Terra Incognita

Three scenarios for the economy and markets, and which one I think is the most likely

The US economy is the pacemaker for all global activity, yet its future trajectory has rarely been subjected to such divergent debate. This comes as no surprise: Today, the set of dynamics driving the US economy are entirely unprecedented in their combination. In particular:

Fiscal spend runs at a record outside of crisis and war, a hallmark of inflationary Emerging Markets - yet contrary to the typical examples, its society is aging, and labor force growth has stalled. The record inflation of the past two years was surely due to trillions of printed money - yet some of it was clearly pandemic-related, with some supply chains only now fully re-established. Add to it an emergent technology that could entirely change the way we work, and reflexive feedback loops between the economy and markets that have accelerated with the near-perfect dissemination of information

With no historic comparable, many intellectually compelling cases are currently made for the path ahead, turning economic forecasting into a confusing cacophony of views, which more often than not seem to reflect personal bias or political views. Today’s post groups these range of views into the three main scenarios. I then attempt a synthesis of what I believe is most likely to happen (hint: there is some merit in all of them)

As always, the post closes with my current outlook on markets, where I explain why my biggest position is now the 2-year/30-year US Treasury steepener

Let’s start with a summary of the three main competing narratives as I see them:

REACCELERATION

Synopsis: The current slowdown in economic growth is transitory, to pick up again in the coming quarter

Reasoning:

With ultra-low mortgage rates locked-in during Covid, high cash balances and a tight labor market guaranteeing strong wage growth, Consumer finances are in good shape. They should pick up spending again soon after the current lull, which in any event is moderate

Further, high fiscal spend pours fuel on the flames of a still too hot economy. The Fed is either absent or unwilling to be serious, so the economy will keep running near or above potential

More broadly, geopolitics, deglobalisation, mass retirement of baby boomers and underinvestment in energy supply drive inflation structurally higher

