Hawks and Supply

Reviewing yesterday's two important events, the Fed and the QRA

In my last post “Is the Honeymoon Over?” I suggested that Jerome Powell would likely push back against the rate cuts priced in for ‘24, which was contrary to consensus expectations of a dovish FOMC meeting. To the market’s surprise, the Fed chair spoke out forcefully against a first cut in March, jolting markets into a broader sell off

I further suggested that the Treasury’s Quarterly Refunding Announcement (“QRA”) may be less politicized than expected by many. Indeed, the supply of coupons was stepped up, and Janet Yellen did not try to send the market into overdrive

Today’s post briefly reviews the implications of each decision. As regular readers may know, my focus is on capturing important turning points across asset markets, which recently included to-the-day lows/highs in oil (see here), the VIX (here), the Yen (here), equities following the October QRA (here) or China (here). I describe why I continue to think that the odds are that equity markets may have put in a top, or is very close to doing so

Finally, as you know I have shared many of my shorter-term trades over time, tying my content and educational journey to putting my money where my mouth is. I understand that these are at times not easy to follow for some readers, so from today I’ve also included my long-term book, which focuses on participating in global asset price appreciation over time, while avoiding significant drawdowns. Both will from now feature in the “What does this mean for markets?” section to close each post

Let’s start with the Fed:

In yesterday’s communication, the FOMC and its Chair Jerome Powell pushed back against the markets’ expectation of 150bps cuts in ‘24. Why is that not a surprise?

For the nominal interest rate level, two variables matter - real growth and inflation. In combination, these represent Nominal GDP. The exit rate for 4Q ‘23 was 3.3% real GDP growth, with 3% CPI we get to 6.3% Nominal GDP. That is a very high growth environment

In early December, the various FOMC members had guided to 75bps cuts based on 1.6% real growth for for ‘24. With the recent strong GDP data, these projections would have to move upward, in theory making rather fewer than more cuts more likely, while the markets assumed 150bps. If (big if) nominal growth continued at 6%, interest rates at the resulting 3.75% would likely overheat the economy (why? because a borrowing rampage would ensue). With strong recent growth in mind, the FOMC outcome was no surprise

Further, in his press conference Powell mentioned the same potential inflation pressures I referenced in last week’s post, in particular that the disinflationary tailwind from the goods economy would likely be over, and that in recent conversation the Fed heard again more about the business cycle picking up (beige book)

Are these views correct and was it the right monetary policy decisions? Who knows. Maybe he’s overtightening, maybe he is smart and reduces inflation risk going forward, maybe it makes no difference. What is important from our point of view - what did the market expect (dovish), and what is the Fed’s new reaction function?

Powell made it very clear. Cuts will happen as early and emphatically as the market expects only if economic data weakens substantially. A conundrum especially for very extended equity markets - data would need to be weak enough to get the Fed to turn aggressive, but not so weak that any worry about earnings would be warranted

To be clear, as usual Reflexivity is at work. Equities are at all-time highs and recent economic data strong, so the Fed rather takes a hawkish lean. It certainly would have been a different meeting if stocks had just sold off 5%-10%

The same thought applies to Powell’s guidance on QT during the press conference. He guided to a start of the QT taper late in the year. Why? With the Treasury providing more coupons again (see next section), the RRP won’t be drained as quickly, and with buoyant markets there is little worry about collateral damage

Summary: The Fed reaction function has shifted from “inflation is low, so we cut” to “we need to see substantial economic weakness to cut aggressively”. This makes the path data-dependent, with coming labor market data in particular focus

Moving on to the Quarterly Refunding Announcement, the Treasury decided to pursue the logical avenue. It increased the supply of long-dated coupons at the expense of short dated bills, as coupons are currently cheap with a low term premium, so that’s currently the best deal for the US tax payer

Looking at the table below, which shows the auction sizes across coupon maturities for the past and coming quarters, we see a step up across the board, most heavily centered on 2-7 year bonds

This is smart, as a market that expects rate cuts will provide demand for this medium-term duration, where you can lock in high rates for a good amount of years, but not so long that you are stuck with it forever (10-30 year bonds)

Now, I’ve read a lot of commentary in the QRA’s wake saying this doesn’t matter anymore and it won’t affect markets. Is that right? Let’s apply some common sense at this stage:

