Will it Hold?

Why some recent labor market trends are concerning

While there is currently little doubt that the US economy is slowing, the degree remains to be seen. The deciding factor will be the labor market. If it breaks, the slowdown very likely extends into a recession. If it holds, the slowdown will likely be shallow and transient

Why is the labor market so decisive for the future path of the economy? Reflexivity, the recurring theme of these posts, is at work again as negative feedback loops set into action once employment weakens: Fewer salaries mean lower consumer spend. Lower consumer spend means lower corporate revenues. Lower revenues mean further job cuts, and so on

Today’s post reviews most recent labor market trends and explains why some alarm bells should be ringing at the Fed and the Government - the only two parties that can both slow spread of unemployment and aid those affected. It also spells out why a benign outcome may still be possible, and why the risks are high this time, should unemployment indeed begin to rise

As always, the post closes with my current outlook on markets. I explained in my last post that it seemed unlikely the market would already done with the US Treasury bond supply issue, which is why I exited the longs acquired for last week’s short squeeze and tilted bearish equities again. Last night’s near-failed 30-year auction appears to confirm said view, for now

Last week, as on every first Friday of the month, the Bureau of Labor Statistics issued its latest Non-Farm Payroll report. It summarises the US employment situation for the preceding month, and is one of the most closely watched economic gauges by global markets

While the headline number +150k new jobs for the month was reassuring, various trends under the hood tell us it is first NFP report since Covid-times with reason for concern. Let’s dive in:

