The Digital Gutenberg Moment

Without hyperbole - why things may never be the same

It has been a few weeks since I wrote my last post in late December. A lot has happened since in particular in AI, where some developments have opened the door to what I believe may be a spectacular new period

Around 1440 in Strassburg, Johannes Gutenberg invented the printing press. This greatly facilited the proliferation of documents which before had to be copied by hand. In my view, the release of Claude Opus 4.5 late last year marks a similar moment, where the ability to generate software moved from costly, labor & time-intensive to cheap, effortless & quick, thus enabling a dramatic shift in access and proliferation akin to the printing press at the time

This opens the door to some major changes to the fabric of our economies and markets, which this post walks through, as always along the lines of the Dominant Driver Theory

Perhaps the best way to illustrate the significance of this moment is through personal experience: I know as much about coding as I do about cooking, to my wife’s great lamentation

Yet, since downloading Claude Opus 4.5 in early January, I have managed to create an investment terminal ideally tailored to my needs. It now replaces my Bloomberg account for most tasks and, more importantly, performs many other tasks that were previously not accessible

More so, having worked with developers before, I was used to lengthy feedback loops between the idea and implementation and a big bill at the end. The work with Claude on the other hand was as effortless as conversing with a developer, but cheap and with immediate results, as coded files are returned within minutes

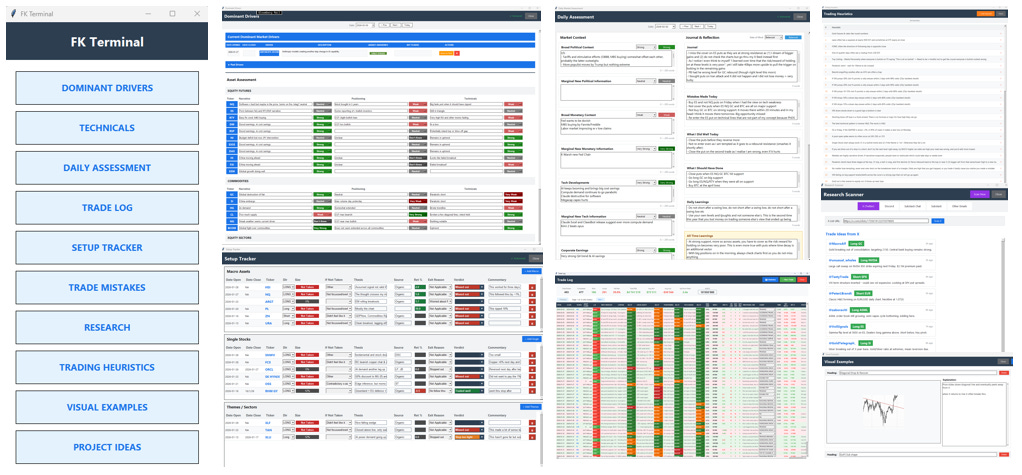

Thus, in the space of a few weeks I was able to build software that (at least for me personally) has huge value and even 6 months ago would have taken several months and hundreds of thousands of USD to create. Here are some more details on the “FK Terminal”, starting with some screenshots below:

The column on the left with the light blue fields is the main menu. Each button opens a tab as some of them are shown on the right. Each tab in turn fulfils a function supporting the Dominant Driver Theory investment approach I pursue, let’s briefly walk through them:

Dominant Driver Tab: This logs the current and past market moving themes with accompanying analytics

Technicals: The charting module (more below)

Daily Assessment: A key part of my investing approach is “radical journaling”, the process of noting down every possible detail around a trade, from technical and fundamental elements to personal observations suchs as mood or sleep quality. This module allows me to do that in a structured way, with daily and all-time learnings extracted every day

Trade Log: This files all my trades including their reasoning across multiple vectors. The adjacent trade statistics allow me to sort for each of these vectors to easily detect what worked over time and what did not - a key improvement engine