The Treasury is raising a net $519bn coupons over the coming quarter, vs $349bn last quarter. Who is buying these bonds? Mostly large asset owners, who will have to sell other assets for it or use cash (that they could have bought other assets with)

Contrary to T-Bills, coupons are not cash-like. The longer their duration, the more their principle value oscillates, e.g. the price of the 30-year bond moves ~1% per day (vs virtually 0 for T-Bills)

Finally, while the government raises money mostly from large asset owners, it then distributes the cash mostly to lower income demographics. Basically, the cash moves from the financial to the real economy, where much ends up in household deposits. In the short run, this makes anyone in need of support happy, in the long run a very high share of government/GDP is usually corrosive for economic growth

So what’s the answer? Of course it matters, the only question is how much? The current total of US coupons outstanding is ~$17tr (~20% of $23tr total debt), in Q2 there will be $500bn more coupons, this year probably $1.3tr+, ~8% more supply in a year. Not enough to cause a crash, but enough to move markets

An example: In late October, when the last QRA jolted a huge rally in bonds, CTAs were max short Treasuries to the tune of -$200bn. Treasuries rallied hard until they were done covering at the turn of the year. Afterwards, treasuries fell again. Right now, CTAs are max long, and coupon sales are increased. Sure, there can be a recession-fear driven bid for bonds, but the money has to come from somewhere. If bonds are bid anyway, the next obvious source is equities

Summary: The step up in long-term coupon supply within the QRA is meaningful, yet centered mostly on 2-7 year duration. On the margin, it should provide a headwind to asset markets

Taken together, in the near term, the Fed and the QRA are a headwind for equities and bonds. There are some more signs however that equities may have formed, or are in the process of forming a top. Let’s listen to the market for this:

In an equity bull market, usually the combination of higher beta and quality leads. For the US, this is the Nasdaq. Since last week, it has underperformed the S&P 500, in other words, it has diverged and is not leading in the past. You saw the same price action between the two during July ‘23 which was followed by a multi-month sell-off (and many other occasions in the past)

[chart]

Similarly, the “Dow Theory” stipulates a lead/lag relationship between the economic growth sensitive Dow Transport and its lower-beta cousin Dow Jones. Again, a divergence appears, Transports have weakened recently, possibly leading the Dow

Add to that sell-the-news reactions on in-line Large Cap Tech earnings (who is the incremental buyer?), a continued string of poor corporate earnings (cf. Adidas last night), and the launch of several vol-selling ETFs (often a top sign in a trend) and the signs start to line up

Does that mean we crash? No. Does that mean we could take another leg up to fool everyone and then fall? Of course. Is it certain that the market will fall? Definitely no. The odds are simply higher now, and at similar instances in the past equities often fell

Finally, a few brief words on the labor market, which has now firmly moved into focus as the most important metric for markets to be watched. As I discussed in “Housing vs. Disinflation”, two dynamics are currently at odds in the US economy - a weakening labor market, which may be lagging, and a reviving goods economy (housing/freight) which may be leading

