Animal Spirits (Part 2)

Implications from the past weeks' seismic shift in markets

After Tuesday’s CPI release I sent a brief post explaining why in its wake I bought some of the equity market’s most beaten up areas. Subsequently, a short squeeze had once again set in motion, with those areas in the lead. I do not know whether it lasts, though I deem the odds favorable and I am constructive on risk more broadly into the New Year

Today’s post provides more context on the reasoning, what I think the market is telling us about the economy and what I look for to invalidate my view

As always, it closes with my current outlook on markets

As discussed in Tuesday’s post, with the latest US CPI release the “inflation fever” broke. The monthly inflation print came in at ~2.5% annualised. Important details suggests an even stronger disinflationary impulse

About 40% of the official CPI is comprised of rents, which are measured with a ~1-year lag (see on OER method here). If we used a real-time measure for rent, the overall CPI would have come in even lower

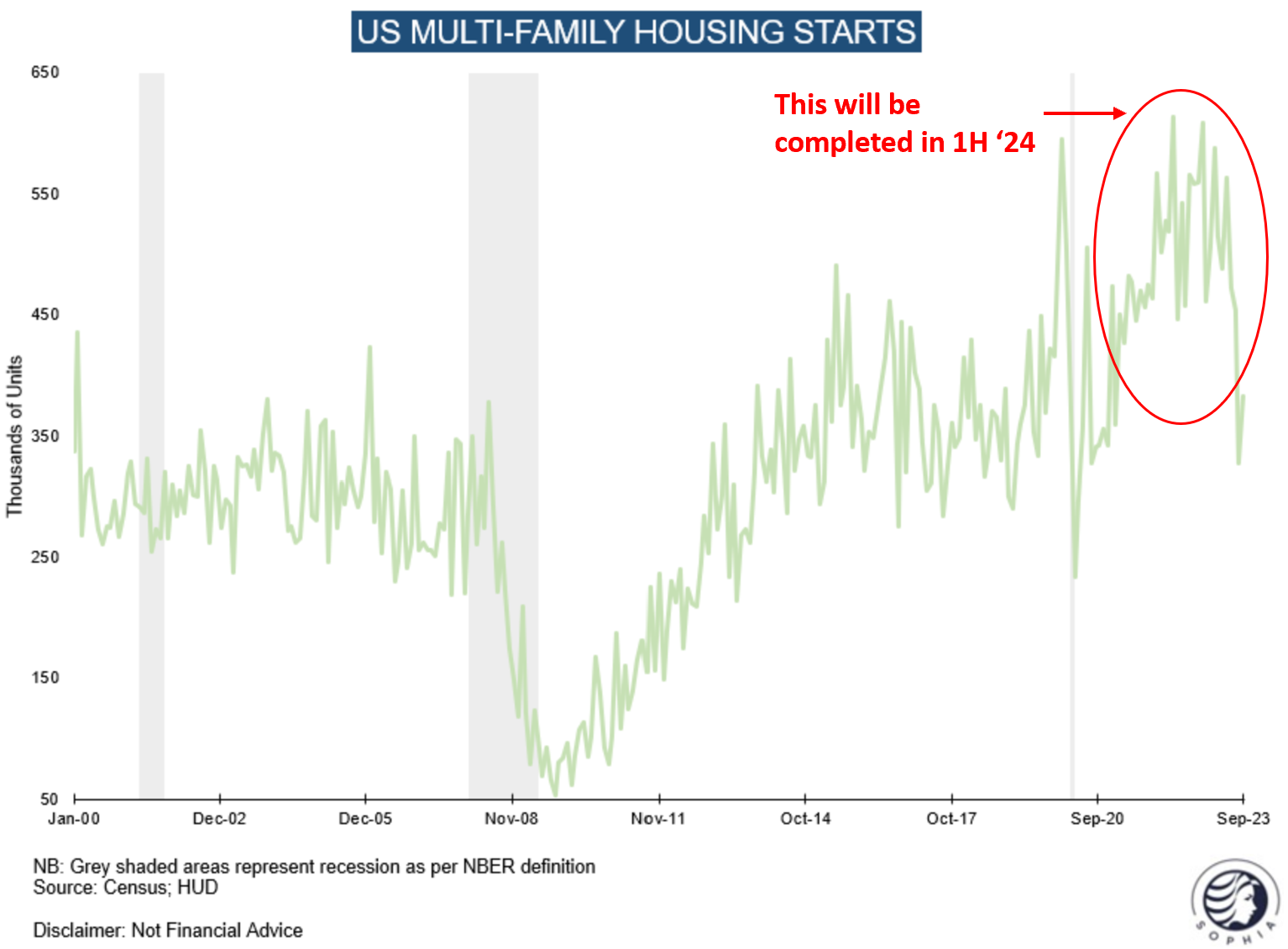

More so, there is reason to believe the downtrend in real-time rents continues. During the ultra-low interest rate period over Covid-19, a record amount of Multi-Family homes was commissioned. As it takes time to build them, they will largely hit the market in the coming two quarters and keep a heavy lid on rental growth for some time

Further, as discussed, economic momentum is clearly slowing, which likely weighs on the other CPI components for a while. See the Walmart CEO’s comments below on yesterday’s earnings call:

Taken together, it is reasonable to assume that inflation readings for the coming 1-2 quarters will be low. Here’s what’s important:

If that were the case, the Fed’s 5.25% interest rate would quickly appear to be too tight, as real rates would expand dramatically as inflation comes down. Sure, this is obviously only a temporary snapshot (inflation could accelerate again), but Jerome Powell has suggest cuts himself in that instance before. The bond market also likes the argument and is now pricing in cuts from next Spring onwards

The common pushback to this line of thought is that the Fed would only cut if the economy is in peril, which would be very bad for asset markets. I am agnostic on this, but need to point out that a severe recession is not necessarily needed for inflation to slow down. We just had a decade of low inflation without an economic collapse

However, looking further ahead (which markets don’t do), it is likely that inflation comes back. Why?

The structural reasons likely haven’t changed, from fiscal spend to skilled labor shortages to geopolitical shifts to rate-insensitive households or the recent Treasury decision to prioritise short-term bills over long-term bonds in funding the government

Just looking at the Multi-family chart above, new starts are down and will likely trend down for a while. Once this past year’s supply is absorbed, this market will eventually get tight again

Summary: The latest US CPI release has taken the sting out of the inflation narrative. For the coming quarter(s), inflation likely remains subdued. The odds are high that it returns thereafter, however market are unlikely to as forward-looking

