Unstable Equilibrium

What consensus misses about the US Regional Bank crisis, and how the debt ceiling relates to it

In my last post I highlighted the importance of data in economic analysis, and how AI can play a critical role. Today’s post returns to said data; I will lay out in a few simple steps why the US Regional Bank crisis is significantly worse than consensus thinks, and what is the likely path forward from here. I also highlight how the debt ceiling debate ties into these dynamics, together creating a volatile cocktail that likely interrupts the current tranquil equilibrium risk assets have settled in

Once more, all roads lead to the Federal Reserve, as the likely only measure that puts Regional Banks out of their misery is interest rate cuts. But with inflation still sticky, that option does not exist until substantial economic damage is done. As such, more bank failures are a quasi-mathematical certainty, which reflexively then sets the stage for said rate cuts later in the year

As always, the post concludes with my current outlook on markets

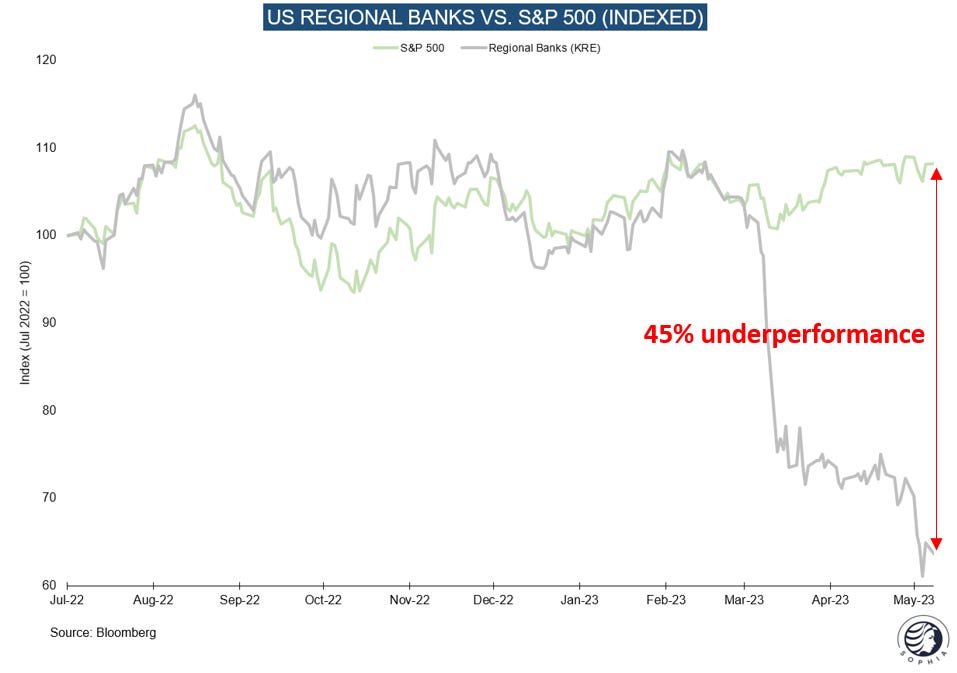

Over the past few months, broad equity markets remained isolated from abysmal US Regional Bank performance. A historically unprecedent divergence opened:

This is in large part because there hasn’t yet been any spillover from bank stresses to the broad economy. More so, some recent data lead commentators to believe that the issue is already on the retreat

