Too Fast, Too Furious?

A brief market update in light of the long-term US Treasury bond crash

In several recent posts I had both expressed the likelihood of long-term US Treasury yields marching higher, and warned that September and October would likely a treacherous period for markets, which is why I had gone into cash recently despite my constructive view on the US economy

Both materialised. In particular, the price of US long-term bonds collapsed, and their yield spiked to levels not seen since 2007. This aggressive development has implications one has to respect and take note of, which today’s post does. Once again, Reflexivity will be at at work and shape the economic path from here

As always, the post closes with my current outlook on markets. Oversold conditions may favor an equity bounce in the near term, but I do not think this episode is over. I expect another bout of volatility later in October and continue to prepare to deploy cash then, in search of margin of safety only provided by market panic

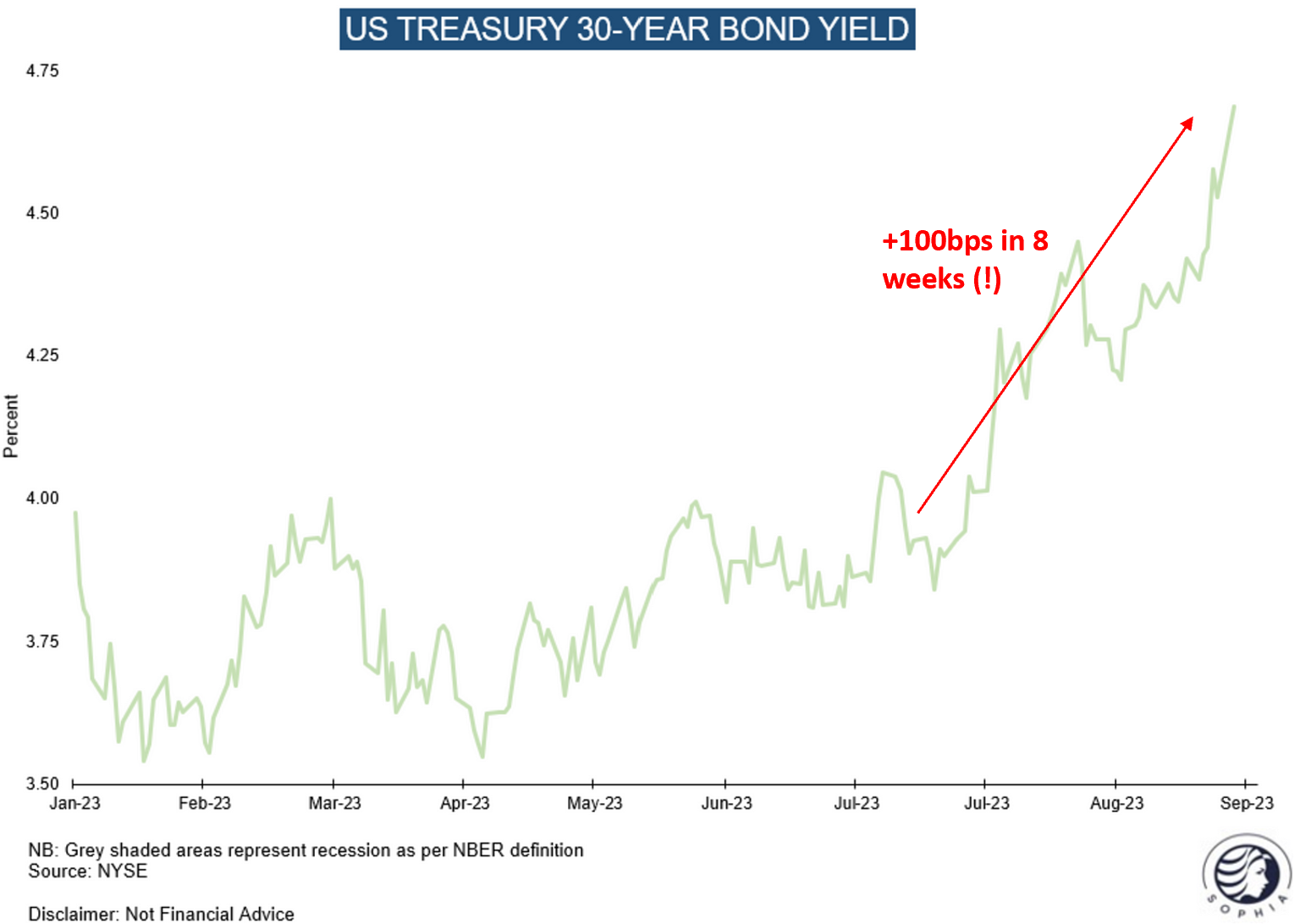

Over the past two month, the long end of the US Treasury bond curve has fallen precipitously, driving its yields up to a new generational high

As I laid out in “The Trillion Dollar Question”, this was initially driven by a re-rating of US economic growth, certainly a positive. However, the most recent move has been disorderly and very likely owed to forced liquidations by the many investors who are still long US Treasuries in muscle memory of the past decade’s “Secular Stagnation” and its low yield regime

These investors - and as the JP Morgan US Treasury investor survey shows, there are many of them - face increasingly steep losses on their bond holdings and have to throw in the towel as stops are blown

Now, an orderly rise in long-term yields (“bear steepening”) is generally a positive sign, reflective of robust and accelerating economic growth. But we have to pay some attention to this recent development. Fast and furious is great in movies, but difficult for any economy. Why?

