Red Alert

The Treasury rout continues, it likely needs a catalyst to end

In early August I published a post titled “A Warning” that urged for caution in light of likely rising long-term US Treasury yields. At the time, the warning was of an “amber” nature. Staying within the colour metaphor, this has now moved to “dark red”. While the rise in 10- and 30-year yields was orderly first, it has recently assumed a disorderly nature, as discussed last week in “Too Fast, Too Furious”

For the current month, the market finds itself in a liquidity vacuum as large deferred California corporate tax payments are due. At the same time, economic data remains strong, giving little reason to buy bonds. Looking past these short-term dynamics, huge deficits are forecast for years to come while foreigners, banks and the Fed are all absent from Treasury markets, just as supply is ramping up. This begs the question where the bid for bonds will come from, something I repeatedly pointed out in the past weeks as many traders enthusiastically dip-buy the 30-year, or its ETF-equivalent TLT

While Treasuries remain very vulnerable and possibly require a catalyst to end their rout, fast money is equally enthusiastically buying the dip in equities, creating a high-risk constellation where another leg higher in yields could trigger a serious wave of selling in stocks as everyone is caught off-guard. In a classic case of Reflexivity, this could then provide the catalyst for Treasuries to stabilise - the 1987 comparison looms large

Today’s post walks through the dynamics and also discusses what to look for to invalidate my thesis. As always, it closes with a current outlook on markets. I remain all-cash since early September, will buy puts on any equity rally and see several weeks of heightened volatility ahead. This period could create some interesting setups in safe-haven assets, and I continue to see a buyable low in equities possibly at its ends

Let’s start with the picture in equities, the asset class I now perceive as most at risk. Why so, after all, the -6% S&P 500 drawdown in September created oversold conditions that historically, 90% of the time favored a bounce?

Indeed, the market is batting for said bounce. CFTC positioning data shows large speculators have bought the dip aggressively. I’ve shared this chart several times before, it keeps going up. Large speculators are now the most long S&P 500 futures in more than a year

Further, Equity long-short hedge funds went into September quite long and got run over, clocking up the worst month of the year so far according to GS prime broking data. Yes, in response, they reduced their market (“net”) exposure by adding popular single stock shorts (e.g ARKK) and some index shorts, which in theory provides the fuel for a potential bounce. However, over the past trading days, they covered shorts again

Some near-time sentiment surveys also show an unusually large swing from bearish to bullish late last week (e.g. here by Nautilus Research)

So conditions historically favored an equity rally at this juncture, but many are already positioned for it. Importantly, there is now one ticker that overrules all old playbooks, that of the world’s most important asset, the 30-year US Treasury bond. For equities to do well beyond technical bounces, it needs to stabilise and likely revert. So let’s look at what data is saying about the long-end of the US bond market:

For bonds to stabilise, we would like to see fast money get stopped out of their longs and capitulate. This would indicate that selling has reached an apex, and little buy demand would be needed for bonds to rally

