Fork in the Road

A critical week for the world economy lies ahead

The coming week will be absolutely critical for the world economy as it faces a binary road that either moves it away from, or over the figurative cliff. This post explains the reasoning behind this and the investment implications

To cut straight to the chase, the origin for this pivotal moment is the Iran conflict, and in particular the blockade of the Strait of Hormuz, through which c. 20% of global oil traffic and many other essential inputs such as fertilizer, LNG or helium flow. This creates a setup akin to a ticking bomb, where every shut day causes gradually more damage, until a large rupture occurs

To illustrate this dynamic, please follow me on the below simple math, focussed solely on oil for now:

Daily global oil demand is ~105m barrels per day. Most of the oil produced in Iraq, Kuweit, Bahrein, Saudi, UAE and Iran, 21mbd in total, is shipped to global markets via the Strait of Hormuz

Oil is an inelastic good i.e. we really need it irrespective of the price. It is mainly used transportation (cars, trucks & planes) and industrial purposes (plastics, energy production)

The current flow of ships through the Strait has decline from ~140 to 3-6 per day. Thus, Hormuz oil volume has collapsed to c. 2mbd (mostly Iranian ships to China) vs the 21mbd pre-conflict. In other words, a 18mbd deficit is now at hand

However, a range of offsetting measures has been introduced. A pipeline that cuts through Saudi with spare capacity is now fully utilised (+4mbd), and more oil now flows from Iraq to Turkey (+0.5mbd) and from UAE to Oman bypassing the Strait (+1mbd). A globally coordinated release of strategic oil reserves (“SPR”) adds ~2mbd

This leaves a daily deficit of ~10mbd if counted generously. For an inelastic good this is a huge gap. Economic theory stipulates that to balance the market, the oil price would have to go high enough for 10% of consumers to give up, i.e. not use their car, halt the factory assembly line, not take that long haul flight etc. The price to do this would be very high, in particular on the industrial demand side ($200-300bbl?)

For obvious reasons, this scenario would crush the world economy and lead it into a deep recession. So why is the oil price not there yet? Three reasons:

The main reason is that there is still a lot of inventory that gets eaten into first

A secondary reason is a disconnect between paper and physical markets, and the focus on US benchmark WTI. Many refined oil products as well as oil originating in the Middle East (e.g. Dubai/Oman) are already at nosebleed levels

Markets are pricing in some odds that the conflict ends shortly

The current commercial inventory both held on tankers at sea and onshore inventories is ~260mbbl excluding China, which has its own strategic interests in opposition to the West, and still receives some Iranian oil. A 10mbbl/day deficit eats through that in 26 days (please note the SPR is already accounted for in the daily deficit number)

Now, many additional levers will be pulled and human ingenuity always goes above and beyond in crisis. Also please note these are back-of-the-envelope calculations to just give a directional sense. So this number of days could also be twice as high

Either way, it is not many days, and once the inventory is absorbed and if the conflict is still ongoing, another aggresive leg higher in oil prices as well as fuel shortages are in the cards. This may sounds hyperbolic, but consider the following: Inventory is not distributed evenly, so in many countries fuel shortages have already started, incl. Japan, Australia, Korea, India, Indonesia, the Philipines etc.

In Europe, Italy would be next in line, as it receives 30% of its natural gas imports from Qatar, which has currently shut down entirely, and where 17% of production has been damaged for 3-5 years

Summary: If the Strait of Hormuz is not opened very shortly, enormous damage will be inflicted on the world economy

How likely is this to happen? First of all, geopolitical conflicts are unpredictable, so all of the below thoughts come with a wide margin of error. Either way, this is how I see it:

At the moment, Iran has full control of the Strait of Hormuz. Since the start of the war, this has not weakened. In fact, over the past week Drone and missile attacks increased again and strikes over the past days occured in a precise manner (e.g. Qatar LNG, Kuweit refineries, Saudi Red Sea refinery), which suggests that despite all the decapitation strikes leadership coordination still occurs. I also assume Russia and China provide significant aerial intelligence help

