The Blind Spot

Why interest rates will likely rise higher than many think. Plus some more on Tech

In my last two posts I described how the Federal Reserve’s answer to inflation would likely lead to a decline in most asset prices and possibly a recession

Equity markets have now picked up on the narrative and entered a bear market. However, many market participants continue to treat inflation as a passing episode. The common assumption is that we will soon revert to the low-interest rates regime of the past decade

I believe this argument is born out of complacency and there are good reasons for structurally higher rates. The case is laid out below

Let’s start with a brief recap of the previous posts

Excessive stimulus in response to COVID-19 has caused the highest inflation in 40 years and the initiation of a price-wage spiral in the US

Inflation takes from consumers and gives to asset owners. After decades of rising inequality, this is upsetting for the asset-poor 80% of the population. Biden’s approval ratings are near all time lows

This creates political pressure to act for the Fed. It has pivoted and is now fighting inflation via increasing interest rates (which slows the economy) and Quantitative Tightening (which reduces asset prices)1

Inflation is the number-one economic topic. But stunningly enough, financial markets seem convinced that it will soon go away

The market’s view on inflation can be deducted from the yields on long-dated government bonds, like the US 10yr and 30yr. These trade near historical lows, at ~1.7-2.3%. They were at 10% last time inflation was this high

The “Terminal Fed Funds Rate”, which tells how high rates would go before they are cut again, is at 1.75%. This implies that only a small raise would be enough to eliminate inflation

What’s going on? Are markets right, and we will just see a short blip after which inflation is a thing of the past?

I believe the reason is behavioral. Most of today’s finance professionals have only ever experienced a deflationary environment, so they expect that to continue into the future

MIT-professor Andrew Lo describes this effect as survivorship bias. The few market participants who bet on inflation had awful returns over the past 40 years, so they have all left the market and gone “extinct”

Interestingly enough, the reverse was true when Paul Volcker slowed inflation in the early 1980s. The bond market did not believe he would be successful and continued to price in higher inflation for another 10 years, wrongly so

Either way, let’s look at the the main argument against higher interest rates. It goes as follows:

There is too much debt everywhere. Therefore, a small rate increase will slow everything and quickly push the red-hot economy back into balance

And yes, the aggregate debt mountain for the United States is enormous (similar for Europe)

However, this line of thought has a gigantic blind spot

My readers trained in corporate finance will notice that debt is only part of the picture

The right number to look at is “net debt”, or debt minus cash. Cash pays off debt, so the two should be netted against each other

And cash in the US economy has exploded, this is why we have inflation. Below is the familiar chart of M2 in the US. To stay with the analogy from corporate finance, M2 is the “cash & cash equivalents” of the national economy

Now, the aggregate debt chart also includes government debt, which has gone up a lot during the pandemic

But government debt is not the same as private sector debt. Governments can always print money to service their debt2, and they did just that over the past two years within the massive QE programs