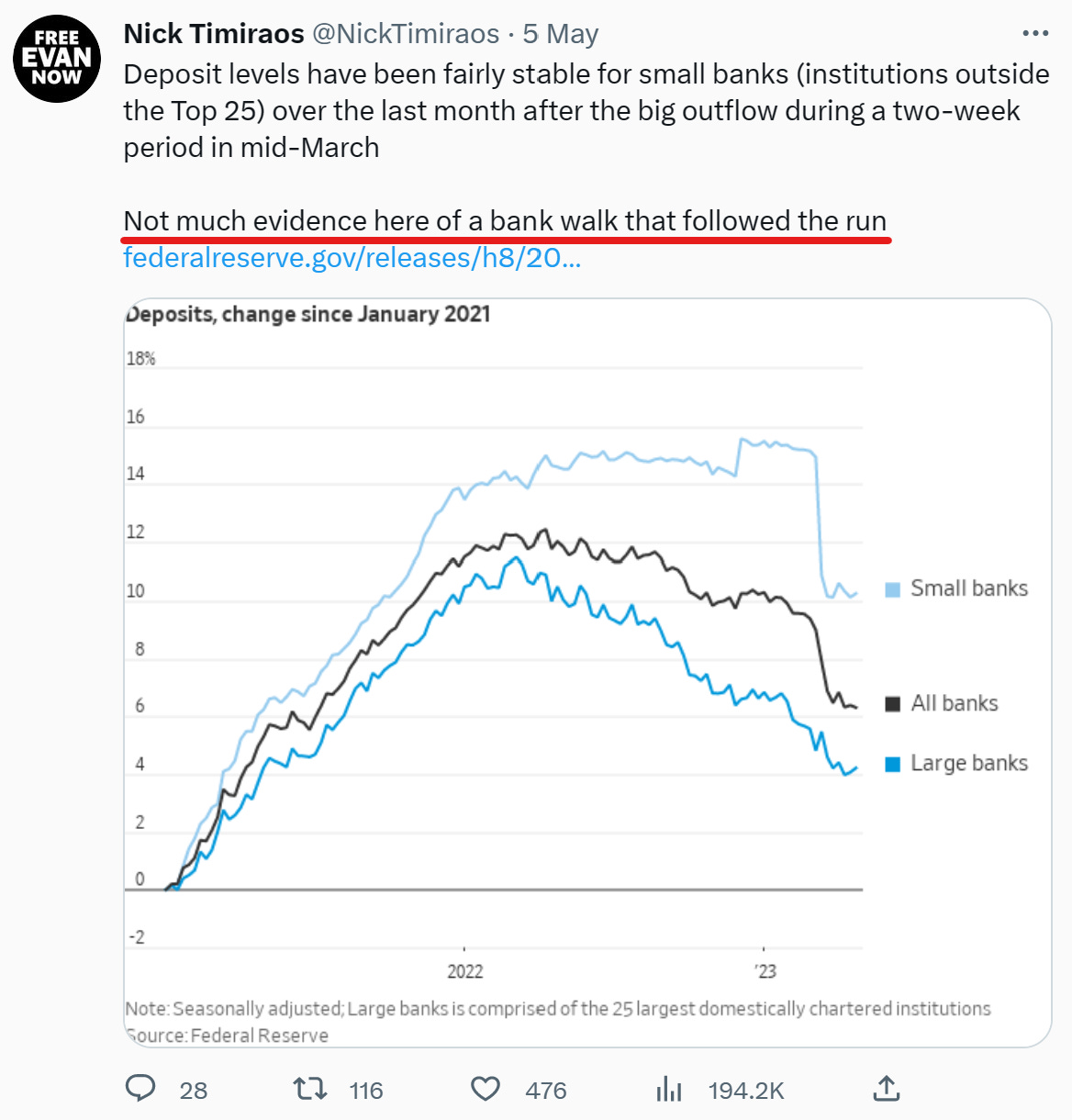

Below tweet by Wall Street Journal writer Nick Timiraos is reflective of market consensus - the “bank run” following Silicon Valley Bank’s demise in March is now not even a “bank walk” anymore. According to the Fed’s latest H.8 release, which contains aggregate balance sheet data for all US banks, the deposit flight is over

Now, what doesn’t quite add up with that conclusion - why did Regional Bank PacWest announce to explore strategic options last week, in this context a “hail Mary” move one step before receivership?