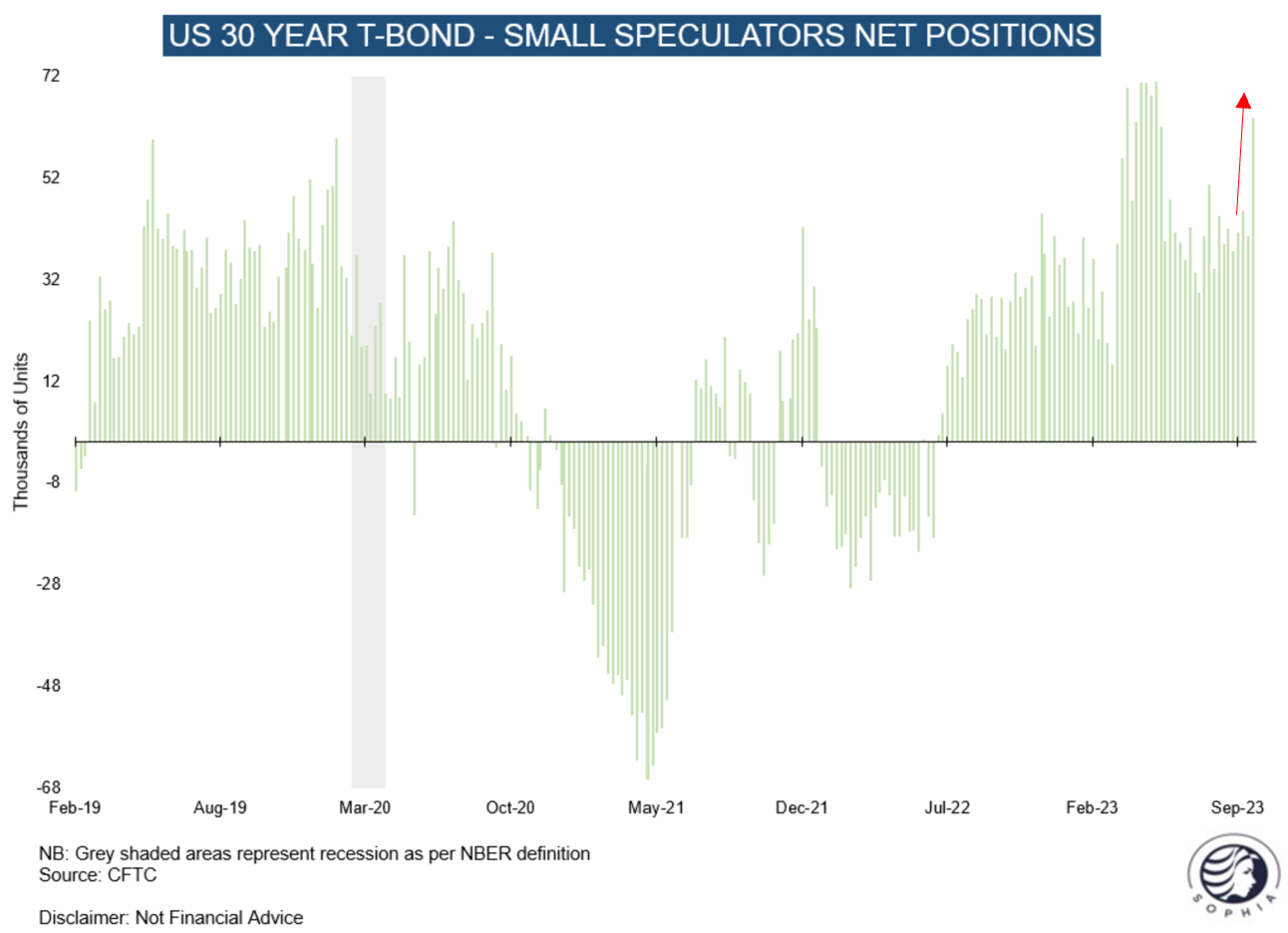

CFTC positioning data for large speculators isn’t useful as it includes data-distorting arbitrage/basis trades. However, the subset for small speculators paints a clear picture. These are of the same fast money character, just smaller in size and they do not engage in arbitrage trades

Looking at the data, there is no sign of capitulation. Instead, just like in equities, we see fast money has bought the dip and is now the most long US 30-year bond futures since the Spring, when Silicon Valley Bank’s demise created a rush into Treasuries. This also ties in with my anecdotal observations, where many traders I speak to have bought TLT recently

This is a very bad sign. For the rout in Treasuries to end, one would want to see capitulation instead of dip-buying. The latter provides more fuel for the selling to continue. Whoever bought will need to flip their position again should Treasuries fall further

But why would they fall further? Several reasons speak for it, let’s walk through them:

Liquidity vacuum. As mentioned in the introduction, October represents an unusually large liquidity drain from asset markets as deferred California corporate taxes are due. Companies like Google will have to sell current cash-like holdings (most likely T-Bills) to make these payments, with a knock-on effect on all other assets

Strong economic data. While there may be some worrying signs on the far horizon (there always are), nothing in near-term data suggests a substantially slowing economy. In fact, initial jobless claims, the most near term and objective data on the labor market, just printed a six-months low, and the ISM Manufacturing index printed a six-month high this week. (NB: When the economic outlook is strong, long-term rates go up/bond prices go down, and vice versa)

Important buyer groups retreated. Bond buying is historically done by foreigners, banks, the Fed (QE), insurers as well as households and corporates. Three of these are out of the market right now: Foreigners stopped buying over a year ago, banks have long reached their maximum holding and the Fed is doing QT instead of QE

Huge supply. While the buyer universe has shrunk substantially, supply is being ramped up at a dizzying pace as discussed here or here. The coming week has another string of large long-end auctions lined up, and there is no slowing down well into ‘24

Taken together, this creates a fragile setup where the market neither has the confidence nor fire power to end the Treasury selloff. So what will it take for yields to turn? I see four possibilities:

Eventually everyone who wants or needs to sell is done, and then it only requires a handful of buyers to drive bond prices up, and yields down again. This is the key argument that invalidates today’s thesis - the Treasury tantrum just peters out by itself, like many other market exaggerations, and maybe it is already over. I remain very open-minded about it, but the small speculator data (see above) makes me think that we are not there yet