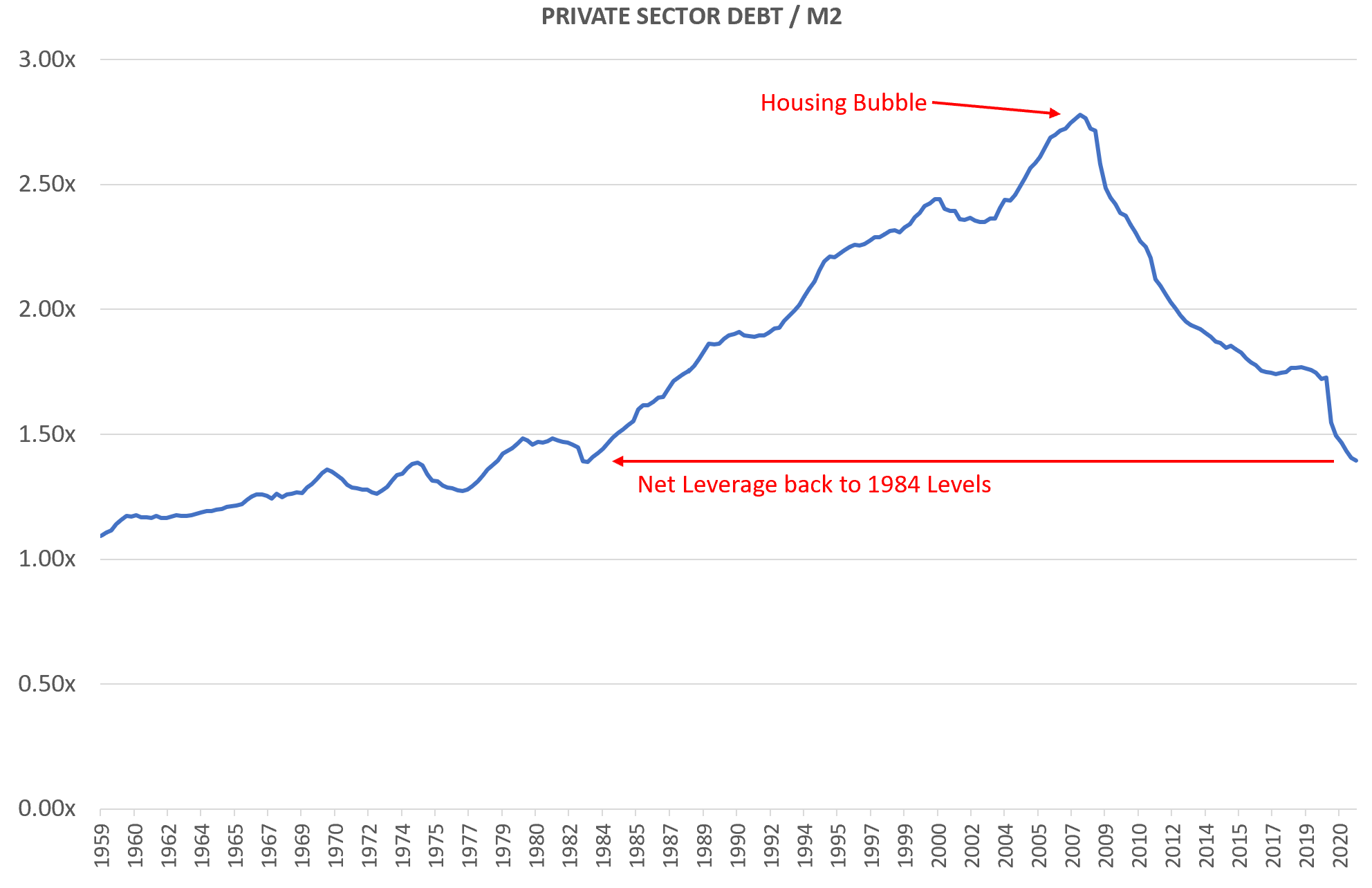

Let’s put all this together into one chart. Add M2, exclude government debt, and we can derive the “net debt” of the private sector in the US. This gives us a solid statement about the health of the world’s biggest demand driver

As you can see from the chart, on an aggregate basis, the US private sector was last this healthy in the early 1980s. All the excesses from 2000s and the housing bubble have been removed.

More so - we haven’t included household assets like real estate or equities. Including them, the picture would be even starker

There are many other ways to look at this, with the same conclusion. For example, take the ratio of debt payments to household income - again, a very healthy measure

Keep in mind, even if rates were 4x higher than they are today, this number would not go up 4x - most private sector debt is fixed and long duration, (e.g. the typical US 30-year fixed mortgage). So even with higher rates, this ratio only increases very gradually as old debt is replaced with new

Unlike commonly assumed, the US private sector is financially, exceptionally healthy. Into this backdrop, rates would have to rise considerably to slow demand

Aside of private sector health, there are two further reasons for structurally higher interest rates

First, the biggest deflationary force of the past half-century was globalisation. This dynamic has likely run its course

Much of the disinflation of the past 40 years came from the addition of China, Eastern Europe and South-East Asia to the global labor market, which kept wages down in the West

This also reduced aggregate demand - as Henry Ford used to say “If I don’t pay them well, who will buy my car?”