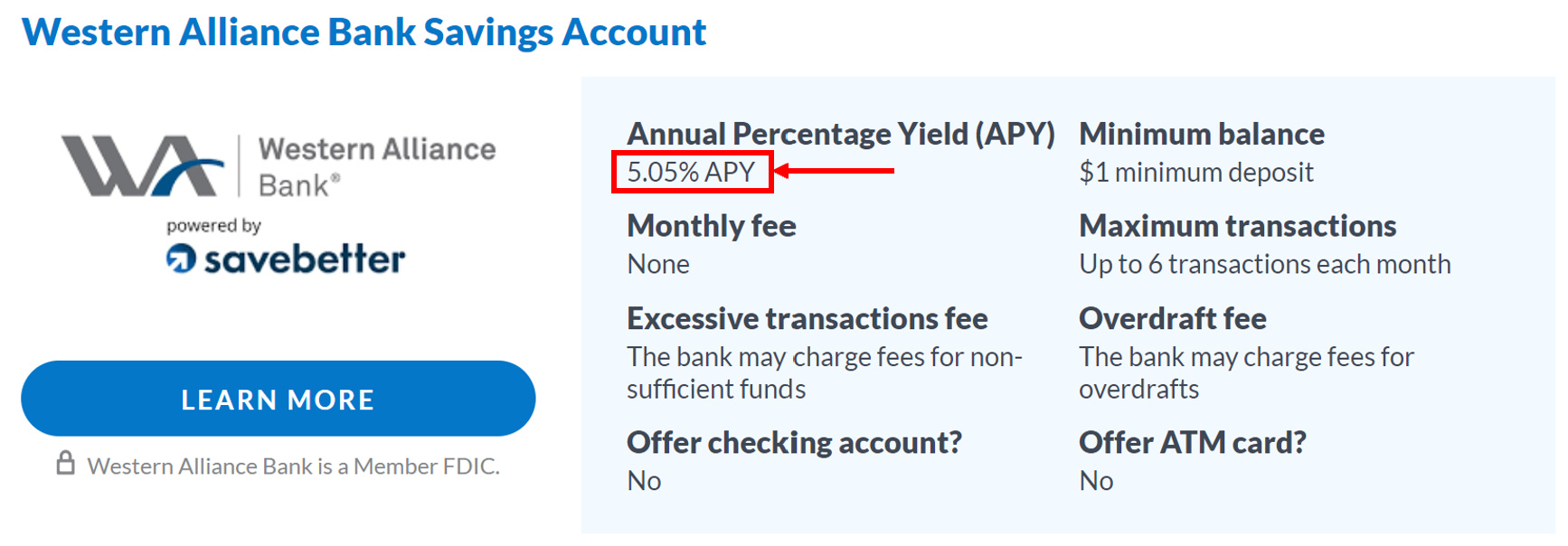

It also doesn’t add up that stressed banks Western Alliance, PNC or Comerica now offer 4-5% interest on their savings accounts, a yield so high that their business runs at a steep loss

The answer can be found in the Fed’s H.8 statement itself. When commentators refer to the end of the deposit flight, they reflected what the seasonally-adjusted H.8 tells them - a $12bn decline over $17tr deposits, not worth the mention. But are these seasonal adjustments truly accurate?

To answer that, we need to know that deposits follow their own intra-year cycle which closely tracks tax payments and payouts. In the last weeks of April taxes are due, so people wire what they owe to Uncle Sam from their bank accounts and deposits go down. The Treasury doesn’t keep that money forever but spends it later in the year (=deposits up), that creates seasonal fluctuations in aggregate deposits

So for late April, the Fed seasonally adjusts the H.8 release by adding back said tax payments. But has that been done the right way in ‘23? Let’s have a look:

Below chart shows a pretty constant seasonal adjustment number of ~$270bn over the years. Treasury General Account movements, in late April mainly caused by tax payments, however swing wildly around that number

So for 2023, the Fed again assumes a net $270bn taxes have been paid in April. However, as the economy slowed and capital gains were reduced, tax payments in ‘23 came in much lower, at $150bn. This leaves $120bn in deposit decline, 10x the seasonally adjusted number!

In other words, the seasonally adjusted data is very overstated. If we adjust the data correctly, we see the deposit flight is far from over, in fact, it accelerated

This also ties in with other sources, e.g. data for money market funds, the popular recipient of pulled deposits. Their inflows have swollen to record levels in recent weeks

Ok, so the deposit flight is worse than consensus thinks. But why is this at all relevant?

It’s simple. Banks fund themselves mostly by raising deposits, and then lend that money out to the broad economy. If the deposit base both shrinks and becomes more costly, the affected banks need to curtail their lending to avoid their balance sheet from becoming overlevered1

Now, one might wonder, this only concerns Regional Banks and not the big banks, so what’s the big deal?

US Regional Banks are responsible for ~50% of corporate bank lending and ~70% of commercial real estate bank lending. Their banking relationships have often grown over many decades, it will be very hard for a highly levered economy to digest their retrenchment.

