Fed could easily fight such an outlier risk should it really transpire

Either way, in light of this, I had already maintained a very cautious stance for Q2, and as per this recent tweet converted my remaining asset holdings (precious metals and Tesla) into cash, which I once again see as - temporary - king

Here is what I think for the rest of the year:

Liquidity likely weighs on markets for the remainder of the quarter, but likely turns positive from July onwards once T-Bill issuance picks up again, latest probably with the 1st August QRA

Inflation data probably won’t provide much near term relief due to shelter inflation, which I see as having troughed. The math is too boring to spell it out extensively, but essentially single family new rents are picking up again as per Core Logic’s SFR index which forms part of the BLS OER calculation, while renewal rents have flatlined for some time at 5%. New apartments rents are still in decline, but a smaller part of the calculation. Also note the 1-yr lag between Case Shiller and OER

Deficit spending will continue. Simplified, deficit spending is bullish as long as it is financed by T-Bills, and bearish if it is financed by long-term bonds. For that reason I think eventually, most of the deficit will be financed by T-bills, like in the 1970s, as historically no one wanted to own the long end of a spendthrift sovereign. T-Bills are cash-like, thus fuelling both inflation and asset prices

I plan to go long when one of the following occurs:

A major CPI miss that brings back rate cuts. This would motivate the $9tr parked in MMF to want to get out of them, providing a bid to all assets (keep in mind it is about the intention, there is never “cash on the sidelines” that disappears, cash just changes hands)

The next QRA refunding announcement increases bills substantially (1st August)

The Fed ends QT, for example due to market stress. This would reduce the Treasury’s funding needs, especially if they cut bond issuance for it

A major equity washout occurs with very bearish sentiment. With speculators the most long the S&P 500 in over two years, I still see dip buying as prevalent and do not think we are near this, but it could happen over the coming months

Whenever one of the above happens, I want to go long high beta (e.g. semis) and long the monetary debasement plays (e.g. gold, bitcoin), as I do not see another long-term outcome bar further money printing. I do not think anyone is serious about reducing the deficit, in fact Europe is now trying to emulate the US with Draghi in view as European Council president and his endorsement of deficit spend. An AI-driven productivity wonder that offsets these dynamics is possible, but likely takes several years to transpire

Finally, for anyone tempted to buy US bonds (=coupons) to hold them for the long run, I encourage to read the passage below from this week’s TBAC statement, the private market advisors to the Treasury on issuance composition. Who would want to stand in the way of this ever expanding supply avalanche?

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

Thanks Florian, this post is gold! Made me start thinking about what the AI influenced future will really look like 🙏

Great note