The Trap

Why downside risk continues to be elevated

Today’s post provides a refresh on my recent views using the latest positioning data. I explain why I continue to see high downside risk for equities, and a cloudier economic context

Regular readers will know I strongly adhere to the concept of Reflexivity. Through its lens, the economic world is perceived as a plethora of interdependent variables, the probability of their evolution inversely correlated to whatever financial market consensus thinks

In this uncertain world, positioning is my objective north star. Not only because most other variables are subjective and interdependent. More so, it’s simple - the majority view cannot become reality on a continuous basis, otherwise markets would be perpetuum mobile or a free money machine. We all know they are in fact the opposite

Further, as financial markets and the real economy are closely connected via countless feedback channels, consensus views can give important clues as to what outcomes are less likely in the real economy. Today, I believe the market is now too optimistic on economic growth, and still too optimistic on interest rates, as this post aims to illustrate

As always, the post closes with my current views on markets. Having gone into cash early September and batting for equity downside via puts since, in my last post I stated that the odds would now be high for “risk off”. This appears to materialise. I will share my plan for the coming weeks, and also provide a comment on next week’s pivotal Treasury quarterly refinancing statement (“QRA”)

To start, let me summarise my recent conclusions in three charts:

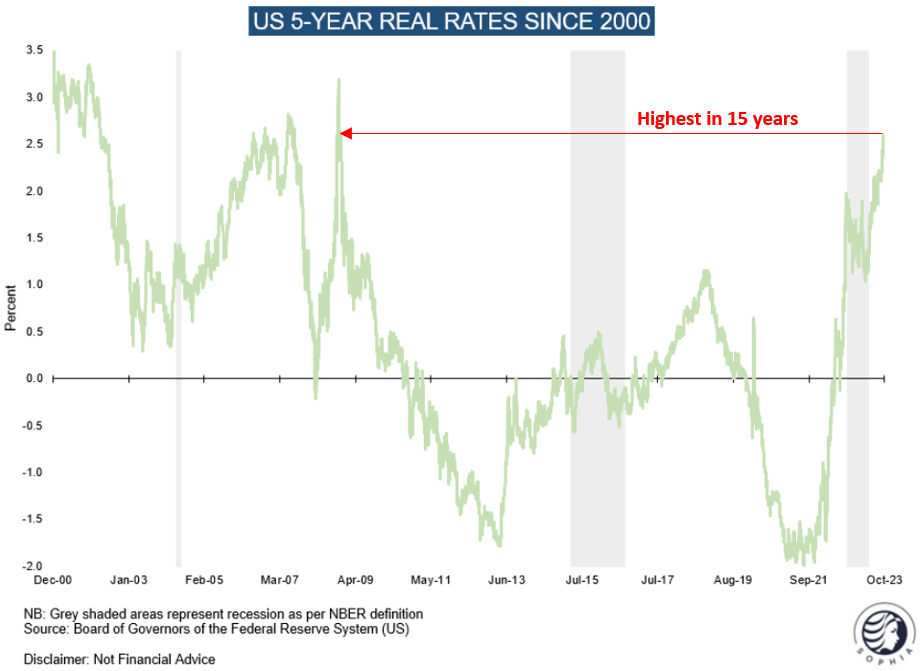

Real rates a currently exceptionally high. The reason for this could be either strong economic growth, or excessive government debt issuance

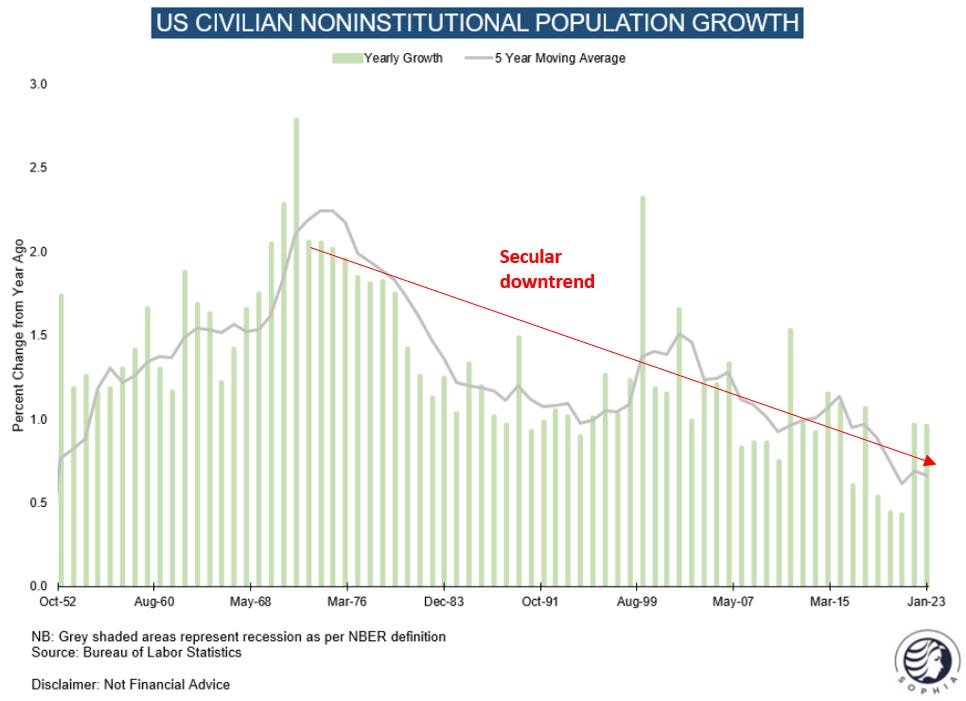

Historical comparison suggests that excessive government bond issuance is the significant driver. The current level of real rates is very high for current population growth, and productivity is likely low as we are within an inflationary period (see “On Real Rates”)

