The Emerging States of America

Plus: Why a near-term bottom may be in

I have to state my admiration for the United States of America. It’s a country where anyone can make it, no matter what background or religion. It remains the engine of the world economy, and the defender of the free world. US financial prowess finances EU exports, subsidises global pharma innovation, and its defence budget is sole obstacle between Putin and the West

However, over the past week something very peculiar happened in financial markets that demonstrates how the playbook has been altered for the United States, with lasting consequences for years to come

This post explains what happened, and provides an outlook on the implications. As usual, it closes with a markets section, where today I outline why a near-bottom for equities may be in

Regular readers will be familiar with my views on the business cycle and the likelihood of a recession. Reading the financial press over the weekend, it’s fair to say this has now become a universal assumption:

Plenty of headlines confirmed this view. UBER’s CEO released a memo to its employees where he announced to “be hardcore about costs”. Facebook and Amazon issued hiring freezes. The CEO of the world’s largest auto supplier Bosch warned of a “big recession in the making”.

In addition, the rumblings in the housing market are getting louder - I believe we’ll see a significant increase in inventory as well as price declines in the coming weeks

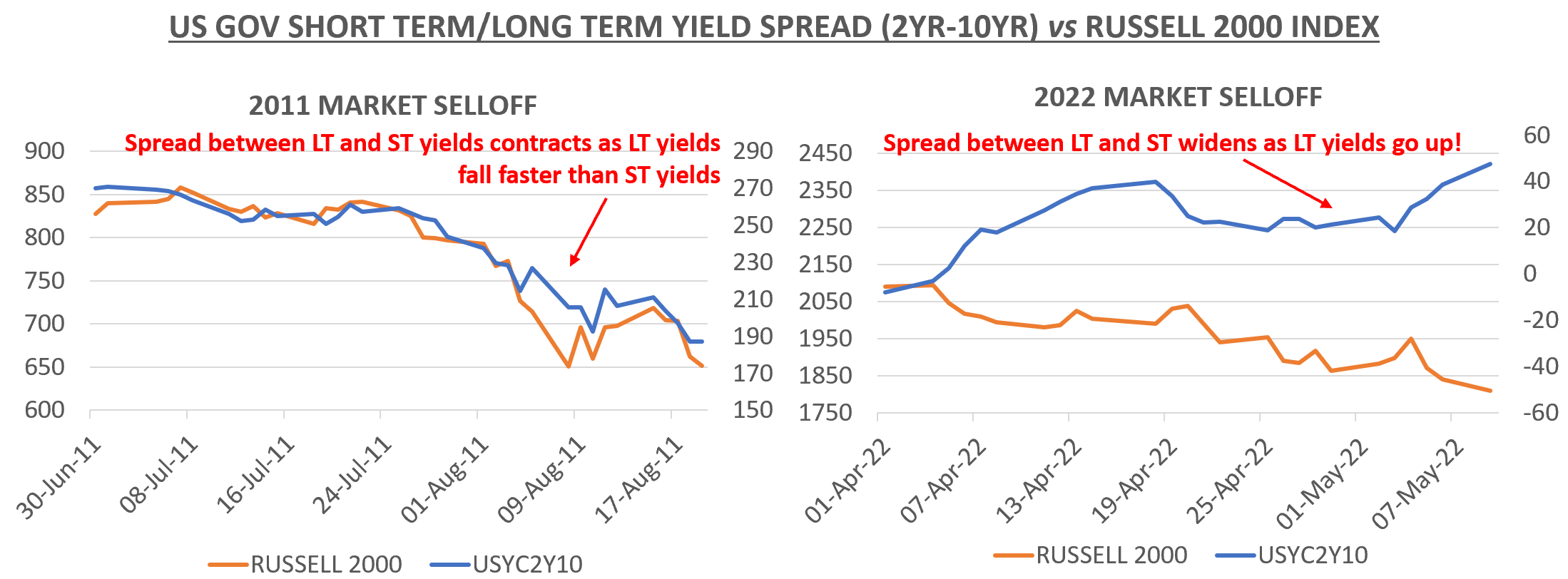

With everyone expecting a broad slowdown, the yield on long-term US government bonds should do what it always does in the lead-up to a recession - it should go down. Why is that?

