When Narrative Follows Price

Is the economy improving, or are we witnessing a financial markets mirage?

In my last post “The Paradox”, I laid out how the January inflation print would likely be “hot”, and how that would likely trigger a sell-off in bonds that takes equities with them. So far, data and markets have indeed followed the sequence

More so, together with seemingly strong January retail sales and unemployment data, many investors are now convinced that a re-acceleration of the US economy is imminent. Even the Fed has joined, as various officials push for even more rate hikes to fight off this presumed resurgence. Meanwhile, it remains very much unclear whether the unprecedented 4.5% interest rate increase over the past year has yet been digested

Has the economy truly turned? Or have we once again fallen victim to our emotions, where prices action tricks the collective mind to cherry-pick arguments that best explain whatever prices suggest?

Today’s post checks in on the most recent data and lays out how the re-acceleration hopes based on January’s consumer-centric coincident data are likely a mirage. Meanwhile, both lead- and increasingly coincident indicators for the cyclical economy continue to deteriorate at a pace rarely seen in the past 70 years. A significant decline in industrial production is likely already under way, historically enough to cause substantial recessions and unemployment

As always, the post closes with my view on current markets, where I outline the trade opportunities I see from this -in my view- enormous divergence between market perception and reality

Often, things move quickly in financial markets. While recession fears dominated late last year, investors have now moved to a “no landing” (= no economic slowdown at all)

Fed officials concur to a resilient US economy…

…and fund managers have cut their recession expectations from 76% to 24%

Is it true, no recession, are we out of the woods? Or what was actually going on in January? Let’s have a look