Like the frog in boiling water who stays in the pot if it is heated gradually, but jumps out if the temperature is suddenly increased, economic actors need time to adapt

That is why a sudden aggressive change in one of the world’s most important economic variables, the US Treasury 10-yr and 30yr rates, warrants close observation for any subsequent repercussions

Where could these comes from? I see two areas:

Bank Lending. Recall how fiscal spending and private sector lending are the twin engines powering the economy (see “From Secular Stagnation to Secular Reflation”). Excessive fiscal flows are set to continue, and bank lending has picked up again recently. We need to observe the latter very closely for any negative impact from the Treasury crash. Lending that creates new money and with it new financial flows is done by banks, will it slow down as hold-to-maturity losses again become a concern?

Housing. Once again, with Reflexivity at work, many people bought houses earlier this year with expensive mortgages in the belief they could refinance at lower rates later. Said belief was encouraged by the abundant recession talk at the time, as well as a deeply inverted yield curve. It is save to say that the recent yield moves have put these ideas to rest. We now see a decline in housing starts that may intensify in the coming months

Summary: To see if there is any fallout from the US Treasury market tantrum, Bank lending and housing are two areas worth paying close attention to in the coming weeks and months

Further, as I’ve laid out before, for any economic analysis it pays to closely listen to the market - the aggregate knowledge of millions of highly informed and incentivised participants

Equities continue to outperform bonds, with the S&P 500 down 5.5% month-to-date vs 8.6% for 30-year treasury bunds (cf. the SPX/TLT ratio, see here), suggesting a decent economic context

However, looking at the below chart of the equalweight S&P 500, which removes the outsized effect of the magnificent seven, we can see the recent uptrend has been broken. This tells me the current episode is not just a trivial hiccup

Tying it all together, I bring back last week’s summary table which shows the possible regimes ahead within an era of fiscal dominance

The reflexive nature of the economy and financial markets makes forecasting all but a probabilistic exercise, where we have to continuously reassess our probabilities for each outcome with new information, such as the crash in long-term Treasury bonds

So where do we stand? Current economic data still points to the higher nominal and real growth world. Yesterday’s core durable goods orders continue to show improvement, and late September retail data appears decent

But given the tumultuous development in US Treasuries, the world’s most important asset market, we have to be vigilant and track the incoming data closely

More broadly and looking ahead into the next decade, I find the climate/weather analogy useful:

The broad economic trends are the climate - they appear obvious and easier to spot. For the next decade, this is likely the shift in power from capital to labor, and with it likely structurally higher inflation

The quarter-to-quarter economic trends are the weather - variable, interdependent and more uncertain. Will growth stay elevated or accelerate next Spring? Will we fall into recession in ‘24? With many reflexive feedback loops between financial markets (e.g. Treasury yields) and the economy (e.g. banks) we have to constantly re-assess based on incoming data

Fiscal dominance and Secular Reflation (i.e. high nominal growth) are the climate for the coming decade. Within it, periods of high real growth vs. stagflation are the weather

Conclusion:

The crash in the world’s most important financial asset market, long-term US Treasuries, needs to be paid close attention to

It may carry consequences that impact the current economic growth trajectory

However, as of today, data still shows robust nominal and real growth

Looking past the imminent future, the climate for the coming decade is likely one of fiscal dominance and Secular Reflation.

To assess the weather, we have to continuously assess the data over the coming weeks and months

What does this mean for markets?

The following section is for professional investors only. It reflects my own views in a strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please see the disclaimer at the bottom for more details and always note, I may be entirely wrong or may change my mind at any time. This is not investment advice, please do your own due diligence

“Everybody has a plan until they get punched in the face” - Mike Tyson

With that in mind, my plan remains the same - I’ve gone into all cash in early September and plan to re-engage in US value whenever market stress is high enough to provide a decent margin of safety. It has played out so far, as the past weeks have been the worst of the year

While oversold conditions now favor a short-term bounce, I think the weight of the Treasury implosion carries heavy and is unlikely to be so easily digested

Further, a significant and unusual tax drain still awaits in mid-October as deferred California tax payments are due

I’ve closed puts earlier this week that I’ve bought here. Should a bounce materialise over the coming week I will probably buy puts again for another (final?) leg lower

In order to deploy the cash, I am looking for rock-bottom sentiment readings and signs of panic and/or liquidation. We have not seen that yet in my view. Maybe we never get there, in which case I will miss it and have to wait for another chance. In the meantime, cash pays 5.5% interest - not bad either

I am insistent on buying in the hole, as I am looking for margin of safety. As discussed, my economic view is what I think is likely, but it may be wrong. Buying when others are fearful to some degree obliviates the view - the market may just rebound irrespectively

A final word on bonds - where is the low?

My sense is that we are very close, but I do not think it is over just yet. The US 30-year was extremely crowded (see above), and its ETF-derivate TLT is still seeing inflows. Recent oil price action isn’t helping either. I am tempted to engage for a trade, but it would not be more than that - Treasuries are likely in a long-term bear market (fiscal dominance!)

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

great take, thank you!

Nice write up florian. One comment re: Now, an orderly rise in long-term yields (“bear steepening”) is generally a positive sign, reflective of robust and accelerating economic growth.

Think warren pies has a retweet of bear steepener and conditions ie. Early/late cycle and shape of curve. https://twitter.com/3f_research/status/1707127489896620181?s=46&t=R4O_767541fCUQqphF0PnA

Any thoughts there? This seems late cycle here with curve inverted