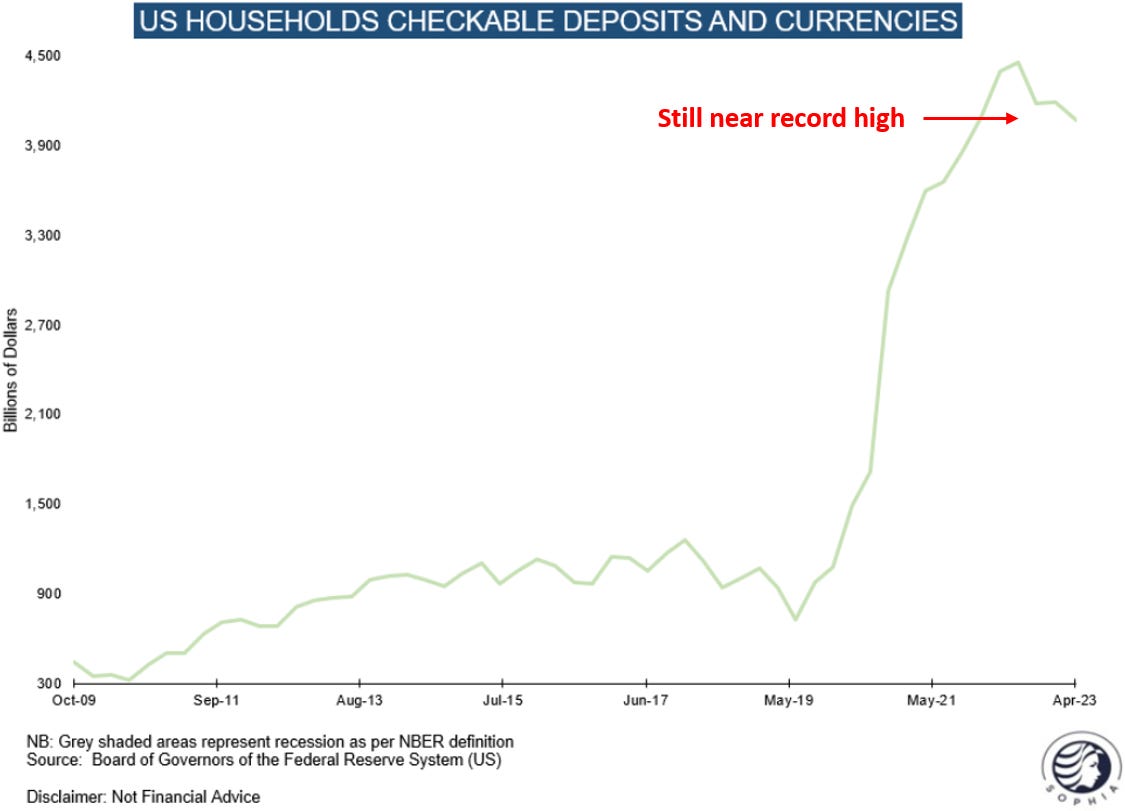

Key chart:

Household deposits remain at historically high levels, suggesting plenty of funds available to spend

Pushback:

Not all households are the same. Some are clearly in less good shape, as credit card delinquencies for younger demographics show. These are rising fast to levels not as high in a decade

Economic as well as inflationary momentum is clearly down, and the economy usually moves like a tanker. It likely requires external impetus to pick up growth again

Investment implication: Long Equities, as earnings increases outweigh multiple decline due to higher bond yields. Short Bonds, as fiscal spend is inflationary

SOFT LANDING

Synopsis: Economic growth is slowing down, but the US will be able to avoid a recession

Reasoning:

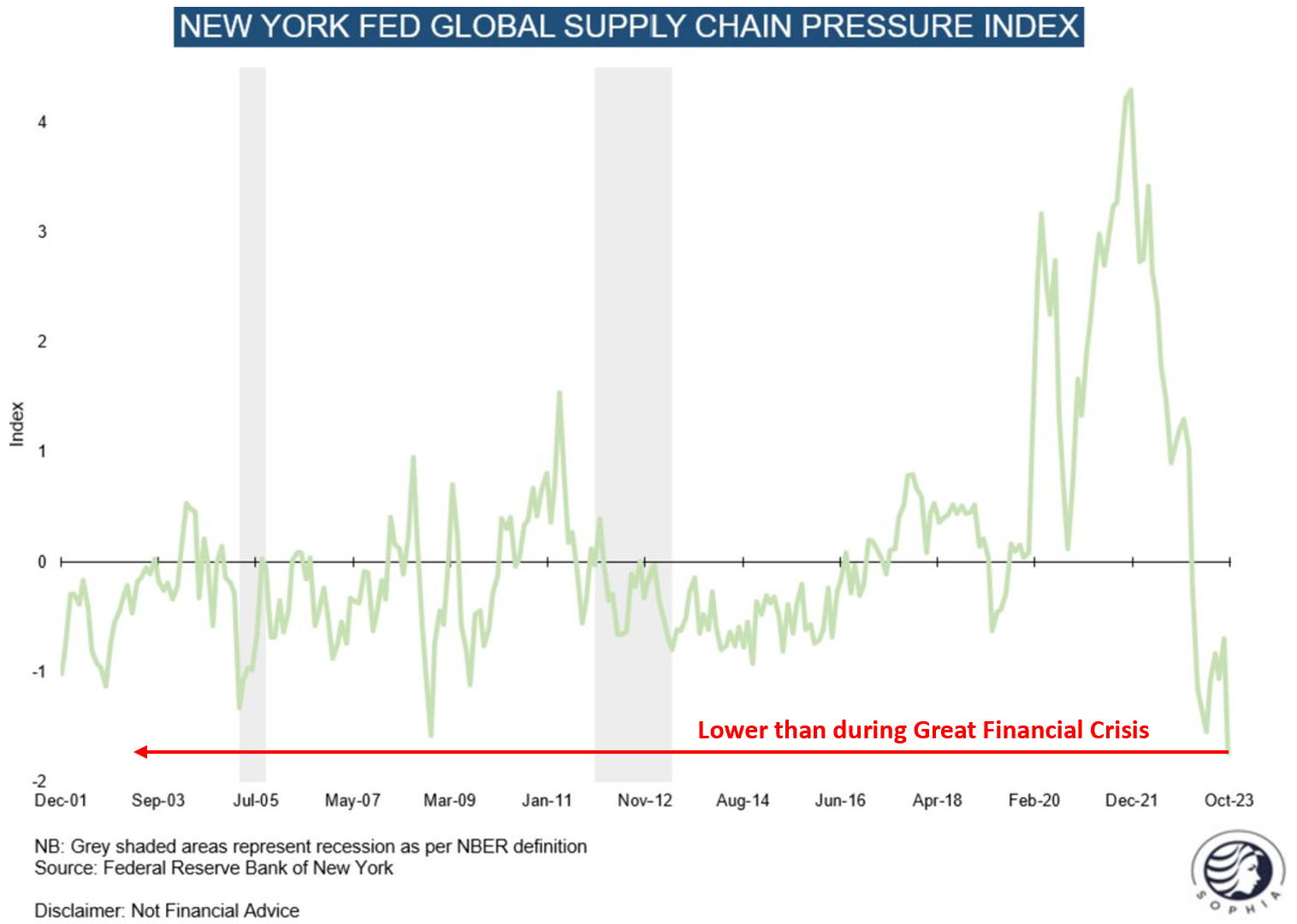

Inflation has declined to target, especially if current rent growth rather than the lagging official OER-method is applied

This gives the Fed ample room to cut, which will prevent the slowdown from turning into a recession

Inflation is unlikely to return as fiscal spend merely compensates for broader deflationary trends such as demographics or AI

Key chart:

Pushback:

Soft-landings are historically rare, with only one out of five “attempts” successful in recent history (1995)

This might require the Fed to cut rates pre-emptively, i.e. before data shows a slowdown, otherwise real rates drift too high and cause economic damage. But doing so invites inflation back

Investment implication: Long Equities, as earnings see no or only a small decline, while multiples benefit from lower bond yields. Long Bonds, as these adjust to a low-inflation world

RECESSION

Synopsis: The US economy has already entered, or will go into recession in the coming 1-2 quarters

Reasoning:

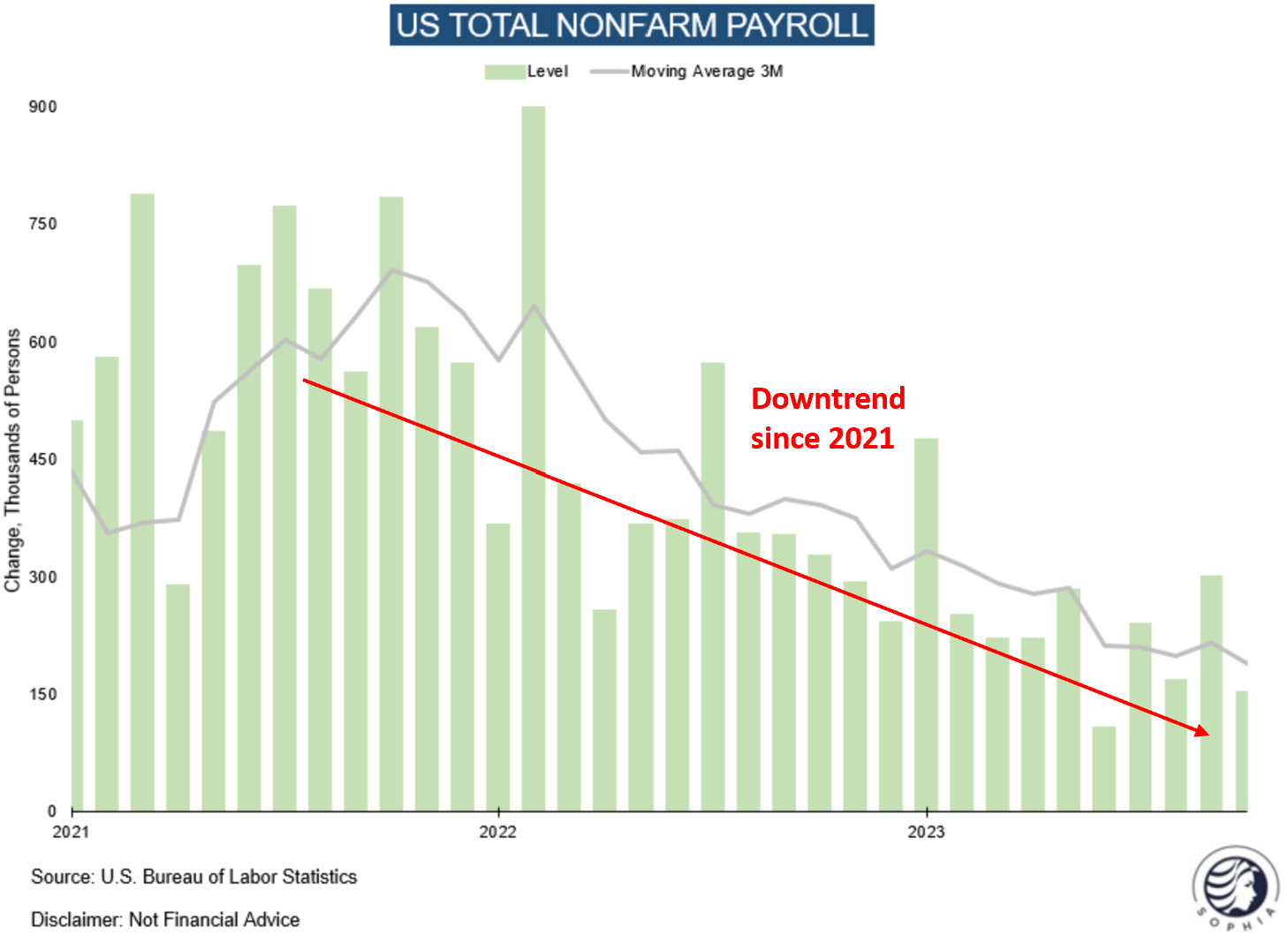

Labor market trends indicate a breakdown soon. Labor hoarding is taking place across corporate America due to “money illusion” (=high nominal revenues), so the labor market is less tight than commonly thought

Corporate margins are getting crushed by a slowing top line, while especially labor costs stay high

The Fed’s ~5% interest rate increases haven’t shown their full effect yet (“the lags of monetary policy are long and variable”)

Key chart:

Pushback:

With a 6-8% government budget deficit for years to come, how can the economy possibly fall into recession?

Solid household finances make a severe leverage-driven downturn such as ‘07/ ’09 unlikely

Investment implication: Short Equities, as earnings decline more than stocks are supported by lower bond yields. Long Bonds, as interest rates are cut

So which one is it? Here is my view, but an important thought first:

The relationship of economic forecasters to markets and the economy resembles the metaphor of the blind man and the elephant. Unable to see the entire picture, each observer describes a part that may be quite different from the other, so each can come to vastly different conclusions. But if all observations are taken in synthesis, a coherent picture emerges

In other words, all of the above scenarios likely describe a partial reality, and each contain some truth. This is my attempt to find a common thread amongst them - the synthesis:

It is likely that the structural inflation drivers indeed have changed. Its baseline should likely be higher for the coming decade

However, the economy is clearly slowing, and while household finances are overall robust, some are clearly stretched. This should weigh on consumption in the near term

With slower consumption but costs staying high, corporate margins will be likely be under pressure, and some corporates will likely respond to that with layoffs. These could lead to a recessionary period in the coming quarters