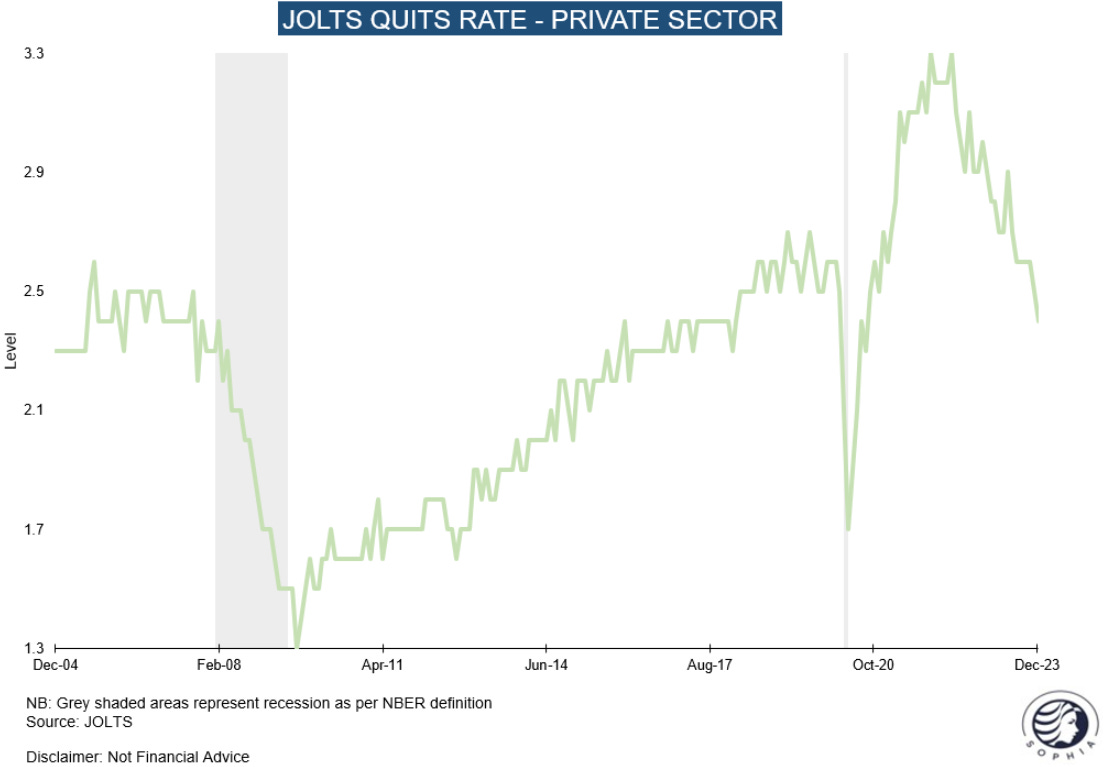

We have to see who will keep the upper hand, and while some recent labor market details have continued to be poor, such as the Quits Rate for private sector jobs…

… consumers have recently felt more encouraged by labor market conditions as an important detail from the Consumer Conference Board survey shows, which often lead other labor market data in the past

Summary: After a long string of weak labor market data, we have the first sign of greenshoots for employment. Whether it was a fluke or will last, will need to be seen as more data comes in over the next weeks

What does this mean for markets?

The following section is for professional investors only. It reflects my own views in a strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please see the disclaimer at the bottom for more details and always note, I may be entirely wrong and/or may change my mind at any time. This is not investment advice, please do your own due diligence

As mentioned in the introduction, I have now split this section into two parts, one which reflects my short-term market views, the other a long-term, asset allocation driven perspective. The goal for the latter is the steady capture of global asset price appreciation over time, while avoiding significant drawdowns, it is run as a long-only book. Neither are investment advice - I could change my mind at any time or be entirely wrong, always do your own DD

Short-term book (Active Trading, Long & Short):

Yesterday morning, I added S&P puts in anticipation of the day as it unfolded (see here) and then hit the sell button on Small Caps as it was clear that Powell’s initially dovish comments couldn’t lift the market. It turned out to be one of my best days over the past year as I was both prepared and got lucky. I further covered the 2-year short after the press conference, it hadn’t moved much from entry, but I now see some risk of the market wanting to possibly run a growth-worry narrative next. In summary:

S&P 500 puts mid/late February

Short Small Caps/Russell

Long EU Luxury/Short Dax

Long Copper and Oil Majors

Long China

Long-term book (Asset Allocation for Medium & Long Term):

As you can see, my starting allocation is quite high with almost 2/3 in T-Bills. I am looking to reduce this as opportunities arise in the coming months particularly in equities, which right now I think are at risk of correcting. In particular, I am still patiently waiting for an entry to Robotics, as well as a particular part of the AI value chain (see here, thank you Gavin Baker). Hopefully some volatility in the weeks to come will provide this opportunity, otherwise 5.3% interest is also not bad. I have set the bond allocation to 20% at the belly of the curve as a recession hedge, and started with some equities and a 5% share in commodities, where I like copper the most (secular demand from electrification, EVs etc.). Over time, I will likely also add an allocation to crypto, though the parth of least resistance for Bitcoin for now appears to downside in my view. In summary:

60% T-Bills

20% Bonds (US 5-Year)

15% Equities (5% DAX, 5% XLE, 2.5% S&P 500, 2.5% China Equities)

5% Commodities (Copper)

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

love that you share both your logic and your investment/tactical decisions.... not frequent to find a professional willing to share so much... thank you

Excellent post.