Trade Heuristics: Here I store all the conceptual market relationships that have shown valid time and again (e.g. “Staples and Energy rallies often precede market downside”, see more in market section)

Trade Mistakes: Macro investing is akin to trying to make a thoughtful decision while you are getting punched in the face, so very error prone. I file and dissect every error here diligently as another improvement flywheel component

Research: I could never read all of the my over 70 email subscriptions which I all rate for one reason or another, and many other sources on top. This module summarises all incoming information in a digestible way

Setup Tracker: I track every trade setup I see and the reasoning around why I take it or not. This is a great and objective way to tease out behavioral biases

Visual Examples: I often come across the same technical pattern, whether it is on an intraday, daily or weekly chart. Here I save images of what I feel frequently repeats, which over time creates a library of patterns I can use for comparison

Now, as you can already tell, this all resembles an external brain/memory/ knowledge storage - whatever you want to call it

As my biggest investing bottleneck is bandwidth and information absorbtion, this is of course very useful, yet nothing groundbreaking on its own

However, what takes it to another level is that AI introduces the recursive learning ability. With enought input, the machine can learn my investment style, and start to proactively assist, and eventually perhaps even replace me :) A good example is the technical analysis component:

This is a key part of my investment process as I rate very highly the information the market provides us via price action. I apply classic pattern analysis on it. However that takes time, and I can only look at so many assets until my bandwidth is maxxed out

In order to expand, I am training the terminal to read charts like me. The red box at the bottom with the arrow counts the # of samples the machine needs to replicate my technique both (1) via standard coordinate settings and (2) via image recognition, i.e. a neural network. So over time, the machine will have seen enough examples from me to read them the same way, and I can have it go through 1000s of assets instead of the currently 120 I scan every day

Given the very high number of datapoints involved in the Dominant Driver Theory approach, there are many other AI feedback loops that eventually apply

These range from a co-pilot that highlights possible mistakes before they occur to trade recommendations or automated overnight trading (I also need to sleep…)

Important: I intend to the make the FK Terminal, or parts of it, available either as a download or opensource for free. Please give me some time with that as that involves more steps than just getting it to run on my computers. It also requires some API connections that can be set up easily

To come back to the introduction- I was able to do all this with no coding experience, no developer team, little money spent and only limited time avaible. It did this with an AI app that is already outdated (Claude Opus 4.6 came out yesterday, and recent Kimi 2.5 performs better in many tasks). I have not taken advantage of the latest AI agentic bleeding edge developments

Now, imagine what all these possibilites mean for the real economy. Let’s have a look at that in the next section

Current Dominant Drivers for Markets

Enterprise AI

It is hard to overstate the implications of what I illustrated above. Here are some that come to mind:

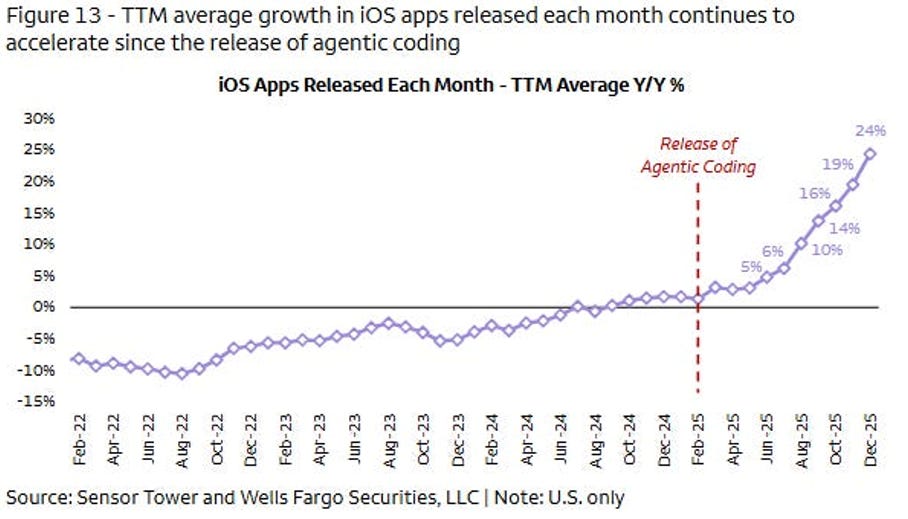

Business formation will likely go through the roof. Never has it been easier to create something that can be useful for others. We can see that already in growth rate for iOS apps which has exploded over the past 12 months