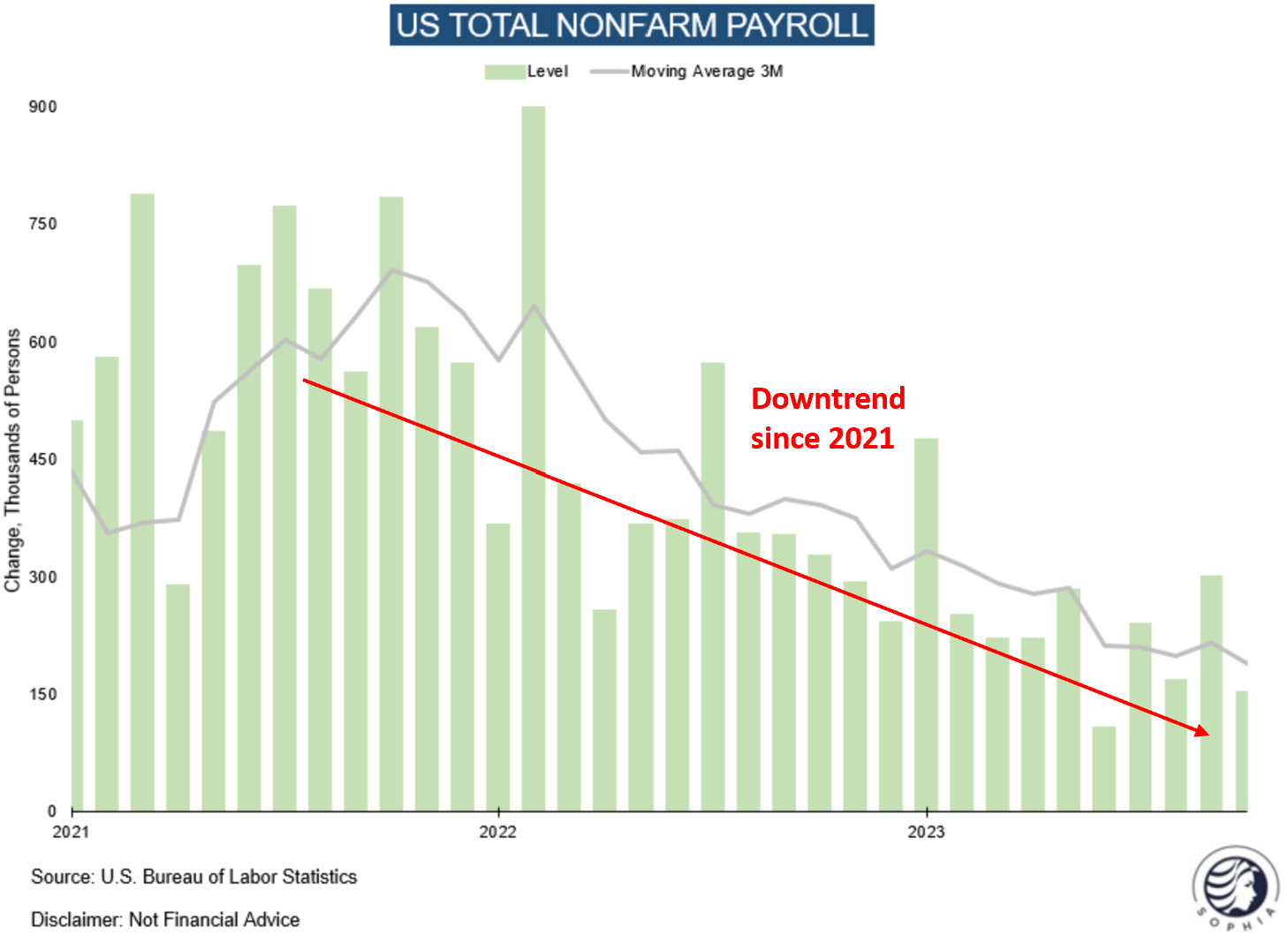

To start, while the number of jobs added still looks healthy, the job addition trend over the past two years is clearly down. If we simply extrapolate it, we’d probably end up with a negative print in 1-2 quarters