Corporate lending is particularly critical, even though it only represents 22% of the aggregate bank loan book (with real estate 68% and consumer loans 14%). Why? Because corporates create employment

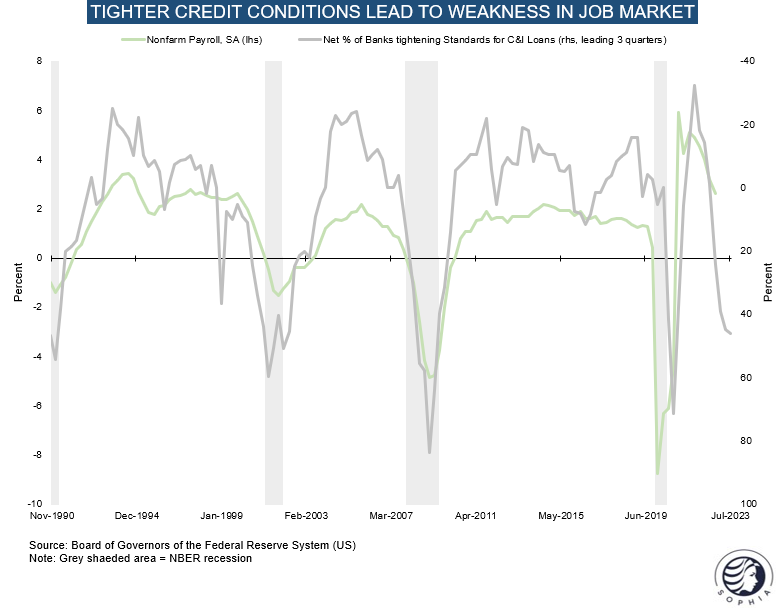

Regular readers will be familiar with my emphasis on past relationships to get predict a likely future, this applies also here

The below chart correlates lending standards to unemployment with a 3-quarter lag. It shows how over the past 40 years significantly tighter lending always predated job losses

Still, many point to continuous bank loan growth in the weeks since Silicon Valley Bank as evidence that things are “not that bad”. To that, I need to highlight two aspects:

First, the most important part of bank lending, corporate loans, has already flatlined since the turn of the year

Second, bank lending evolves with substantial lags. This is because credit is often paid out in instalments, e.g. as construction projects advance or as revolvers are drawn. The chart below shows the historical the lead-lag relationship between lending standards and loan growth - it is only a matter of time until the latter turns negative