Ok, so the inflation narrative is likely broken, for now. Let’s take that assumption and contrast it to how equity long-short hedge funds in particular are positioned. I have at many instances laid out how this investor segment on aggregate should be faded in their extremes, as they have become too large to generate meaningful alpha (as a group - many individual funds still do very well). With basically no one left to arbitrage, they have to trade against themselves (see more details on this here or here)

Equity long-short hedge funds showed extreme positioning in two aspects coming into this new narrative, as per Prime Broker data that was widely circulated online

First, their gross exposure is near record highs

Second, their net exposure is near lows

In other words, they are highly levered, with many more shorts than their historic average

And what do they own on the short side? Mostly high beta, interest-rate sensitive stocks that have been completely beaten down this year

The chart below shows some of these sectors, and their dramatic underperformance since January

Thus, the bed is laid for a feedback loop that could now set into motion. It goes as follows:

Inflation fever breaks→Rate sensitive sectors are bid→High short interest see supply/demand inbalance in them→Price moves up aggressively→Performance pain sets in and hedge funds cut positions→Price moves up more aggressively as much more buyers than sellers→squeeze continues

This is particularly pertinent as everyone owns the same stocks on the long side:

As long as these mega caps go up, the imbalance can be glanced over. If they stop rising, for which the odds are now higher given their tremendous run, shorts squeezing creates much more urgency to cover. So how does it resolve itself?

I have seen this movie before, and it usually resolves with mass capitulation, i.e. hedge funds degross by selling their longs and covering their shorts in a price-indifferent way at the same point in time. I’ve pointed out these occurrences over the past two years in the chart below

However, not all movies end the same way. Here’s are reasons for why it could be different this time, it is also what I look for to invalidate my view:

Bond yields rise again. This would weighs on these rate-sensitive areas, as both their valuation declines as well as their access to capital deteriorates. With seasonal momentum firmly in favor of bond buying between now and year-end while economic data slows, I assign low odds to a major yield breakout for the remainder of ‘23

The economy tilts into recession. High-beta stocks are very sensitive to economic downturns. A slowdown is already priced into them, but a recession would take their earnings down more than they’d benefit from multiple expansion due to lower bond yields. The US economy could go into recession in ‘24, and the market could front-run even this year. It is also a possibility that already data deteriorates sharply in the next few weeks. I assign some odds to this outcome, but it is not my base case this side of Christmas

Now, as we listen to the market for clues as to where the economy is going, what does it tell us with the past weeks’ aggressive price action?

