Land of the Rising Yen?

Recent Treasury decisions should weigh on the US Dollar. Possibilities to express that view

Following the Treasury’s recent decision to prioritise short-term bills over long-term bonds in funding its deficit, I wrote that we would need to see the dust settle to judge its relevance. While I had already made up my mind with regards to risk assets and bought them, last week’s data now shows a meaningful increase in US bank reserves. I perceive this as strong indication that the Treasury decision was indeed possibly the first marking of a transition of monetary power from the Fed to the Treasury, also know as “Fiscal Dominance”

Is the Treasury is now the Fed? And has this “new Fed” just decided to ease financial conditions significantly? I think it’s possible. Aside being positive for risk assets, this is negative for the US Dollar. But against what? The Dollar’s biggest counterpart, the Euro, likely faces an ECB in easing mode next year as Europe’s economies appear to increasingly struggle. Gold is another obvious choice, but its positioning is long and real rates are above 2%, a headwind for it. As mentioned, I’ve recently had much more sympathy for Bitcoin, and see the case for it here, but a big move already happened

My choice fell to upside exposure in the Japanese Yen, which I acquired on Friday’s close (see here). The reasoning is laid out in today’s post

The following section is for professional investors only. It reflects my own views in a strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please see the disclaimer at the bottom for more details and always note, I may be entirely wrong and/or may change my mind at any time. This is not investment advice, please do your own due diligence

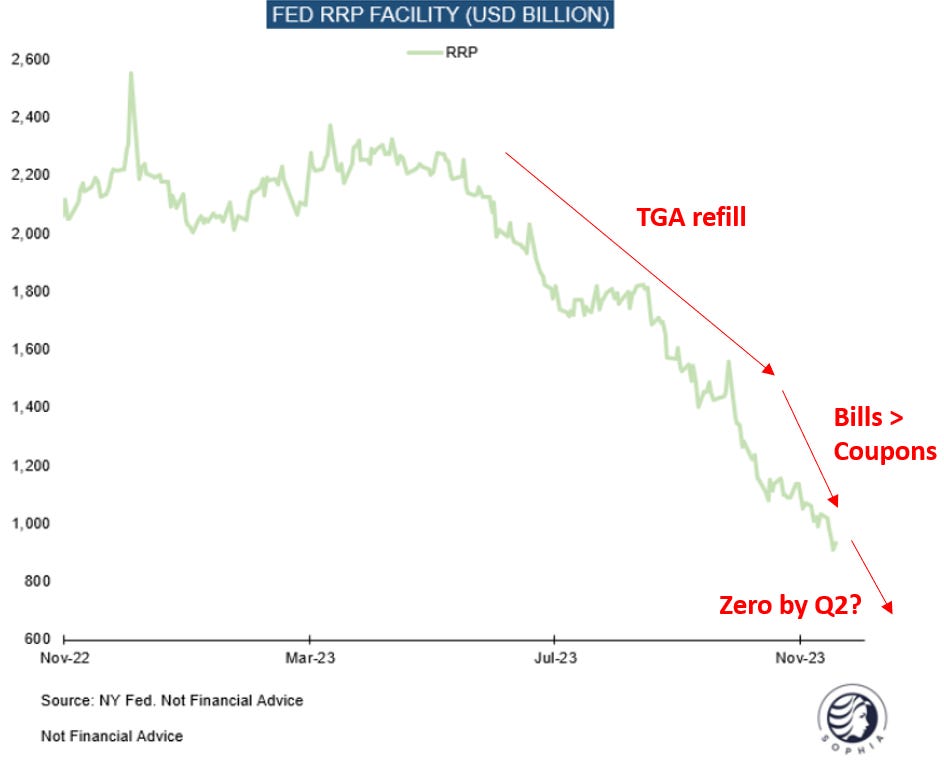

As discussed in several previous posts, on the 1st of November the US Treasury published its decision to prioritise short-term Bill over long-term Coupon issuance in the coming quarters, as the bond market did not want all the duration the Treasury had offered given deficit and long-term inflation concerns

More Bills mean primarily two things:

More liquidity for financial markets as bills are “pristine collateral”

Long-term yields stay lower than they naturally would. This neuters their corrective mechanism against excessive government deficits, as well as their dampening effect on inflation

And in addition, in today’s specific case:

The Reserve Repo Facility (RRP) gets drained. The RRP is a repo facility that money market funds (MMF) can use to park cash at the Fed overnight in exchange for the lower bound of the Fed Funds rate + 5bps. With manymore Bills now in circulation, their yield rises above what the RRP offers, so MMFs are incentivised to switch from the RRP into Bills

If MMFs switch from the RRP to Bills, bank reserves increase, which in turn is likely stimulative for both the real economy and asset markets. The mechanism works as follows:

An MMF buys Bills from the government and uses funds parked in the RRP for it

The government then spends these funds into the economy, where it shows up in bank deposits

Deposits show up as liabilities on banks’ balance sheets, their equivalent on the asset side are reserves, which they hold at the Fed

It now gets very technical and I will expand on that in one of the coming posts, but for a variety of reasons, in my view, more bank reserves are stimulative for both assets and the real economy, even in an ample reserves regime (see footnote for details1)