Simplified, the government bond market can be split into the short end (0-2 years duration) and the long end (all else, but mainly 10 year and 30 year bonds)

The “short-end” is mostly driven the overnight rate set by the Federal Reserve

The “long-end” is also influenced by that, but more so by the economic outlook. The Fed only sets short-term rates, so for future years the market has to guess the corresponding future overnight rate, which is determined by how the economy does at that time

When a recession nears, markets reduce future growth expectations, so long term rates fall. Short term rates stay steady until the Fed indicates it will lower the overnight rate. Accordingly, at this point the spread between short-term and long-term rates contracts

But over the last week, the opposite happened. Short term rates fell, but despite the increasing recession risk, long-term yields increased

So, counterintuitively, the spread between short term and long term yields widened substantially, something you normally only see if the economy improves. Below is a side-by-side comparison of the recent equity sell-off with a similar period in 2011

Ok, interesting. But why does this matter?

In the Western financial system, all assets are priced off the long-term interest rate on US government bonds. These are considered the “risk-free” rate which serves as benchmark for everything else

So when long-term bond yields rise, all other assets decline in value, all else being equal. The cost of capital also increases, which slows business activity

If we’re looking at a recession, this means a hefty double whammy for risk assets. Both the valuation multiples and the earnings expectations are cut, which imply steep price declines

Ok, got it. So what’s the reason behind this move in bond yields, that now wrecks havoc across financial markets?

The key reason is a loss in confidence in US institutions, in particular the Treasury and the Federal Reserve

After the Federal Reserve stopped buying government bonds in March, the bond market is not “manipulated” anymore and left to free-market price discovery by rational investors1

And how do these investors assess long-term bonds? Just as you would: They are wondering whether it’s a good investment. Bonds in a reserve currency are very unlikely to default, so the biggest risk to the investment is inflation

And with a 30-year investment horizon, that means taking a bet on the soundness of a country’s institutions, and their ability to prevent inflation

After years of manipulating financial markets, first with Quantitative Easing and then with money-printing for stimulus cheques and subsequent inflation, trust in US institutions is severely harmed

Long-term yields are going up, because, despite much strong rhetoric, the market does not believe the Fed’s resolve in its fight against inflation

Instead, the implicit assumption is that the Fed will cave the moment the recession broadens and open the monetary firehouse again. This would be too early, so inflation would immediately worsen - which makes long-term bonds a bad investment

Ironically, the negative price action in long-term bonds is how markets bring discipline to institutions. Which brings us to the title of this post:

Capital markets forcing governments to assume a sound monetary stance is straight out of the Emerging Markets playbook. It’s the story of the so called “Bond Vigilantes”, imaginary watchmen who discipline governments by selling their bonds when they step over the line

In this case, investors may only return to buying US bonds once the US has re-established its credibility in its fight against inflation. If the US refuses to do so, its bonds will keep falling. This slows the economy, so this way the market forces a slowdown in inflation

Now, to make a judgement on whether any “vigilance” is actually warranted or whether the market - as often - overreacts, one needs to look at the long-term inflation outlook

For this, I always come back to the chart below, which -in my view- summarises the inflation story in one single depiction

It’s the ratio of people looking for jobs vs. the number of open positions in the US economy, a good way to judge the tightness of the labor market. This decides how fast wages grow, which is the ultimate driver of inflation:

As you can see, after decades where globalization depressed wage bargaining power and kept inflation now, we are in a new inflation paradigm. In fact, we likely already entered it in the late Trump years, when deglobalization measures around immigration and tariffs showed first effects

Given this context, I find it likely that inflation settles at a higher plateau going forward (>3%). This would mean the current high bond yields are here to stay, even if they look extended in the short-term, after their recent run

One thought to consider in this context: A huge amount of malinvestment has occurred over the past two years. Just think about the billions (trillions?) of Dollars that went into crypto fantasy projects, and contrast that to investments that are now sorely missed in fertilizer, food supplies, natural gas etc. - Will these malinvestments act as strong deflationary agents? I don’t think so. This bubble didn’t involve the same leverage as historical precedents; also US banks are in very good shape

The biggest risk to the future economic trajectory is populism. Populists that make untenable promises can charm an electorate that is fed up with the status-quo. However, this comes at a steep cost

Again, we return to the Emerging Markets playbook. Looking at Latin America, populist regimes have a long tradition, often summarised as Peronism after Argentina’s hugely popular 1950s leader Juan Perón. They have contributed to decades of boom-bust cycles

Today, in the West, Boris Johnson won Labour’s heartlands in Northern England with a populist agenda that has since left the UK in the worst shape of all OECD countries. France only closely escaped Marine Le Pen’s economic program, which would have likely seriously harmed the country’s economy