This makes Iran the new de-facto OPEC. By deciding which ships can go through the Straits they can set the price of oil. This situation is absolutely unacceptable not only to the US and Israel, but to the entire West, against which Iran is aligned

It is highly unlikely that Iran will give up this new found power voluntarily. It also seems implausible that the Strait can be made secure from the air. After all, it only takes a kid with a drone to disrupt it, and that can occur from far away as the drone strike on the Saudi Red Sea refinery 1500km away demonstrates. This leaves the following three options from here:

The US and Israel take control of the Strait by force, on the ground

The US and Israel manage to destabilise the regime from within in short enough time before global oil inventories run out

The warring parties make a deal that ends the war, likely involving considerable concessions to Iran (e.g. sanctions relief)

Today’s reporting suggests that 1. is the most likely, and preparations for it are under way. This would be a high-risk path with many challenges, and likely considerable time and possibly casualties involved. At its end however I would think Hormuz control is achieved. Again, keep in mind geopolitical events are very fluid, and I also leave some probability assigned to 3., as unlikely as it looks today

What Does that Mean for Markets?

The following section is for professional investors only. It reflects my own strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please always note, I may be entirely wrong and/or may have changed my mind even by the time you read this. This is not investment advice, please do your own due diligence

Short Run:

In the very short-run, anything that prolonges the Strait closure is cryptonite for equity markets, as it increases the odds of the “off-the-cliff” scenario I outlined above. Even if that case may be 2-6 weeks out depending on the calculation, markets will very likely front run it

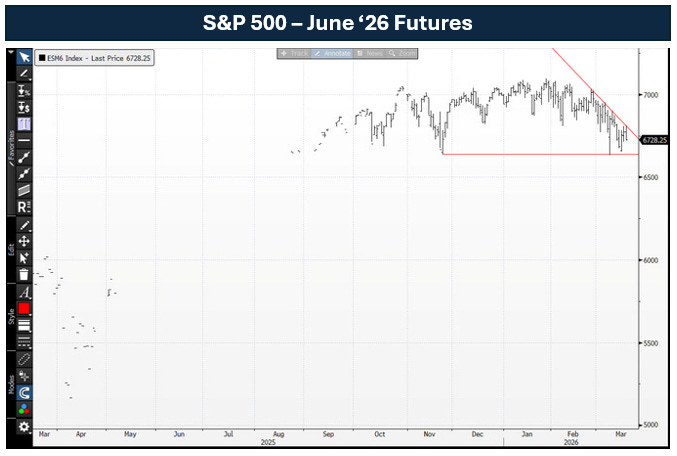

This also aligns with the technical picture, which shows the S&P 500 in a lengthy consolidation pattern since the fall (cf. Wyckoff distribution pattern), that now has a fundamental reason to be resolved to the downside

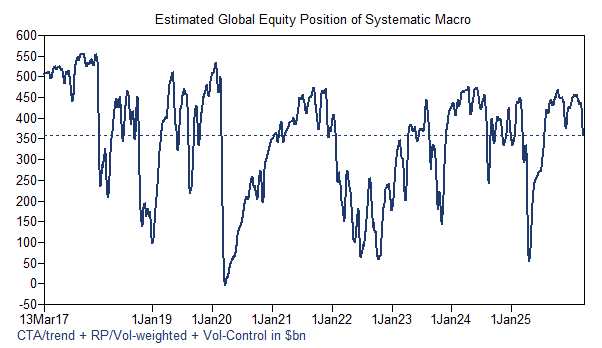

More so, while positioning has certainly cleared a fair amount, it is not at levels that are so one-sided that it is no brainer to go long. Many pockets remain with considerable net length (below for systematic hedge funds)