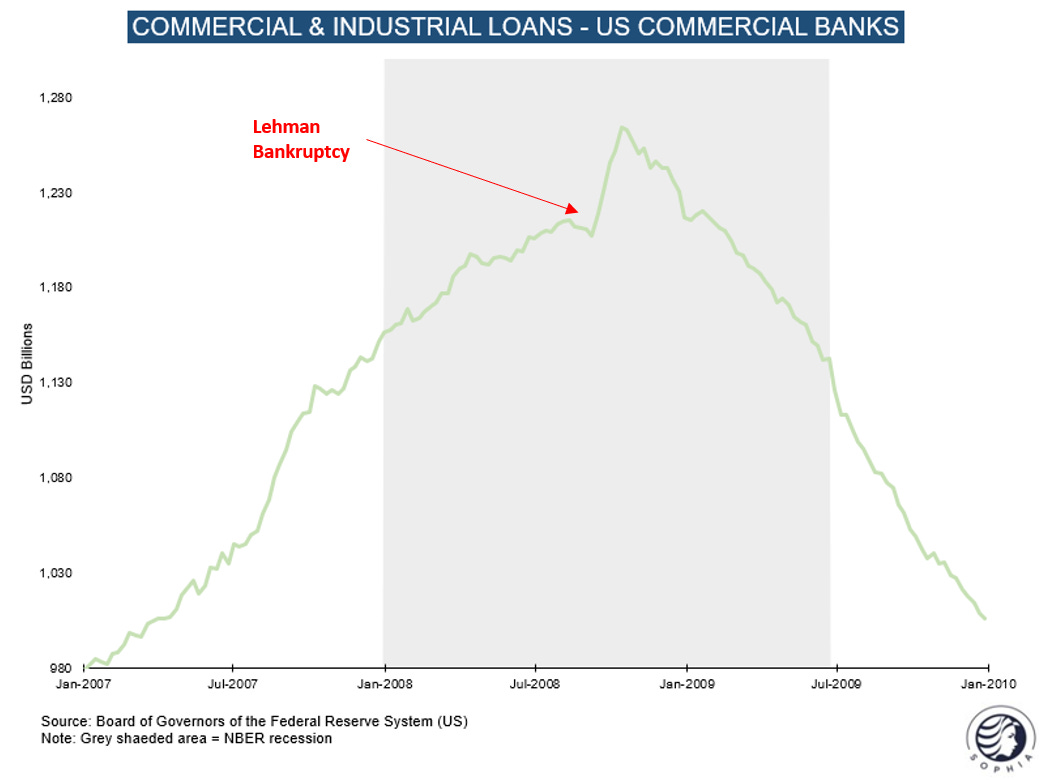

Consider this - even after Lehman Brothers went under in September ‘08, it took two months for corporate lending to contract. In fact, in the immediate aftermath loans grew as companies rushed to draw revolving facilities

Let’s return to the bank liabilities side (i.e. deposits). Why is the deposit drain such an issue for US Regional Banks, but not for JP Morgan or BofA?

The answer: Their capital base is much narrower than at the big banks. The deposit drain so far has brought Regional reserves-to-assets ratio down to critical levels on aggregate, with many individual banks already below

Importantly, deposits are not only pulled by customers fed up with 0% yields when money market funds pay 5.25%. A much overlooked dynamic is Quantitative Tightening

Every month, the Fed buys $70-90bn fewer US Treasuries and MBS than expire from their holdings. The private sector has to fill the gap from its deposits, a c. $350bn drain so far this year

This brings me to the final piece of the current economic puzzle - the debt ceiling

In late December ’22, the Treasury hit the maximum debt level permitted without further Congress approval. Since then, the Treasury hasn’t issued any new net debt, so the private sector had to send fewer deposits to the treasury. More so, the Treasury spent down its existing $900bn cash pile (to as low as $100bn in late April) which grew deposits

This was only a temporary boost. Whenever the debt ceiling is lifted, the Treasury General Account will be built back to $500bn, and that money has to come from the private sector, just as it was given to the private sector since the debt ceiling was reached

(Side note for monetary plumbing enthusiasts: Higher bill issuance is likely following a debt ceiling resolution, which means some funds may come out of the RRP. But whenever the bill surge has passed, these funds likely flow back to the RRP)

In other words, whenever the debt ceiling is lifted, a dynamic that has been a tailwind for deposits so far this year will flip to being a big headwind. This while QT is still ongoing and the consumer deposit flight continues

Conclusion:

Rather than having slowed down, the deposit flight continues at a brisk pace. No wonder - it is irrational to hope people leave their funds in accounts paying 0% while interest rates are at 5.25%, especially when they are reminded by media headlines on a daily basis

Many Regional Banks cannot afford to pay 5% on their deposit base without turning deeply loss making. Consequently, their situation is unstable. It is highly likely that more banks will fail over the coming weeks and months

This will contract lending. Lending is the lifeblood for a highly levered economy, particularly for corporates who provide employment. As a result, credit spreads likely widen substantially from here, which in turn likely pressures other asset markets

The only true solution are interest rate cuts, which the Fed cannot provide while inflation is high. As such, it is likely that the situation continues to deteriorate until enough economic damage is done so rates can be cut

Where could I be wrong

The economy could be so strong that it can digest severe damage to one of its most important lending arms → This appears unlikely to me as especially small businesses which employ half of Americans rely on Regional Bank relations. Today’s NFIB Small Business Survey speaks loudly of their increasing pains

The Fed will turn on the monetary hose (“QE”) as soon as the next bank fails, lifting the markets and all boats with it → I find this unlikely as long as inflation lingers and no broad economic damage has occured. Jerome Powell has made his priority of fighting inflation clear many times. While inflation is still around, this would also run the risk of the long end of the treasury curve selling off aggressively, a counterproductive move

Yes, the outcome is likely, but the timing is off → This could well be the case. I would point though to the reflexivity between bank equities and their core business. If Regional Bank stocks continue to sell off, it will force bank managements’ hands. As such, the timing appears to be now

What does it mean for markets?