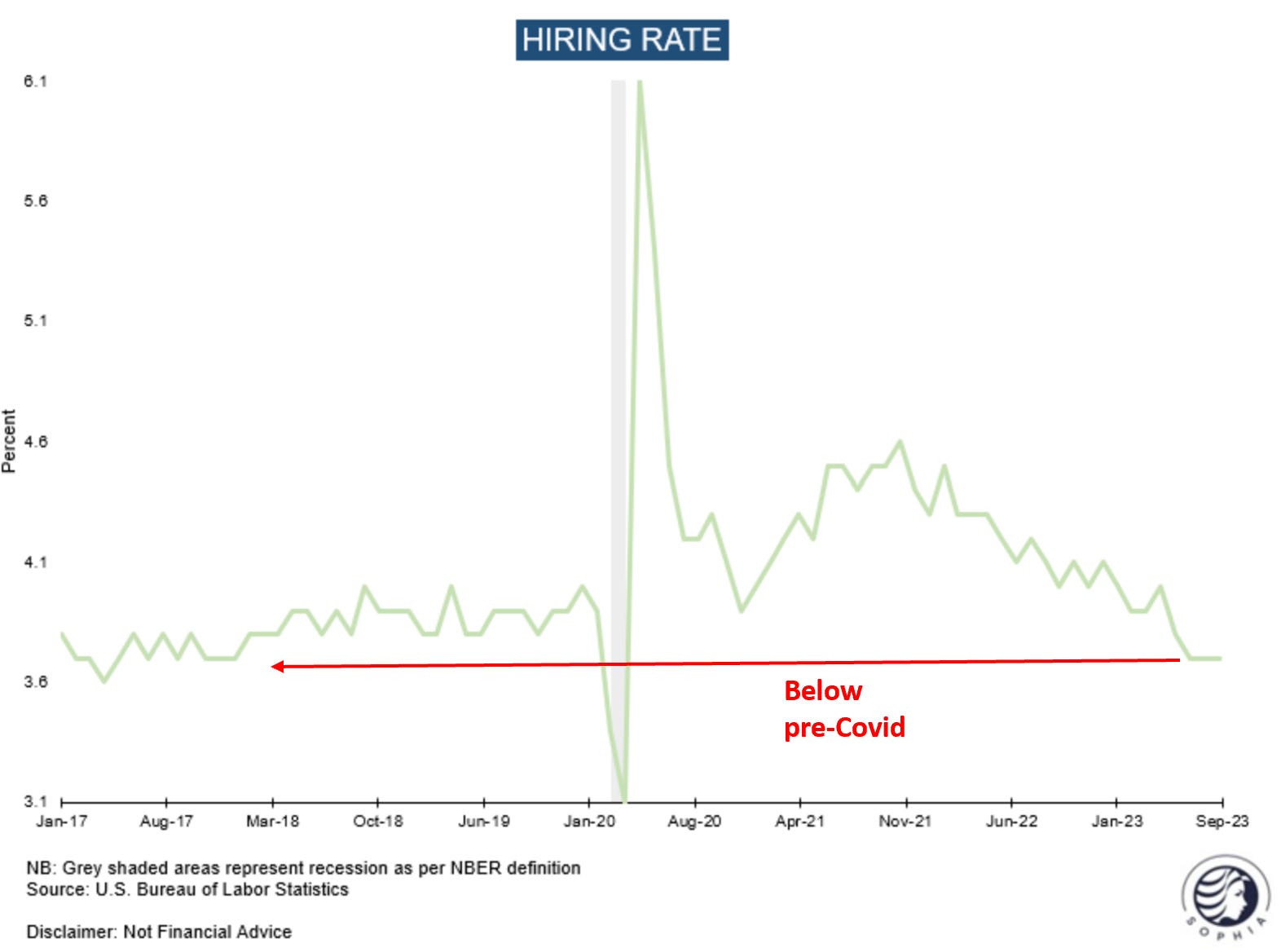

Moving from the headline to the details, the hiring rate stands out. Companies are now recruiting new workers at a slower pace than pre-Covid

The main reason why this doesn’t translate into weaker employment is that the layoff rate still hovers near a historic low - very few are also getting fired. This has lead some to speculate that companies are currently engaging in labor hoarding

This theory goes as follows: After Covid, many companies had a hard time finding staff, so now they are hesitant to let some go even though they’re not needed anymore. The phenomenon would not be new: Labor hoarding could last be observed in the the inflationary 1970s, when employment weakened only very late into the 1973/1974 downturn. But then, it all poured out at once and unemployment shot up sharply

Further details lend some support to that thesis. The share of long-term unemployed has risen steadily over the past year. With fewer hires, it gets harder to find a new job. Historically, outside of 1970, similar changes always coincided with a recession

Similar applies to youth unemployment, which has also moved up significantly. Young people mainly work part-time or in entry-level jobs, so these are the easiest for companies to shed

In the past, both long-term and youth unemployment were trends that moved up a lot, once they move a bit. This also applies to the unemployment rate more broadly given the negative feedback loops mentioned in the introduction. Below chart visualises this dynamic well:

Summary: While job additions are still positive, long-term unemployment and youth unemployment trends run at a pace that historically preceded a recession. The trend in the overall unemployment rate is on the cusp

But what happened to the super-tight labor market referenced as recently as some months ago?

Yes, job openings are still historically high and an encouraging sign for labor demand. How can we reconcile this with tepid hiring? Skills or geographic mismatches could be the reason, as could be stale advertisements

Wage growth could be an indication that job opening misrepresent labor market strength. According to some measures it is trending down fast, and lower than it should be according to the number of job openings. As measured in NFP data, it is now in line with pre-GFC levels

Now, wage growth is difficult to track and best done by triangulating various measures. The highest quality one of them, the AtlantaFed wage tracker, is still running at elevated levels, but also pointing down

For further clues, let’s take a a closer look at an industry that has driven in particular blue-collar wage growth over the past two years - Hospitality. Wage growth is coming down quite fast here, possibly a lead vis-a-vis the aggregate

So what does this tell us - Is the absolute level of wage growth still strong, and thus indicating a healthy labor market? Or is it about the trend, which is clearly pointing down?