However, as I mentioned above, geopolitical events are both unpredictable and very fluid. Further, the outcome I describe above is undesirable for almost everyone including China, so all possible forces will work against it happening. Thus, a resolution, or a step towards it may be announced at any time. Equally, there will be many attempts to jawbone markets higher with reassuring words. I have closed out equity shorts today, and will be flat into the weekend. If the news context does not change, it will use risk rallies to re-enter these. It is not my base case (see above), but at the same time, if the news context provides a light at the end of the tunnel I will go long. As always, I may be wrong in direction, time or both, and am ready to change my views on a dime should new information warrant it

Long Run:

Equities broadly My base case assumption is that markets see a sharp correction over the coming weeks as the world moves closer to the brink. In turn, that could be the catalyst putting sense into everyone and an off-ramp is found, which may coincide with positioning so washed out that no one is left to sell, providing much fuel for an upside move I am looking to go long risk into that low

Looking at sectors and asset classes in more detail, I see the following as long-term winners from this situation:

US LNG - Mideast natural gas supplies are likely both damaged in output and reputation, with main demand sources Europe and Asia needing to turn to other sources. US LNG is the most obvious and I would expect this sector to do well

Renewables & EVs - Substantial progress has been made in partiular in Solar power generation, as well as in battery storage. This is another obvious winner for me, as well as electronic vehicles, which are more attractive again at higher gas prices while autonomous driving makes big progress

Coal - left for dead many times over the past decade, coal remains a go-to energy source for higher short term demand

Defense, in particular drones and lasers - After Ukraine, the Iran conflict has once again re-affirmed that future conflicts will be assymetric and drones are a key component in them. The flipside is laser-based air defences against them, which are much cheaper than e.g. existing Patriot systems

AI - Iran is another proxy war between the West and China/Russia. Global tensions rise, and with it the urgent need to win the AI race. Expect more government support. Focus on whatever the bottleneck is and the highest beta to it (memory, photonics today, what’s next?)

Gold & Bitcoin - While either in the short run are tied to risk-on/risk-off, in the long run war is inflationary as more defence spending requires more money printing, and the worries on governmental confiscation rise, which benefits store of value proxies

Commodities - The conflict accelerates the breakdown of the world into competing spheres. This weakens global supply chains and increases the need to hold more strategic inventory of key primary inputs

These will have difficulties:

Japan - The land of the rising sun imports most of its energy and food. It has also embarked on a highly inflationary policy mix just before the war broke out. It will have to hit the inflation breaks hard or risk a Turkey-style outcome

Germany & Europe - The old continent is facing another inflation wave as its vulnerability to energy shocks has not diminished since the Ukraine war. The silver lining could be that this creates the impetus for lasting positive change, as Europe realises it needs to rely on itself

Fantasy stocks and financial concepts - A hallmark of the late 2010s and early 2020s easy money period, it is hard to see a return to 100x EV/sales ratios for gaga-stocks and fantasy coins when liquidity is needed for commodities and defence

I’ve share my views much more closely on X, and continue to trade along the Dominant Driver Theory introduced last year. Performance continues to be good (below as before since 17th Oct ‘24) and is composed almost entirely of hyperliquid global macro instruments (ES, UB, CL, GC futures etc.)

Rather than adding to these gains, my main personal challenge from here is not to give them up, as human psychology incl. mine will work against me to induce carelessness and excessive risk taking. The FK Terminal Claude Opus let me build helps a lot in that regard, a small data excerpt below. I still intend to make an open-source version available when I get the chance for it (please note that all it does is give you structure and process, you’ll still have to do the hard work yourself of filling it with life :)

Finally: there have been some imposters and spam accounts in my name that X is slow to get rid of, please note I do not run any paid service or investment opportunity and will never contact you via whatsapp or otherwise for it

The world is in a difficult place today. I genuinly hope that further escalation is avoided, I would much rather be wrong on my short-term view than see it continue down an increasingly difficult path. My thoughts are with all those affected by the war one way or another

very timely, very nuanced; excellent analysis. Thank you!

Excellent work. Thank you for sharing.