The political wind has firmly changed against globalisation. Brexit, Trump’s tariffs and tougher immigration laws are all a consequence of this. Noticeably, Democrat Joe Biden has made no attempts to reverse Trump’s immigration policies, and he’s kept the China tariffs

The results are very visible in public data. There is now a ~2m gap in US immigration that contributes to a tight, inflationary labor market

Second, while the private sector is in good shape, credit demand has so far remained sluggish. But credit is a tinderbox that can very quickly fuel an inflationary fire

As long as inflation remains significantly higher than interest rates (which is the case now with rates at 0% and inflation at 7%), there is a strong incentive to take out credit and spend it. And this is what we’re sending now, private sector credit demand has picked up considerably in Q4 21

An acceleration in credit demand is very dangerous for an inflationary economy. Credit is newly created money, it adds to M2 and can quickly accelerate existing inflationary trends

Ok, so rates may be significantly higher going forward, but what does that mean?

Every asset in the Western world (and beyond) is priced off the interest rate on US government debt

The US is the engine of the world economy, and the US-Dollar is the world’s reserve currency. This make interest on US government debt the global “risk free” benchmark rate, other central banks including the ECB have to follow

Because the risk-free rate has steadily declined over the past forty years, riskier assets have revalued higher, from stocks to real estate, from fine wines to luxury watches. The riskier, and the more leverage, the higher the revaluation

If this trend reverses and the risk-free rate increases, the tailwind turns into a headwind. Investments have to overcompensate what can also be described as multiple compression with exceptional operational performance

In my last post, I had laid out a list of recommendations for asset allocation in the current context. It still holds and you can find it here. The short summary: Right now, I continue to believe cash is king and there are few places to hide

That is unless you would want to short the market, for which every relief rally provides entry points in my view. The Nasdaq-100 seems the most logical instrument in that case, as I had mentioned in my last post the FANGs might provide the wrong illusion of a safe haven

But cash is not held in vain, there will be great opportunities if this bear market resembles all previous ones and eventually ends in a catalytic decline and reversal

Beyond that, my humble recommendation would be to be mindful of the headwinds created by higher interest rates, and the questions they imply:

Will this investment still work if the multiple compresses? Will this house still be a good purchase if mortgage costs rise? Will this startup still see follow-on financing if funding markets dry up?

Conclusion: Interest rates will likely go higher than many think, as a healthy US private sector, de-globalisation and credit creation all maintain inflationary pressures. This will create headwinds for asset values, requiring a very thoughtful approach to asset allocation

ADDENDUM - Some more bits on Tech

There is a huge wave of developers going into web 3.0

This follows a similar patterns of enthusiasm for computer science degrees during the New Economy bubble, which cooled off after

While private funding rounds continue to defy gravity (see checkout.com’s 40bn valuation), it is important for founders to keep in mind how these dynamics can reverse on the way down. See below excerpt from a messaging board about stock-based compensation at Square

How much air is in the current NFT frenzy? This NFT by cognac brand Hennessy is currently listed for $226k

An interesting debate on the pros and cons of web 3.0 by the co-founder of Signal and the co-founder of Coinbase can be found here

Finally, de-globalisation is not limited to the West. The number of US study-abroad visas issued in China has declined significantly since 2015

Strictly speaking, it has indicated its intention to raise rates and conduct QT, which markets anticipate in their price action

As long as the debt is issued in its own currency, which is the case for all major Western Economies. It might default on debt issued in foreign currency (e.g. Argentina on USD bonds)