War and Covid

Issues mount for Russia and China

As before, please continue to consider donations. 3.2 million Ukrainians are now displaced, cities like Cherniv or Mariupol are entirely in ruins and the destruction continues every day. You can find the link to UNICEF Ukraine here

In my last post, I laid out how a potential ceasefire in Ukraine and renewed lockdowns in China would take some air out of an elevated oil price. Together with extremely bearish investor positioning, this would set the ground for a strong rally in risk assets, in particular DAX and US-Tech. Markets have indeed moved that way, yet a ceasefire still has not been reached and there continues to be much uncertainty about the evolution of COVID-19 in China

This post looks at both these issues in turn and summarises their economic implications

Following days of intense negotiation, it seemed like a ceasefire was ready to be signed. The Financial Times ran a headline story, and several further sources, including directly from the negotiations, corroborated that an agreement in principle was found. Yet hostilities are still ongoing and bellicose rhetoric has again intensified. What happened?

With Russia increasingly in disarray, the Ukrainian stance has firmed. While the country was prepared to accept major, painful concessions, the increasingly large cracks in the Russian army as well as Russian domestic politics provide an opening to push for better terms. Several notable events occurred over the past days:

The Russian military campaign has deteriorated further. I had shared Francis Fukuyama’s assessment of likely Russian defeat last week. With every day the signs grow that the Russian army is overwhelmed and exhausted. A Ukrainian presidential advisor estimates Russia to have fighting power only for another 10-14 days

While sanctions are crippling Russia, Ukraine receives immense international support. After President Zelensky’s speech in Congress, the US committed to another $800m worth of arms deliveries, incl. 800 antiaircraft missiles, 9,000 antitank weapons and 100 advanced tactical drones. A huge amount of weapons, ideally suited against the Russian heavy machinery on Ukrainian territory

The Russian domestic situation shows visible strains. Many Russians speak out despite repressions, with prominent examples a TV-producer who protested during the main evening news, or this mother talking to ABC about her soldier son in Ukraine:

Russia’s leadership seems in disarray. In eery Stalin-style moves, a general was detained and several high-ranking FSB officers put under house arrest. A plane with senior government officials, maybe even foreign minister Lavrov himself returned in mid-air on its way to China. Putin’s latest TV speech was dark and unhinged

China’s position has very visibly shifted. China’s ambassador to the Ukraine made a public appearance in Lviv, lauding “the unity of the Ukrainian people”. Chinese domestic media has also changed its tone and become more favorable to Ukraine. A call between Biden and Xi has been scheduled for today

There is an opening to push for better terms, and the Ukraine is taking it. Noticeably, public territorial demands have now moved away from conceding Donbass and Crimea:

This strategy shift is understandable and it is right. But is also comes with high risks

Russia will possibly intensify attacks on civilian structures. That’s the only conventional military leverage they still have. It likely means more innocent deaths

Russia is a nuclear power. If pushed near defeat, nuclear threats will likely re-emerge

Summary: The rapid weakening of Russia improves the Ukraine’s position, at the expense of a rapid, unfavorable solution. It also increases the probability of Russian domestic turmoil and thus regime change. Equally, the tail risks of irrational actions are now higher. However, in my view, these remain tail risks

The pivot in China’s Ukraine stance brings us to the second topic. In China, lockdowns have returned after several Omicron outbreaks. Looking at the severity of the current COVID-19 wave in Hong Kong, many see this as an harbinger for what’s to come for China

So far, China has employed a “Zero-Covid” strategy with strict quarantine rules for travellers, frequent mass testing and draconian local lockdowns

This has been a success. The number number of COVID-19 deaths is dramatically lower than in the West (<10k vs US ~1m), generating much domestic pride

The “Zero-Covid” approach worked for the Delta-variant. Will it also work for Omicron? Let’s have a look

To start, Omicron is significantly more contagious then Delta

Various studies have assessed Omicron to be 1.2x (Danish study, within same household) to 2.0x (NHS study, between strangers) more viral than Delta

An Omicron case in a quarantine hotel in Hong-Kong has reached notoriety, where the virus was transferred across the hallway, without in-person interaction. The Omicron subvariant BA.2 is compared to measles in its infectiousness

This is not a good start, what about vaccines?