The AI cost saving curve for traditional businesses I discussed in several past posts goes on an even steeper leg, and the pressure to implement these will be VERY high - never has the first mover advantage been greater as so much difference can be achieved in so little time

However, the code and agentic breakthroughs open the door to a new, possibly even larger dynamic:

It has now likely also never been easier to attack an existing business

What do I mean by that?

The US economy in particular is shaped by oligopolistic structures across many sectors. Many incumbents sport very high margins, but their customers have long been less than excited about the product and service, often with no alternative to turn to. From FICO to Expedia, from Salesforce.com to Microsoft Office, from LexisNexis to Bloomberg in my example above

While the market for the past months has focussed on the “AI Winner” trade, a new dynamic is now in its early innings and will likely stay with us for some time - “AI Creative Destructuion”

AI Capex

The initital read from all this is that AI compute demand from here only goes up. So the US Tech Megacaps have once again hiked their capex forecasts, e.g. Google from $91bn (FY25) to $185bn (FY26) or Amazon from $125bn to $200bn

However, as model competition remains intense and cheap and compute-efficient Chinese open-source alternatives pour into the market (e.g Alibaba’s Qwen 2.5-VL that runs on your phone), investors continue to doubt the ability to monetise these gargantuan numbers

A comparison with the US shale boom comes to mind, where US oil companies invested hundreds of billions into accessing more complex US onshore oil deposits from ~2010-2020 which ended up great for the consumer as it depressed the oil price, but left equity and debt investors with negative returns

At the same time, Megacap capex comes at the expense of their buybacks which until now had been a significant demand source for US equities

AI capex remains a headwind for US Tech Megacap, with some growing risk that low-cost models open source models bring return potential down even further

What Does that Mean for Politics and the Economy?

The fast AI advancements pose tremendous opportunity and challenge. We may be very close to some incredible scientific breakthroughs, from curing cancer to slowing or reversing aging. At the same time, the risks are high that economic change occurs too fast. Job cuts this January were the highest since 2009 and Job Openings (JOLTS) are dropping like a rock, with AI cost savings no doubt playing a role. The following two scenarios cover both bookends of the range of possible outcomes:

Business formation creates many new employment opportunities. AI wealth gains are spread enough to create societal discontent. Scientific breakthroughs lead to significant deflation, bringing down the cost to access high value services and products The historical equivalent of this is the post WWII period and the producivity boom enabled by better transport, refridgeration and industrial tools

AI-related employment losses happen too fast to be absorbed elsewhere. AI wealth gains are highly concentrated while AI costs (e.g. energy) are socialised. Societal discontent rises, and with it populism, inflation and ultimately conflict The historical equivalent are the 1920/30s

We need to remain open-minded to either outcome. Perhaps most likely is a combination of all of the above

What Does that Mean for Markets?