With rates at 5.25%, the Fed does have ample room to cut. This should quickly provide stimulative to the economy. The housing market in particular comes to mind, where supply is tight despite the very high current mortgage rates

Summary: A slowdown seems likely as some consumers and corporate margins are squeezed. This could lead to employment losses and a recessionary period. On the bright side, the Fed likely has ample room to respond to this in a constructive way. In response, a return of inflation at a later stage seems likely as the structural drivers for it have changed

Now, despite all efforts to remove bias, my synthesis might still be subjective or miss important elements. But there is another way of corroborating this - by listening to what the market tells us. It is the best economist, after all

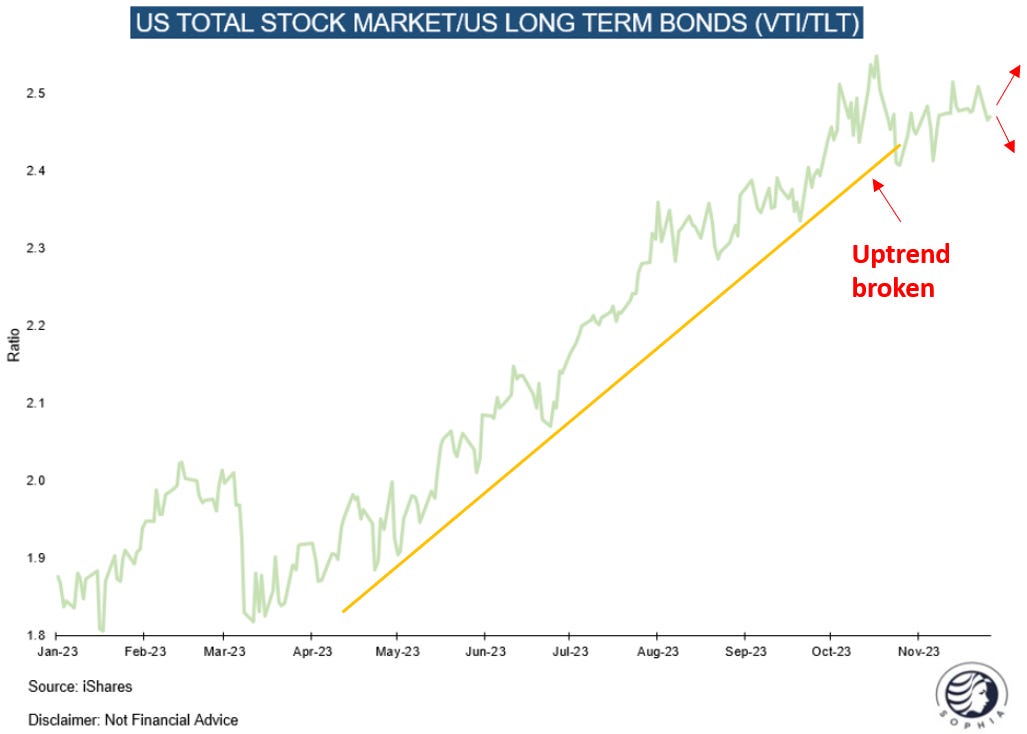

For this, in particular, there is one chart that I pay great attention to: The ratio of stocks vs bonds, as measured by VTI (US total stock market cap) vs TLT (long duration US Treasury bonds)

This ratio has consolidated for some time. Whatever it does next will tell us what regime we are in - as outlined above each scenario has different implications for stocks and bonds:

If this ratio goes up strongly, then stocks are vastly preferred over bonds = reacceleration, Fed absent, fiscal dominance

If is goes somewhat up or sideways, then stocks are roughly equal to bonds = soft landing, bonds do well and stocks do well

If it goes down, then bonds are preferred over stocks = recession, bonds do well and stocks do poorly

Now, most investors have made up their mind, and according to this recent Merrill Lynch survey expect stocks to do better than bonds (= soft landing), with the highest degree of conviction in the survey’s albeit short history

This makes me think that view is probably close to priced in, and the odds of something else happening may be higher…