As always, below is my personal attempt at connecting-the-dots for my own investments. Please keep in mind - I may be totally wrong, nothing is more important than risk management, and none of this is investment advice

Bonds - This asset class assumes some notable probability of an economic calamity as rate cuts are priced in from the summer and the yield curve is heavily inverted. Meanwhile, inflation swaps still forecast 3-4% CPI prints for the remainder of the year, so the pricing is unlikely due to inflation falling off a cliff. I think bonds are right - the current dynamics are unstable and a noisy resolution is likely. The 5-Year remains my favorite as it avoids the steepening risk of the 30-yr if rates are cut while inflation still lingers. And unlikely the 2-year, it is far enough out not to depend on imminent rate cuts

Equities - Stocks currently price in a soft landing as well as lower rates. In other words, they also assume that rates are cut, but that the reason for these cuts wouldn’t affect their earnings. This would be possible if inflation declined rapidly over the coming months, which is only likely if some economic calamity occurs as all inflation leads point to sticky inflation otherwise. However, said calamity would highly likely affect corporate earnings. As such, I perceive equities to currently price in a circular reference, which - in my view - likely resolves with them re-setting lower

Now, there has been the assumption that equities already frontrun a return of QE, with the pandemic memory present. In another circular reference, QE seems unlikely as long as the S&P is high (why do QE then?)

Crypto - The past few weeks have seen meme-coin Pepe surge 1300% to $1.2bn market cap, just to crater afterwards. As before, early insiders made a fortune while gullible retail investors now sit on heavy losses. I would not be surprised if the peak in Pepe coincided with a local peak in risk assets, as the liquidity needed for these pump and dumps is much more scarce today than in the meme-coin hayday. In my view, these episodes continue to be a disservice to the Crypto community as they provide the context for regulatory attacks

Gold - Similar to stocks, Crypto or the US Dollar, gold currently incorporates a decent probability of a return of QE. I find this likely premature, and would think the hurdles for more QE are likely higher than the market currently assumes, especially as long as inflation remains high. Over the coming decade however I see few alternatives to more monetary debasement, but the road to that is long

With the debt ceiling debate and more Regional Bank stress ahead, the current tranquillity in risk assets seems unlikely to persist much longer. In my view (which may always be wrong), investors are well advised to remain defensive and conserve cash, to have it available when dislocations materialise again later this year

DISCLAIMER:

The information contained in the material on this website article is for professional investors only and for educational purposes only. It reflects only the views of its author (Florian Kronawitter) in a strictly personal capacity and do not reflect the views of White Square Capital LLP and/or Sophia Group LLP. This website article is only for information purposes, and it is not intended to be, nor should it be construed or used as, investment, tax or legal advice, any recommendation or opinion regarding the appropriateness or suitability of any investment or strategy, or an offer to sell, or a solicitation of an offer to buy, an interest in any security, including an interest in any private fund or account or any other private fund or account advised by White Square Capital LLP, Sophia Group LLP or any of its affiliates. Nothing on this website article should be taken as a recommendation or endorsement of a particular investment, adviser or other service or product or to any material submitted by third parties or linked to from this website. Nor should anything on this website article be taken as an invitation or inducement to engage in investment activities. In addition, we do not offer any advice regarding the nature, potential value or suitability of any particular investment, security or investment strategy and the information provided is not tailored to any individual requirements.

The content of this website article does not constitute investment advice and you should not rely on any material on this website article to make (or refrain from making) any decision or take (or refrain from taking) any action.

The investments and services mentioned on this article website may not be suitable for you. If advice is required you should contact your own Independent Financial Adviser.

The information in this article website is intended to inform and educate readers and the wider community. No representation is made that any of the views and opinions expressed by the author will be achieved, in whole or in part. This information is as of the date indicated, is not complete and is subject to change. Certain information has been provided by and/or is based on third party sources and, although believed to be reliable, has not been independently verified. The author is not responsible for errors or omissions from these sources. No representation is made with respect to the accuracy, completeness or timeliness of information and the author assumes no obligation to update or otherwise revise such information. At the time of writing, the author, or a family member of the author, may hold a significant long or short financial interest in any of securities, issuers and/or sectors discussed. This should not be taken as a recommendation by the author to invest (or refrain from investing) in any securities, issuers and/or sectors, and the author may trade in and out of this position without notice.

This creates particular issues if Banks hold assets that are under water on a mark-to-market basis and therefore losses would be realised when the assets side shrinks, or if their loan book is low-quality and thus hard to sell - either is the case for many Regional Banks

Fantastic. I really appreciate and value your work. Thank you !

Another great article. Thanks for sharing!