I think whatever the data says, the vibe has definitely changed. Last year, journalists paraphrased the state of the labor market as the “the Great Resignation”, with employees jumping ship to an unseen degree to capture better pay

This has now moved to “Employees that aren’t Quitting”, as per last week’s widely circulated Wall Street Jounral article

Applying some common sense to this, wage growth should show some cyclicality even in a structurally tight labor market

Employees are just less likely to ask for and get raises when the company isn’t doing so well or when the share price is down (which is the case for the majority of listed US companies this year). Their bargaining power may come back as the economy improves

But for now, wage growth seems to cool off, and hiring is tepid. What drives this? It’s simple: Corporates are less keen to hire if they see less demand for their products. The US consumer buys their products, and after two years of inflation it just seems to be tired of spending

Now, the US consumer has been declared prematurely dead many times, so one has to be careful with any assumptions of its demise

With this caveat, I want to point out rising credit card delinquencies. These appear to mimic typical consumer late cycle behavior, where spending is maintained on credit, until that eventually is maxed out, then card delinquencies rise

For younger demographics, credit card delinquencies are now approaching a decade high

This is obviously only one narrow part of consumer debt, where the overall picture remains solid given termed out mortgage debt. But clearly for those getting delinquent, that doesn’t help

Summary: Despite historically high job openings, wage growth trends confirm the impression of cooling labor market, as do anecdotal observations. Slowing consumer demand is the likely culprit, with signs of typical late-cycle behavior in credit card delinquency data

Putting all that together: If history is any guide, then we are currently in a pre-recessionary labor market, with meaningful odds of eventually tipping over

BUT, while these are the most dangerous words to ever be uttered in economics, here are some valid reasons to consider why it could be different this time:

The biggest reason is Covid. The pandemic threw the labor market into disarray, as millions left the labor market either to take care of children stuck at home (women!), or because of sickness. Former Fed economist Claudia Sahm highlights in various worthwhile interviews why her own “Sahm rule” may not apply this time. It predicts further substantial job losses once the unemployment rate rises moderately. So far, with few layoffs, the rise in the unemployment rate is driven by supply coming back to the labor market, rather than people getting fired and losing their salary, and thus setting said negative feedback loops in motion

The second biggest reason is demographics. Labor hoarding as introduced above may today be due to an aging population rather than inflationary reasons as in the 1970s, when the working population actually grew quite fast. With baby boomers mass retiring and subsequent generations far smaller in numbers, the skilled labor shortage is real. Further, in countries like Germany or Japan labor hoarding is an established practise that persists through the other side of a downturn. We cannot rule out similar behavior in the US this time around as demographic change makes skilled labor much harder to replace

Third, the absolute level of unemployment is very low. If we were to add 2% to the unemployment rate and take it to 5.9%, it would take us to levels last seen in 2014 and still much below the financial crisis. This could mean the impact on growth is limited

Finally, labor trends are forceful, but they a slow. It is unlikely that the labor market falls apart within a few months. There is likely still a meaningful window where economic momentum can turn up again, or where policy action can be taken

However, should employment “break”, the risks may be pronounced this time around, for the following reasons:

Next year is an election year, and that usually means one thing - political paralysis. Expect a much more complicated process to get anything done

The fiscal deficit is already a staggering 8%/GDP. If unemployment goes up, tax intakes declines and expenses increase which widens it further. How much more can be spent for social support in that context?

Inflation is still high and sticky. Money supply patterns continue to suggest fodder for further inflation waves. Can and will the Fed ease when it should? Or will it wait too long, just like it waited too late with rate hikes in 2021?

Conclusion:

Several employment trends are now at levels that have historically always lead to significantly higher unemployment

A labor market disrupted by Covid as well as demographic change *could* mean it will be different this time

Should the labor market break, it will be harder to drum up support as congress faces elections, the deficit is high and the Fed’s hands may be tied

These dynamics are not hidden from the broad discourse. The recession consensus is once again on the rise, with significant increases in unemployment as part of the forecast. And, yes, there is reason to assume that view. But here’s what I think:

While no one knows what will happen yet, I think the likelihood that things evolve - at the very least - differently than expected are high. Covid has blown up most traditional economic models. This could once again apply to the labor market, which also faces unprecedented demographic change

Some food for thought: The European chemicals industry is going through a downturn on par with the financial crisis (see slide from German Chemicals Company Evonik below). Yet, it has barely laid off any staff. A possible template as other sectors slow down, too?