Economic data turns bad and brings with it a revision in the nominal growth outlook, thereby providing a strong reason to buy bonds. As discussed above, all current data is strong, e.g. the Nominal GDP estimate for August just came in at 10.6% annualised (!). However, this may change, the US labor market in particular is of highest importance here, with the next NFP dataset due on Friday. In any of the leads I follow, I cannot see any sign of the labor market cracking, but it equally remains a possibility

The Fed intervenes to end the rout, just like the Bank of England did during the Trussonomics inspired Gilt-meltdown in Oct ‘22. It could tweak or end QT, provide “liquidity management” to the long end or other measures. This is a high-risk endeavor, as any “easing” of monetary conditions would seriously hurt their inflation-fighting credibility and likely create a panic bid into real assets. The bar is very high on this one and likely requires a pretext

The stock market sells off and that brings a revision in the nominal growth outlook. E.g. one possible transmission channel between markets and the real economy would be banks curbing lending as collateral values decline (see “From Secular Stagnation to Secular Reflation” on the importance of bank flows for economic growth)

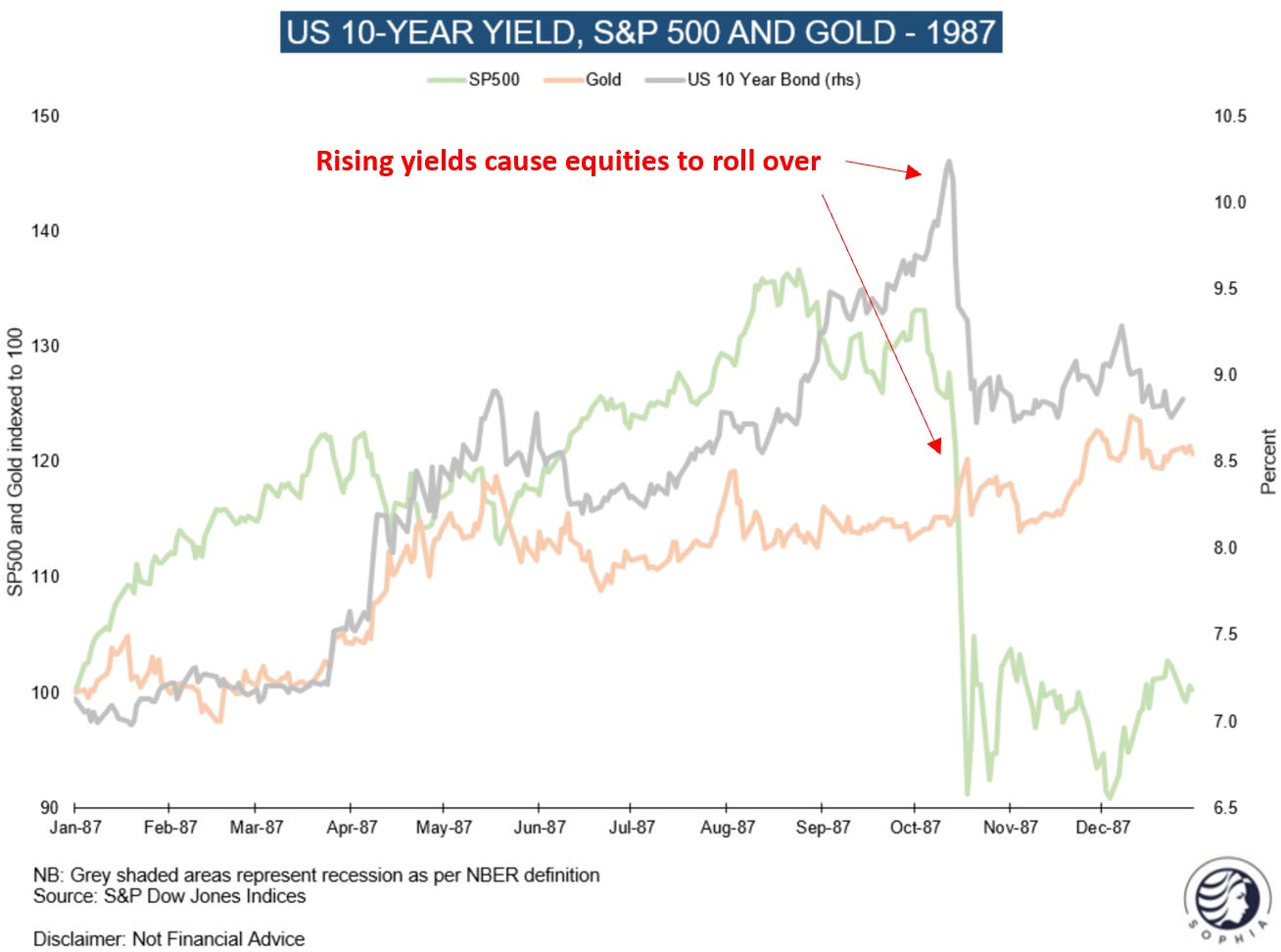

Let’s expand on the last point - it is the 1987 playbook, another pre-election year with eery similarity when looking at the chart below. Yields rose over the course of the year, so much that they eventually caused stocks to crash. That was also the remedy. The market melt down provided the reason for bonds to be bid, and the rout was over