The following section is for professional investors only. It reflects my own strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please always note, I may be entirely wrong and/or may have changed my mind even by the time you read this. This is not investment advice, please do your own due diligence

Let’s tie the themes together for their investment implications

In my last post, I suggested that equities would see weakness early in the year, ROW and Europe would outperform the US, oil should be traded from the long side, volatility would go up a lot and the low in crypto would not be in yet, the CHF could be the safe haven from USD debasement and bonds should be traded from the long side

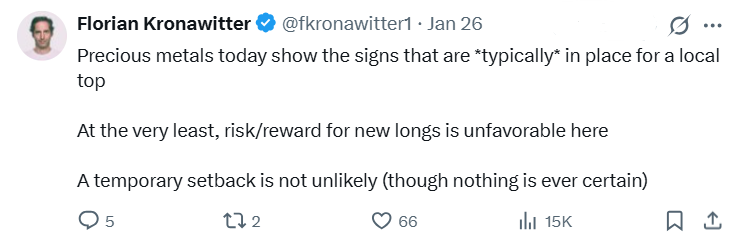

I’ve also shared this on precious metals the day Platinum, two days before SIlver and three days before Gold peaked:

These views largely turned out to be correct, which of course may also just be coincidence as I have been wrong many times before, e.g. earlier this week with calling for a low in Software too early. Further, bonds have gone nowhere

Either way, I have traded these view within the Dominant Driver Theory which continues to work (below as before since 17-10-24). You can see quite well on the equity curve when I started using the “FK Terminal” in mid-January. I would say one of the biggest benefits so far is higher trade discipline and broader trade implementation

My updated views by asset class:

Equities

On the one hand, it appears that many active market participants have turned quite bearish this week, as levered ETF selling has been the highest since April ‘25 and Bitcoin went through a collosal sell off which looks like it may have found a local low at 60k last night. On the other hand, there is a long list of technical observations that usually occur before major drawdowns, with the extreme outperformance of Energy and Staples (XLP) as in the chart below as one example

As of writing this, I am currently still long some residual US equities index positions set up yesterday (see here), but I believe we must be open to the posibility that if we get a bit of a rally here it may just be short cover, and we reverse lower again once that is done. Retail, CTAs and vol control are still very long, and the market has turned on US mega cap capex spend, now perceiving it as an issue rather than a positive. Thus I plan to exit these soon and initiate downside bets again if/when that short cover squeeze is done, for a more climatic low perhaps later this year Please keep in mind as always this may change, or simply be the wrong read and something totally different may occur

Given the reflexivity between the US stock market and the US economy (“wealth effect”) as well as a weakening labor market, it would not be a huge surprise if economic data eventually also gets hit, which could then trigger a very aggressive and thus bullish policy response

Precious Metals

Big picture, the supportive structural trends remain in place. However, volume was very extreme at the highs before the big drop, which means that many or even most (!) market participants are currently under water as they all bought at the top. Whoever hasn’t been stopped out from this group may be glad to use any rallies as exit opportunities which could weigh on the space for some time

Oil

I remain constructive on crude. However, any longs face downside risk from Iranian oil coming back onto the world market, e.g. if the regime collapses due to intervention or on its own, so I continue to see this as a market to be bought on dips

Bonds

I expected Bonds to be a long on weakening labor market data in my last post. This has not really happened until yesterday, and there are also some crosscurrents e.g. potentially higher energy prices or tariff-related price hikes for goods at the start of the year. My bias remains for long end yields to go lower but this is a lower conviction view

US Dollar

I believe there are too many US Dollar bears right now for the Greenback to move lower for now. Once that positioning has cleared and new policies are introduced we could go back to the debasement path

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

Very impressed by FK Terminal and excited to try it! Quick question: do you see “capital repatriation to RoW” as a dominant driver right now? If not, what makes you skeptical?

The idea that trumps recent policies (Greenland, Venezuela etc.) are prompting countries and individuals to reassess an overweight to US equities seems plausible. South Korea even introduced tax incentives for capital repatriation. Cross-asset moves seem to confirm this: DXY looking weak and recent outperformance from equity markets with large net international investment positions versus the US. For example, VEU/SPX has shown notably bullish price action. Am looking to go long RoW here.

Great article! However, would caution against extrapolating your own high agency to rest of the world and the common person, there has always been tools available for those who have the will. Similarly, coding itself has never been the obstacle to the creation of a great (software) company...