With both bonds and equities rallying, the market is telling us that the odds of a soft landing are much higher than commonly believed, and than their historic precedent implies (most “soft landing” hopes ended in recession, aside of ‘93/’94 and probably ‘66/’67)

But we have to acknowledge the strength especially in equities. Please keep in mind, this new equilibrium has been established very quickly. It is therefore fragile and can be taken apart by, say, a weak NFP print in a heartbeat. But the market is telling us that for now, the weak data everyone fears seems still some time off

How can we make sense of this? I believe two dynamics support the soft landing dream. At this point I cannot judge whether they will hold - I frankly do not think anyone knows - but we should acknowledge them:

Demographic change. This may have made the labor market more resilient. When unemployment shot up during the inflationary 1970s, the labor force grew rapidly as baby boomers came of age. Today, these are retiring and leaving a skilled labor gap behind them. It is notable that the NFIB Small Business survey still sees labor shortage as one of the biggest issues for its constituencies, much more so than sales or interest rates (Please see my recent post “Will it Hold?” for a detailed analysis of the US labor market)

The fiscal deficit. Unprecedented in size outside war and recession, it both stimulates economic activity and provides liquidity, as long as bill issuance is prioritised

We have no historic precedent for this combination of dynamics, so the outcome may at the very least be surprising

Conclusion:

The inflation fever has broken, and while it is likely to return in the future, for the next quarter(s) a disinflationary trend likely lies ahead

Markets are adjusting to this new narrative. The odds are this adjustment occurs in a violent way, e.g. by squeezing equity hedge funds that are short out-of-favor sectors

This is not an all-clear though. We have to accept that the recession odds have risen. The risk is the market could price them, possibly even this side of Christmas

Demographic change and fiscal stimulus are possible reasons for a soft landing. However, there is no historic precedent for this combination of dynamics, and we have to stay vigilant for a more negative outcome

What does this mean for markets?

The following section is for professional investors only. It reflects my own views in a strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please see the disclaimer at the bottom for more details and always note, I may be entirely wrong and/or may change my mind at any time. This is not investment advice, please do your own due diligence

As laid out in Tuesday’s post, right after the CPI release I entered long positions in high beta, out-of-favor areas within equities, such as Small Caps or Biotech, as well as out-of-the-money calls on US Solar and Regional Banks (see here and here)

In my view, these areas have suffered the most from higher yields, so the “inflation fever” breaking should help them the most

Given their high short interest, I think some of the sectors could squeeze substantially (hence the OTM calls). More broadly, equity flows should stay supportive into mid January

Finally, looking at the chart below and using Small Caps (Russell 2000) as a proxy for this space, it appears to have tested the Covid-lows relative to Large Caps (Dow Jones) multiple times in the past weeks and they’ve held

As always, there are many ways to look at this and certainly also risks. I have already singled out a yield resurgence as well as the recession risk in the main body of today’s post

In particular on the recession risk, incoming data will guide us to its probability. The next milestone is likely the November labor market data released on December 1st, as well as the weekly Initial Jobless Claims. Should either release be very bad, the narrative will move to recession very quickly

Further, looking at intermarket relationships and presenting a differing view to above, the ratio of Small Caps vs Technology continues to be in a downtrend. For those weighing the severe slowdown case more heavily, this trend would simply continue; it would still be too early for Small Caps, with many of them early-cyclical in nature

I continue to think that the market is currently too negative on an imminent recession for the US economy. But, yes, the risk is there. As always, we need to stay vigilant, observe the data closely and listen to what the market tells us going forward

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

great comprehensive take, thank you!

Excellent post Florian.. cleared up most of klmy doubts I had, but majorly what would NEGATE my positioning, i.e. rise in yields would immediately negate it. (Im short nq long solar - $maxn, $tpic and $stem).

Having said that, i think there is 0% chance of a soft landing - why - because Jim Cramer said we're having one.. that guy has a crytal ball on the exactly opposite thing that's gonna happen.