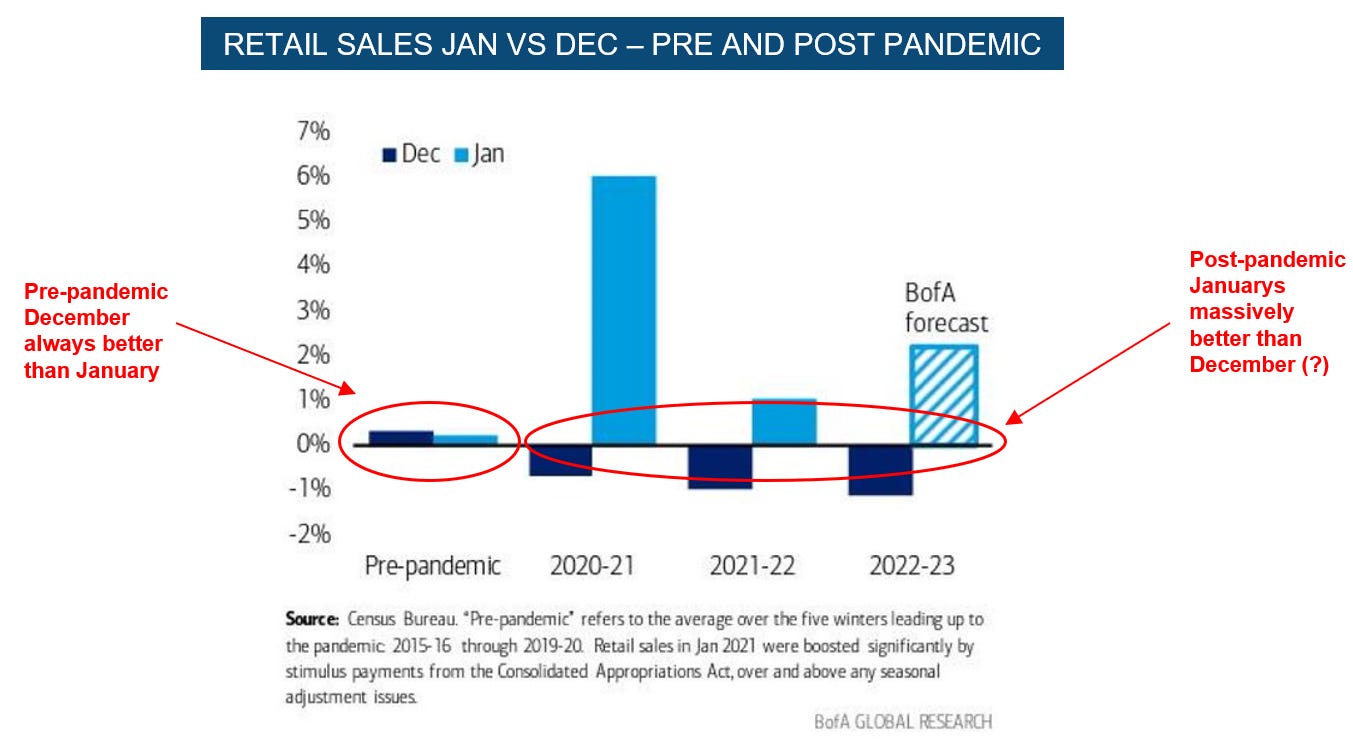

Much of the re-acceleration views rest on very strong January retail sales, which came in at +3.0% month-on-month, much better than expected

How did Americans have that much more money in January? Sure, many wages reset that month, as did social security payments for millions of pensioners

But still, such a resurgence seems extreme. In fact, a much more likely explanation can be found in the seasonal adjustments, which overstate the strength of the data. Since the start of the pandemic, Januarys consistently index higher than December, which makes little sense outside the ‘21 stimulus cheques. (NB: Similar dynamics apply to the January NFP employment data1)

Beyond seasonal adjustments, inflation also plays a role. Not only did wages and social security payments reset in January, many bills and contracts did so too - a big reason why the January CPI print was so high

So what is the true state of retail trends? For that we should look at a number that excludes both seasonality as well as inflation

We achieve that by comparing “real” retail sales (i.e. excluding inflation) year-over-year. In stark contrast, this figure shows a 1.6% decline, and remains in a consistent negative downtrend since Spring ‘21

We can corroborate that conclusion from various other angles

Credit card and auto loan delinquencies are on the rise, the latter to a 13-year high

Corporate earnings this week added to the assessment of a frail consumer. Walmart and Home Depot guided to 2.5% and 0% nominal (!) growth for 2023, and Walmart’s CFO John Rainey commented on Tuesday’s earnings call:

Further, near-time retail trends for February show the January “bump” already in reverse

Summary: Seasonal adjustments and inflation likely overstate the strength of the US consumer in the various January data releases. The underlying trend likely remains downward

Now, ok, the US consumer may not be booming, but whatever the data, it also isn’t falling off a cliff

But here’s what’s important - recessions are usually not triggered by consumers. They are triggered by cyclical industries

Regular readers will be familiar with my framework that puts highly volatile housing and durable goods sectors at the center of the ebb and flow of the economy

The huge demand swings in these industries then permeate the remainder of the economy with a lag

I would also like to recall that historically slowdowns in manufacturing were enough to both cause recessions and significant employment losses, even at times when the services sector grew (e.g. ‘69,’73,’01)

So the most critical question we should attempt to answer is - how are cyclicals doing? The answer: Their outlook continues to worsen, as they face a trifecta of headwinds

First, they struggle with weak demand, as the Covid-stimulus boom brought forward goods purchases. It’s simple - how many new TVs, handbags or garden grills do consumers need before they are saturated?

Second, goods businesses produced too much, assuming that the artificially high demand would continue. More so, with supply bottlenecks persistent they double-ordered many input products. But demand tailed off and bottlenecks eased. As a result, inventories are now sky-high while new orders keep trending down

Third, the Fed’s aggressive monetary policy massively increased the cost of capital. This is particularly painful for manufacturing businesses. They are called the “capital goods” for a reason - these businesses need a lot of capital for their production processes, and that capital is very expensive now

Taken together, it’s a perfect storm for cyclical industries. As a result, it is highly likely that industrial production declines meaningfully in the near future

Historically, the current sales-to-inventory ratio has given good guidance of industrial production in the following months. It suggests a steep decline is under way

Now, a recession could still be avoided or at least softened if this slowdown in cyclicals would not lead to layoffs. However, that unfortunately seems unlikely. As I’ve laid out in previous posts, it likely won’t be long until manufacturing businesses respond to these pressures by cutting headcount

The pressure on corporate margins is immense. In Q4 ‘22, S&P 500 revenues (excl energy) grew by 4%, mainly due to inflation, yet profits fell ~11%. This gap will only grow in ‘23