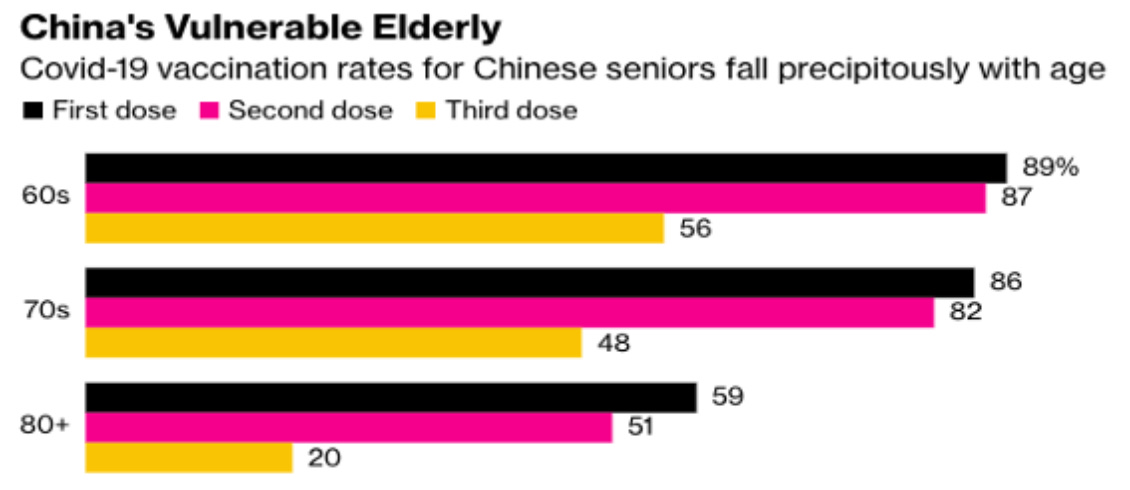

China’s vaccine drive is somewhat lagging. While an optically high 85% of population are jabbed, many vaccinations are over a year old. Booster shots are much more behind than the West

Critically, same as in Hong Kong, the share of unvaccinated elderly is high. This is the most vulnerable group:

More so, the Chinese vaccines are worse than their Western counterparts, in particular for elderly

China’s vaccines lag Moderna/BioNTech in all metrics. The difference is the starkest for protection against severe Omicron disease for elderly (34% vs. >80% for BioNTech)

All this would suggest high vulnerability towards mass outbreaks. So why didn’t China simply introduce Western vaccines?

Initially scheduled for approval, this was indefinitely postponed as vaccines got entangled in nationalistic propaganda. China’s COVID-19 success story of successful containment was to rely on domestic means only

China faces a huge challenge. Mass lockdowns kill economic growth, and a mass breakout undermines the “Zero-Covid” story. This is on top of several existing challenges:

The Beijing Olympics were a PR-disaster, with athletes stating to “never want to go back” and low international viewership

The country’s real estate woes are well chronicled and, after a cascading sequence of defaults, will require enormous intervention to be turned around

Chinese stocks have been hammered as the geopolitical risk premium increased following China’s alignment with Russia. China is now actively trying to rectify this, with the pivot on Ukraine very much related

The Ukraine conflict also impacts China’s food production. Fertilizer supplies are now scarce, and China is a big net-importer

President Xi is up for re-election this year. COVID-19 issue could not come at a worse time

Here’s why, despite the bad context, I don’t think it will get to that:

China is very quickly learning from Hong-Kong’s experience and stepping up its vaccine drive, with a focus on the elderly

Outside the elderly, Omicron is much less bad than Delta, even for the unvaccinated. So getting the elderly vaccinated is what really takes the sting out of Omicron, and it opens the door to a departure from Zero-Covid policies which are hard to maintain given Omicron’s contagiousness

China found a way to let Western vaccines in through the backdoor. On the 14th February, the country approved Pfizer’s Paxlovid pill. Paxlovid reduces severe disease by ~90% when taken up 4-5 days after infection, so even for the unvaccinated this changes the game. Pfizer has committed millions of doses to China, the first batches arrived last night. Keep in mind, with Omicron’s milder profile, only the severely ill/risk patients would need them

Summary: Given Omicron’s contagiousness, expect further flare-ups. However, with a reinforced vaccine drive and the introduction of Paxlovid, China now has the tools to exit its lockdown-driven Zero-Covid policy

What does that mean for the economy?

With broad lockdowns in China unlikely, there is no respite for the world’s commodity markets

Let’s take oil again as an example. China’s full-scale lockdowns in February 2020 took out 4.6mb/day out of oil demand. A repeat of this would be a gift for strained Western buyers; in an inelastic market such demand reduction would equate to a precipitous price drop. As outlined above, this now seems very unlikely. With Chinese travel demand already low, any further demand reduction absent of draconian lockdowns will likely be de-minimis

For anyone hoping that stranded Russian oil could calm the market as it returns after a ceasefire, that oil is likely already back in the market. While Western companies like Shell stay away after public shaming, independent traders have picked up the slack, attracted by up to 30% discounts on Ural barrels. To avoid being called out, they turn off their ships’ trackers

The US economy remains on fire1, and commodity markets remain extremely tight. All this continues to be a very favorable backdrop for oil services (ETF:OIH). The US government now openly demands that domestic oil companies increase production and cut buybacks

For the DAX, after a 13% up-move, the risk is more balanced. The market now likely looks through further noise out of Russia, bar a dramatic escalation. However elevated commodity prices will weigh on European industrials

For the US and the Nasdaq in particular, near term, amidst excessive bearishness, the likely path is higher/neutral for now

However, medium term, the risks have increased enormously. I will write about this in more detail in another post, but the Fed’s response to inflation remains grotesquely inadequate

Often a chart/picture says more than words, so I will leave it at the below for today:

Meanwhile, near-term inflation data continues to accelerate

After a brief pause, February rents resumed their uptrend again, up 1.1% month-on-month, or ~13% annualised (!). With a ~40% share, cost of shelter is the most important component of CPI. Please see the previous post “It’s all about housing” for the relationship between rents and inflation

The most likely trajectory is now that the Fed will have to hit the breaks very hard later this year, with more dramatic results. The timing is unclear, it might attempt to hold off with a more aggressive intervention until after the mid-terms, but its hand might be forced before