On listening to the market, I also look at what the S&P 500 is doing, which appears to be at a critical juncture, as stated in my last post

After the impulse November move, the index sits right at the downtrend from the Covid-19 bull market highs. Will it run into resistance here or break through? I think whatever happens here will be informative

Conclusion:

The US economy faces an unprecedented combination of dynamics that renders forecasting via historical analogies futile. Several possible templates deserve merit

There is likely some truth in all of them. A possible synthesis would be that the structural drivers of inflation have indeed changed, but it seems clear that the economy is slowing as some consumers cut back and corporate margins are squeezed. The Fed likely has much room to respond, which may keep any recession brief. Inflation is likely to pick up again at a later stage

Either way, the market will give us more clues soon. The ratio of stocks to bonds warrants particular attention, as does the S&P 500 right at the Covid-19 downtrend

What does this mean for markets?

The following section is for professional investors only. It reflects my own views in a strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please see the disclaimer at the bottom for more details and always note, I may be entirely wrong and/or may change my mind at any time. This is not investment advice, please do your own due diligence

The economy and markets appear at a crossroad, with a moment of decision between several competing scenarios imminent. How have I translated the above into my own investments?

To start, as laid out in my last post, this past Friday I sold all my longs as the risk-reward on them appears unfavorable, at least until we know how the dice fall

I still have the long Yen position, which I wrote about in “Land of the Rising Yen”. A dovish Fed seems to juxtapose against a more hawkish BOJ

I have also bought a small amount of March expiry equity index put spreads. This is not because I believe in them, but mostly because they are exceptionally cheap now, so the risk-reward on them is compelling if you equal-weight the scenarios in today’s post, and only in 33% of cases see equity downside from here

After Fed governor Waller’s dovish comments yesterday I added exposure in oil majors yesterday, to which the equity put spreads can work as hedge, as well as some TIPS

Further, I bought some Gold puts as the shiny metal had a tremendous run and now everyone is excited about it, as Jason Shapiro points out. This could indicate some mean reversion is due, while real rates are still competing at 2%

If the S&P convincingly breaches the trendline shown above, I may add back some of the calls I already held in the out-of-favor areas

Finally, I had mentioned the long German bunds idea in my last post, but the price ran away from me. Instead, I have bought the 2-30 steepener in the US, so long 2-year and short 30-year US Treasury futures (~6:1 contract ratio). As this trade covers several scenarios and my general lean well, I have put it on in size:

Should the economy reaccelerate, then the curve likely bear steepens as the long end rises more than the short end

In both a soft landing and a recession the Fed will likely cut rates soon, and if it does, it likely does so meaningfully (otherwise what’s the point?). At the very least the curve should disinvert by front end yields coming down. Huge long end supply is still looming in ‘24, and if the Fed is seen as too dovish, the long end may stay pinned or even move up

Only when the Fed is very hawkish while the economy slows significantly should the curve invert meaningfully further. I find that unlikely in an election year and with very little societal tolerance for higher unemployment (understandably so)

As you can see, this set of positions is in some ways contradictory, but offers optionality vis-à-vis a range of possible outcomes, hopefully with a good risk/reward in each. It reflects the uncertainty of an reflexive, interdependent economic world, while aiming to benefit from positioning that in each instance possibly appears too one-sided

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

great read. thanks for taking the time to share with us.

As always, I enjoy your analysis. I think we are in unchartered waters. The deficits and the debt continue to explode and JPow doesn't want to be Arthur Burns. Therefore, he stays higher for longer. The last Treasury auctions were weak in my opinion and likely to get weaker. The Pivot scenario plays daily on TV and the average investor can't get enough. We are in the strongest period of the year, historically, so a rally into year-end is a decent likelihood. Next year is an election year and some sort of easing is likely. While gold has had a great run, despite high rates, it's under owned. If you are not a nimble trader, the risks outweigh the rewards in my opinion. A 5% yield on cash is a pretty good risk free rate!