Corporates are highly likely to cut cost in response, and many labor market lead indicators such as the employment component of the Empire Manufacturing Survey suggest layoffs are on the way

Unfortunately, job losses are not only likely in manufacturing, but also in construction, the other crucial cyclical industry

Looking at the chart below, we see a record divergence between construction employment and housing starts

For these jobs to stay, housing starts would need to recover pretty much imminently. Instead, the opposite seems much more likely

There is a record number of homes under construction in the US. These need to be finished and sold, before housing starts can grow meaningfully again

However, selling these may take quite a while. Housing affordability is at a multi-decade low due to high mortgage rates, while the consumer is pinched and unemployment likely to go up. Unsurprisingly, new mortgage applications, which lead future home sales, just dropped to a 28-year low

Finally, I had mentioned how some Fed officials now call for ever higher interest rates in reaction to the January data, while we haven’t yet seen the effects of the unprecedented 4.5% rate hikes over the past year

Keep in mind, today’s economic data was “created” many months in the past. Additional hikes today will slow the economy 6-12 months from now

Looking at bankruptcy filings in January, which came in at a decade high, I cannot help to think that the Fed has done enough already, and we would simply need more patience to see the medicine work

Large parts of corporate America, as well as its government are highly indebted. Higher rates for longer represent a tremendous challenge for many, from overlevered LBOs to States dependent on capital gains taxes. Please see more details on these dynamics in my previous post “Incentives and Inequality”

Conclusion:

The January boost in consumer-centric data is likely overstated and unlikely to represent a new dawn

The cyclical economy is under immense stress, with weak near-term activity readings, and deeply recessionary advanced readings

Housing should continue to slow as a huge pipeline and poor affordability weigh on future activity

Cyclicals and housing lead the broad economy. Either way, their weakness will likely be sufficient to cause a recession and an increase in unemployment

In contrast to today’s consensus view, my base case remains that of a “hard landing”, with a US recession likely already under way in Q1, or imminent (Q2)

What does this mean for markets?

As always, below is my personal attempt at connecting-the-dots for my own investments. Please keep in mind - I may be totally wrong, nothing is more important than risk management, and none of this is investment advice

As laid out in the most recent post, I had sold the long-term US Treasuries of the “60/-40” book in anticipation of a “hot” January CPI and kept the equity shorts. This has so far proven to be the right decision. My thoughts for markets from here:

The momentum in long-term US Treasuries (TLT) remains negative and likely only breaks either with a cathartic sell off, or a significant event, or both. I am waiting for that moment to enter, and believe the labor market data on March 3rd, the next CPI print on the 14th or the FOMC meeting on the 22nd could provide the turning point, possibly at or near the previous high for the the 10-year (4.25%). I would regard that moment as the last cycle-high for interest rates, and would expect yields to fall from there until the economic cycle turns up, possibly in Q4/’23 or Q1/’24

Equities likely remain under pressure as long as bond yields go up. Tech in particular appears vulnerable after the 2nd largest short cover in a decade in mid-Feb. I remain short equities and have added Nasdaq shorts on the cover news

Some brief sectoral thoughts:

Oil/Commodities - A “hard landing” has historically always been bad for commodities including oil. About 1/3 of global oil demand is industrial, I also see China’s reopening handicapped by lackluster export demand and its real estate bubble, which appears tough to push further with record vacancies rates. I’m short SXPP, XME and GLEN LN

US Regional Banks (KRE) - This sector faces many headwinds, including likely higher loan losses, higher income reliance on loans, pressure to raise deposit rates as QT and the RRP remove liquidity. Finally, once rates turn, interest income should decline

Homebuilders (XHB) - Builders have front-run a housing recovery that is unlikely to materialise. I see much downside for this sector. I’m looking to enter shorts in both KRE and XHB

Credit - Billions (or trillions?) of US Dollars have been deployed in credit over the past six months. This area is perfectly set up for a rug pull as spreads are tight while the economy deteriorates. Be fearful when others are greedy, in my view now is the time to sell both Investment Grade and High Yield

To conclude, I could envisage the follow trajectory for capital markets. Please keep in mind that this assessment is very fluid as market context changes every day (see “The Observer Effect”). I may also simply be wrong

In my view, the current equity and bond sell-off remains joined at the hip and likely continues until bonds find a bid, which could come around mid/late March (see above)

With bonds stabilising, another bear market rally could follow as coincident data then is likely not weak enough yet to usher in a period of “risk off”

That “risk off” period, where equities sell off hard, while bonds and the dollar are bid, could follow later in Q2/Q3

In response, the Fed changes course and economic lead indicators recover. This could mark the end of the bear market, and a longer lasting rally ensues (Q4?)