But with all criticism, one has to accept that both Johnson and Le Pen gave a voice to large parts of the population that the establishment left out in the cold

Summary: The US bond market now follows the Emerging Markets playbook, and US institutions will have to work hard to re-establish trust

This means that long-term yields are likely higher for longer. It also means that real yields likely settle in positive territory. Taken together, this provides alternatives for capital looking for a home, which makes it scarcer for other purposes

A higher cost of capitals moves investor focus away from growth and towards cash-flows and profitability. For the investment industry, this will present many challenges. After decades in a different paradigm, few professionals have acquired the skillset needed for this dramatically different landscape

What does this mean for markets?

As mentioned before, the commentary in this section reflects the positioning of my own investments. However, instead of giving specific buy/sell recommendations I want to emphasise the reasoning behind it, so it can be helpful in your own, independent decision making. With that in mind, these are my current views:

Nasdaq 100 - Having been negative on “long-duration” for most of the year, with a brief intermission in last March, I’m now turning constructive on the Nasdaq-100 for the near term. A possible peak in yields, together with extremely negative sentiment and a substantial sell-off lays the ground for a near-term rally in this index, in particular in light of declining commodity prices and some softening in inflation lead indicators2. Also, merger arbitrage spreads blew out yesterday, which is typically a sign of forced liquidations that occur near lows. Medium term, I remain negative and think any rally, if it comes, should/would be sold. Earnings forecasts are still likely way too high and we’re likely only in the early innings of a recession

Bonds - For the same reasons, I also find it likely that bond yields peaked for now, even though I do not think they are ripe yet as a long-term investment

XHB/Housing - As mentioned earlier in the post, there are many signs that US housing is going into a downturn, which is obviously bad for homebuilders. However, the sector trades with interest rates, so I expect some short-term reprieve here, too, if yields halt their ascend, even though the medium-term outlook remains negative

Luxury - The current climate is not one for luxury spending. I think it is telling that the market for secondary watches has shown considerable weakness recently, and inventory is rising fast. I expect this sector to be very challenged going forward

Commodities - As discussed before here and here, a global recession is negative for commodities. Also, please note that while the oil price hasn’t reached levels that historically corresponded to demand destruction, bottlenecks in refining capacity, in particular for Diesel, have driven prices at the pump much higher than the oil price would imply, and according to GasBuddy US Diesel demand is down 17% last week. However, given the severe underinvestment and inventory depletion in many commodities, the floor in a downcycle should likely be higher. Further, as discussed, it seems likely that we’ll face a higher-inflation environment in the years to come, which is in contrast to the deflationary years following the end of the last commodity bull-market in 2008

Finally, whenever there is a seismic shift in financial markets, bodies of unsound investments are exposed. These are my “candidates” for the current cycle:

Crypto - Yesterday’s turmoil around algorithmic stablecoin UST/Terra/Luna is likely a harbinger of more distress to come for this sector. Ponzi-elements are still ubiquitous, just looking at UST itself, its market cap is $18bn, but how can anyone believe that an algorithmic stablecoin3 can work? This is frankly beyond me, as it would be akin to the invention of a perpetual motion machine

Real Estate in Germany and Canada - In both markets, real estate prices have far outpaced the real economy and leverage restrictions are too loose. As mentioned, 10% of German residential real estate loans are >100% LTV, I think it’s very likely that some banks, developers or funds/investors have overextended themselves

Buy Now Pay Later - This concept was celebrated as innovation and stuffed with billions of Dollars of growth capital. Yet, it’s one of the oldest retail concepts in the world, paying in instalments, which is mainly a behavioral illusion of affordability, usually followed by defaults down the line, especially as the cycle turns. With consumer budgets under severe pressure from escalating energy prices, it’s not hard to imagine how this unfolds. I will close today’s post with an FT-headline, which encapsulates the current state of affairs well

Many bond market participants are buyers for regulatory reasons, such as banks, insurers, corporate treasuries etc.

Average hourly earnings, part of past Friday’s Non-Farm Payroll data and a good proxy for wage growth, came in below expectations and decelerated sequentially

Algorithmic stablecoins are backed by a formula and balancing mechanism. This is in contrast to stablecoins which are 1:1 backed by USD reserves, such as Circle’s USDC

Amazingly good post.

Insightful as always! What does turning constructive in the near term mean?