However, there are many differences to 1987. Most obviously, deficit spend wasn’t as out of control at the time, so I am not sure whether a stock market sell off would lead to bonds be as well bid today. Equally, with abundant fiscal spending, the market may never sell off as much now. Either way, a flight to safety this time around may involve the Swiss Franc, the Yen, Gold or Bitcoin instead of Treasuries. I have added Gold to the chart above, it did well in the shake out’s aftermath

Importantly, a stock market sell off could provide the pretext for the Fed to intervene and ease monetary conditions, just like the BoE did in the Fall of ‘22. This could lead to a V-shaped recovery at least for some equity sectors, as a opposed to the flatlining in 1987

Keep in mind, the circumstances of the BoE intervention were different, with especially the currency playing an entirely different role. I think the key analogue however is the market’s seeming lack of confidence in the respective asset, and an event possibly needed to restore it

To be very clear: History rhymes, but it does not repeat. Very rarely do historical analogues play out the same way. With that in mind, the 1987 relation between bonds and stocks, as well as its resemblance to today are still very notable

Conclusion:

Equity markets display oversold conditions that in 90% of cases lead to a bounce. Many in the market are batting for it

However, these conditions are quickly invalidated if the rout in long-term US Treasuries continues. The dip buying then provides fuel for another wave of selling

I see decent odds that the high in 10- and 30-year yields is still not in, with massive supply into a difficult liquidity context, while important buyer groups are out of the market. A catalyst may be needed to stabilise Treasuries

This creates a high-risk setup for equities. Stocks selling off may be said catalyst that ends the rout either in a reflexive way, or by giving the Fed the pretext to intervene and stabilise the long-end

What does this mean for markets?

The following section is for professional investors only. It reflects my own views in a strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please see the disclaimer at the bottom for more details and always note, I may be entirely wrong and/or may change my mind at any time. This is not investment advice, please do your own due diligence

The coming weeks are likely very eventful and possibly historic. This is my plan for how to play them:

As stated in several recent posts, I have gone into all-cash early September. This is also owed to the fact that there is never a perfect hedge. In eventful times, market-neutral equity books can easily go haywire as hedge funds are forced to degross and chances are everyone has the same positions, leading to shorts falling less than longs

I intend to buy puts with a mid/late-October maturity (e.g. 20th Oct Opex) on any rally in equities, or possibly Wednesday this week as I expect the positive quarter-start flows to abate by then. Please keep in mind, most option trades are loss making, I would only use a small % of NAV, this is just my personal plan and it may change any minute

As discussed in recent posts, I intend to buy US value and/or other real assets should a pronounced sell off materialise that provides margin of safety, in particular should Fed/government action be used to end the US Treasury rout

I intend to buy safe haven assets such as the Swiss Franc, Gold or Yen in the coming weeks should their current negative trajectory culminate in a forceful unwind that provides margin of safety for entering them. Positioning in all three has turned from crowded to less so, but not yet capitulation. We may be close though

Please keep in mind that few plans ever materialise as originally conceived. My crucial assumption is that the US Treasury long end does not stabilise without intervention or an event (or both). This assumption could well be very wrong. Either way, some other options include:

Buy volatility with a mid/late October time horizon. Again Opex comes to mind

Sell TLT puts at say 82 and buy S&P puts with the proceeds. This would get you into TLT at a ~5%+ yields, a level I find likely to be in the “reflexive” zone where it causes so much damage that it comes down by itself, at least in the near term

Do nothing and enjoy a relaxed 5.5% yield on T-Bills

As you can see, I have opened my mind to save haven assets including gold in today’s analysis. I’ve been bearish on them for the past few months as real yields rose, and these have indeed not performed well. But I now see a constellation where their attraction could return. Same applies to Bitcoin, which would be a major beneficiary of any Fed intervention in the long end, should it occur

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

"Best things in life are free" - rarely true, but your blog is an exception. As for capital markets, I see no alternative to Fed intervention and YCC.

Tactically best course of action is to stay in money markets and t-bills. Tough time to buy or sell but if rout emerges then maybe time to buy.