What does this mean for markets?

The following section is for professional investors only. It reflects my own views in a strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please see the disclaimer at the bottom for more details and always note, I may be entirely wrong and/or may change my mind at any time. This is not investment advice, please do your own due diligence

A brief recap:

In my last post I described how last week’s Treasury decision to issue more bills instead of long-term debt (vs expectations) could have seminal character. I walked through three scenarios that described various possible repercussions while we wait for the dust to settle

I further wrote that my inclination was that it was likely insufficient to change the trajectory of the economy and markets, but that we would need to watch especially bond market trading for further clues whether that view was right

Either way, in accordance with my base case, I had sold the Small Caps and Unprofitable Tech bought for the short squeeze following the QRA, and entered some bets for equity downside again

In turns out, after a strong 10-year auction on Wednesday, likely as CTAs and remaining short covers provided the bid, last night’s 30-year auction once again saw exceptionally weak demand, as measured by the various usual metrics

In my view, this has likely brought the Treasury supply issue front-of-mind again, after it had been completely buried within just a couple of days following the QRA

Consequently, I’d think that US long-term yields now likely trade with a “supply premium” relative to where they should be, as anyone wanting to buy them will have seen the auction results. How large is that premium and how long does it last? I don’t know, but I would judge it not to be ephemeral

To keep in mind: The market does what ever screws the largest possible number of participants the most, and I have been and will be part of that many times again, too. Either way, sentiment had swung dramatically in a short period of time from rates that stayed “higher forever” to the imminent advent of a recession. So what trades have I done this week, with that in mind?

As mentioned on Monday, I had bought equity downside exposure early this week, to which added further

I took the other side from what I perceived a potential local apex in the bearish growth narrative by shorting US 10-year bonds after Wednesday’s strong auction (see here) and by buying crude oil call spreads yesterday, and have added to the latter today

Crude oil sold off almost 20% in recent weeks both on the war premium deflating again, as well as macro hedge funds hammering the commodity in expectation of a recession. Demand appears to hold up well, and speculative positioning is now possibly back to June lows when the previous rally started (we find out on Monday with the CFTC’s latest data). I believe many macro hedge funds have also run regressions similar to what I’ve discussed today, saying unemployment will shoot up, which likely supports their recession view

In summary, I think the current pain trade for the most market participants is likely yields up, oil up and equities down, so I’ve positioned in the opposite way. Please note that this setup can work for a variety of outcomes, but equally none of the components may work, or the timing could be off.

I find equity downside the most likely out of the three and am larger in that vs crude and rates. But I also have to recognise seasonally strong flows and momentum, even though the early November ramp should have frontrun much of that

Looking ahead, once again everything rests on US long-term Treasury yields. What will they do?

Yesterday’s 30-year auction has likely shown that the supply avalanche is still an issue for Treasuries. Sure, it is only one datapoint, and could just be absorbed by a broader bid for duration that I may fail to recognize. This is the risk I take with my view

Either way, all else equal, the supply premium now likely priced into long-term yields should weigh on risk assets and eventually the real economy, though as mentioned for the latter, it may take more time than many in the market currently anticipate

Still, the dust is still settling over the Treasury’s QRA policy change. Thus, I continue to remain open for alternative scenarios. I will listen to both data and the market to flexibly evolve my judgement, should it be necessary

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

amazing

Regarding "Yes, job openings are still historically high and an encouraging sign for labor demand. How can we reconcile this with tepid hiring? Skills or geographic mismatches could be the reason, as could be stale advertisements"

I heard Danielle DiMartino (I think) explaining this fact because a single remote job (WFH) is being advertised in multiple (50+) states. 50 job openings for 1 job position. Not sure if true.