So, as per last week’s data, bank reserves have now visibly risen, as the blue shaded area in the below chart shows:

Taken together, the Fed on hold, more Bills and higher bank reserves provide an easing of financial conditions, which as described in the introduction is US-Dollar negative. In addition to going long rate sensitive out-of-favor equities, I have chosen to hedge against dynamic with long Yen exposure, for the following reasons:

First, the Yen is a very popular fast money short. In fact, as per CFTC positioning data, it has rarely been as shorted before. This would provide plenty of fuel should speculators be forced to cover

Second, it appears that shorts have reached their maximum extension. BOJ governor Ueda made comments on Friday that read very dovish (“It is hard to definitely say that a current weak is negative for the economy”). This should have weakened the Yen further, instead it strengthened. This suggests dovish news are possibly in the price

Third, the economic context for Japan appears favorable and the country is not necessarily in need of further monetary easing. Using its stock market as a proxy for the need to ease, the Nikkei just hit a 33-year high this morning, and fast money positioning suggests it could have further upside, as these shorted the recent rally

More broadly, the BOJ is on a path to exit its Yield Curve Control policy, while the Fed is on hold, and the possibly “true Fed” (i.e. the Treasury) is in easing mode

If we think in FX terms, we see both a strengthening dynamic on the Yen side of the cross, and a weakening dynamic on the US Dollar side of the cross - I find this an appealing context, together with the extreme Yen short positioning

I expressed this view late Friday when the CFTC data came out by buying short dated near-the money call options on JPYUSD (see here). These can be rolled, as the cost of carry is relevant given the US-Japan yield differential. As always, I may be wrong with this view or its timing, and I may change my mind any time. Please do your own DD

To take it a step further, if the EU economy slows more than the US, the ECB would likely have to ease more than the Fed (or the Treasury…). This trade could therefore be swapped for a long JPYEUR position towards the end of the year, when typically year-end positive EURUSD seasonality might abate

Conclusion:

The US might have seen a transition of monetary power from the Fed to the Treasury, and the Treasury is in easing mode. Together with the Fed being on hold, this is likely a headwind for the US Dollar

Aside from the risk asset longs I detailed in last week’s posts, I hedged against this dynamic with long Yen exposure

Japan’s economy appears to do well, with policy easing likely incrementally dialled back, in contrast to the US. At the same time, fast money accounts are very short the Yen, setting up a large pool of money that could be forced to cover, should the Yen rally

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

DISCLAIMER:

The information contained in the material on this website article is for professional investors only and for educational purposes only. It reflects only the views of its author (Florian Kronawitter) in a strictly personal capacity and do not reflect the views of White Square Capital LLP and/or Sophia Group LLP. This website article is only for information purposes, and it is not intended to be, nor should it be construed or used as, investment, tax or legal advice, any recommendation or opinion regarding the appropriateness or suitability of any investment or strategy, or an offer to sell, or a solicitation of an offer to buy, an interest in any security, including an interest in any private fund or account or any other private fund or account advised by White Square Capital LLP, Sophia Group LLP or any of its affiliates. Nothing on this website article should be taken as a recommendation or endorsement of a particular investment, adviser or other service or product or to any material submitted by third parties or linked to from this website. Nor should anything on this website article be taken as an invitation or inducement to engage in investment activities. In addition, we do not offer any advice regarding the nature, potential value or suitability of any particular investment, security or investment strategy and the information provided is not tailored to any individual requirements.

The content of this website article does not constitute investment advice and you should not rely on any material on this website article to make (or refrain from making) any decision or take (or refrain from taking) any action.

The investments and services mentioned on this article website may not be suitable for you. If advice is required you should contact your own Independent Financial Adviser.

The information in this article website is intended to inform and educate readers and the wider community. No representation is made that any of the views and opinions expressed by the author will be achieved, in whole or in part. This information is as of the date indicated, is not complete and is subject to change. Certain information has been provided by and/or is based on third party sources and, although believed to be reliable, has not been independently verified. The author is not responsible for errors or omissions from these sources. No representation is made with respect to the accuracy, completeness or timeliness of information and the author assumes no obligation to update or otherwise revise such information. At the time of writing, the author, or a family member of the author, may hold a significant long or short financial interest in any of securities, issuers and/or sectors discussed. This should not be taken as a recommendation by the author to invest (or refrain from investing) in any securities, issuers and/or sectors, and the author may trade in and out of this position without notice.

To highlight in particular: IORB paid on reserves, reserves not evenly distributed (SVB crisis) and deposits more likely to be spent in real economy than RRP funds (= positive for asset earnings)

I confess that I don't understand how the BoJ will exit YCC / their loose monetary policy....

I've been following the theme closely for a long time and only closed my Long USD/JPY late last month. However my views remain consistent on the matter -- I've written a lot on it but these two threads are indicative:

From last September: https://x.com/philoinvestor/status/1567789714467348483?s=20

From this January: https://x.com/philoinvestor/status/1615335485051740161?s=20

They both give great context on Japanese macro and the Yen.

The way you tie these various forces together is super enlightening. Very easy to understand and super helpful. I am blown away and so glad I found this newsletter!