Whatever happens, it is highly likely that the bear market is not over yet. With that in mind, short-term US treasuries continue to offer a very attractive 5% yield, a save and stress-free way to invest

DISCLAIMER:

The information contained in the material on this website article reflects only the views of its author (Florian Kronawitter) in a strictly personal capacity and do not reflect the views of White Square Capital LLP and/or Sophia Group LLP. This website article is only for information purposes, and it is not intended to be, nor should it be construed or used as, investment, tax or legal advice, any recommendation or opinion regarding the appropriateness or suitability of any investment or strategy, or an offer to sell, or a solicitation of an offer to buy, an interest in any security, including an interest in any private fund or account or any other private fund or account advised by White Square Capital LLP, Sophia Group LLP or any of its affiliates. Nothing on this website article should be taken as a recommendation or endorsement of a particular investment, adviser or other service or product or to any material submitted by third parties or linked to from this website. Nor should anything on this website article be taken as an invitation or inducement to engage in investment activities. In addition, we do not offer any advice regarding the nature, potential value or suitability of any particular investment, security or investment strategy and the information provided is not tailored to any individual requirements.

The content of this website article does not constitute investment advice and you should not rely on any material on this website article to make (or refrain from making) any decision or take (or refrain from taking) any action.

The investments and services mentioned on this article website may not be suitable for you. If advice is required you should contact your own Independent Financial Adviser.

The information in this article website is intended to inform and educate readers and the wider community. No representation is made that any of the views and opinions expressed by the author will be achieved, in whole or in part. This information is as of the date indicated, is not complete and is subject to change. Certain information has been provided by and/or is based on third party sources and, although believed to be reliable, has not been independently verified. The author is not responsible for errors or omissions from these sources. No representation is made with respect to the accuracy, completeness or timeliness of information and the author assumes no obligation to update or otherwise revise such information. At the time of writing, the author, or a family member of the author, may hold a significant long or short financial interest in any of securities, issuers and/or sectors discussed. This should not be taken as a recommendation by the author to invest (or refrain from investing) in any securities, issuers and/or sectors, and the author may trade in and out of this position without notice.

Similar dynamics apply to the +500k January NFP job growth number. Seasonal adjustment likely overstate the true degree of employment growth in January, which if approximated with other data lies more in the vicinity of 150k-250k

Florian,

normally, given how sensitive housing is to interest rate, at this point of the housing cycle, we should see construction employment at least plateauing if not not dropping, why is it still going up?

also, is it possible that this time around, in-person service sector cycle is lagging manufacturing so much that recession could be delayed longer than we thought due to the pandemic? Note that hospitality and leisure employment level is still below pre-pandemic, and much lower below trend, indicating still huge labor shortage in that sector. Also, the most recent NFIB report shows many businesses are finding it hard to find quality labor. Another industry that's finding all time high labor shortage is the car repair sector. These are contradictory signals to "close to recession" bet.

You can call it lagging effect of the policy, but I say FED this time is very transparent about their policy projection. It doesn't make sense for the construction industry to keep hiring (JOLT opening still healthy for construction too) at this point in cycle when housing starts is clearly going down. Any good reason they are still doing so?

Florian, even if your recession outlook is correct, why do you think automatically inflation will also come down?

rate raise in the late 1980s early 1990s didn't do much to core inflation at all (stays at 4.5 ~ 5% throughout the whole period). Basically, you had the worst of both worlds (inflation plus recession). Any good reason why we cannot have something similar this time around? Most people are either in the inflation/soft landing camp or deflationary recession. I haven't seen any view point suggesting stagflation.