The market corroborates this view. Many important trends broke the moment US long-term bond yields went into their disorderly stage. This way, the market is telling us the high yields are now an issue for economic economic activity (see “On Listening to the Market”)

Into this context, latest positioning data paints a concerning picture. Let’s walk through it in a few short steps:

Equities

During the first half of ‘23 many investors were convinced of a new low ahead for the S&P 500. They continued to short the market and thus provided the fuel for a tremendous rally. Today, we see the inverse. Consensus calls for a year-end rally, if we take Wall Street strategists as a proxy

Further, I have shared the following chart many times. Every time I update it, large fast money accounts get more long S&P futures. This reflects the same dynamic. In 1H ‘22, they shorted a rising market in hope of a new low. Now, they are buying a falling market in hope of said year-end rally

The near-time NAAIM index reflects exposure amongst active investors and shows a similar picture, as do various sentiment surveys

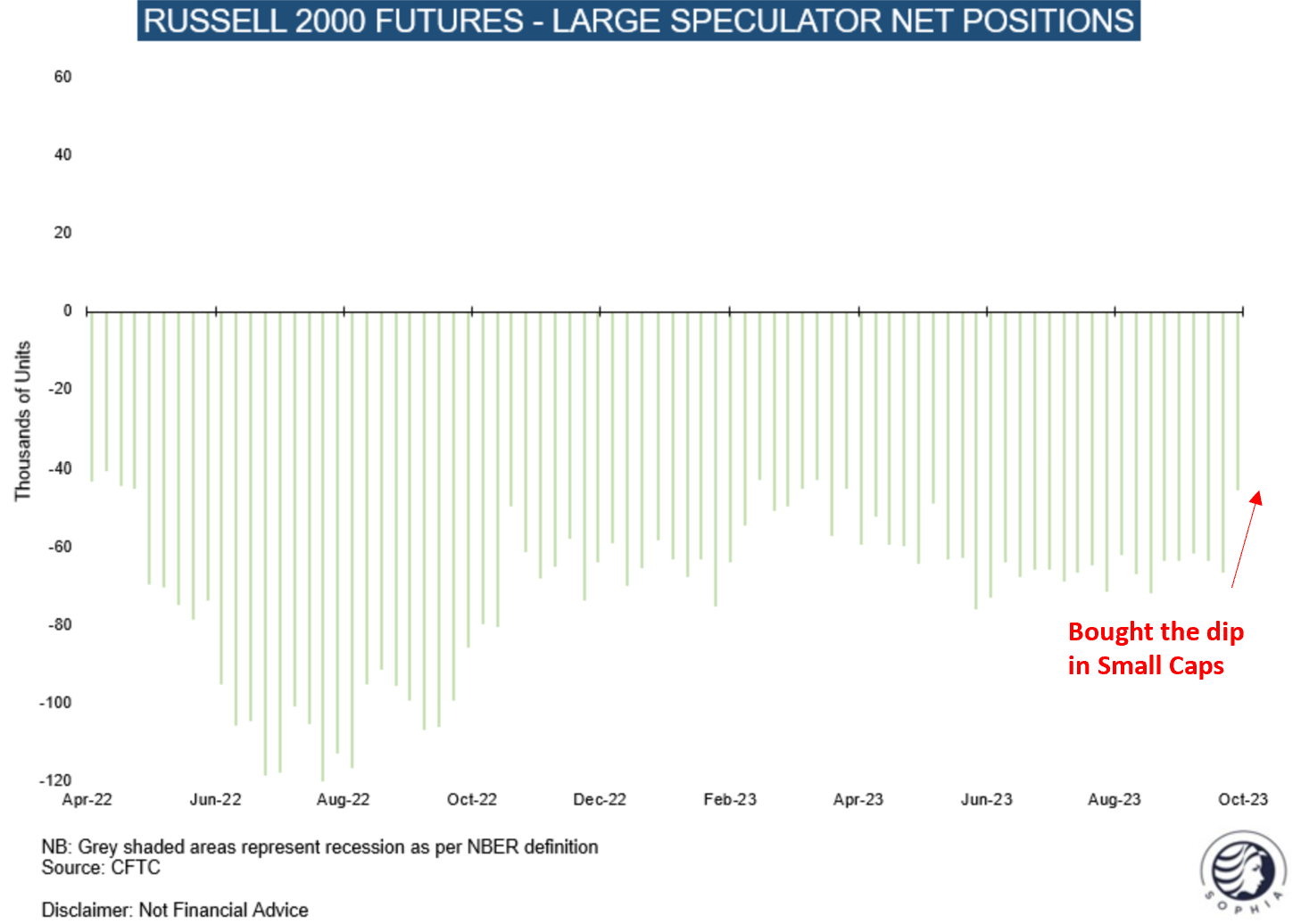

In particular, CFTC data shows large fast money accounts are reaching for the riskiest areas of the market in their buys - e.g. the Russell 2000 small cap index. This group is a critical thermometer of the state of the US economy, as small caps employ ~50% of Americans. For a durable bottom, you would want to see capitulation. Dip-buying suggests more downside ahead for this group, which is critical for the economy

Bonds

Many investors are of the view that the high in yields is in. Indeed, trading volume in the long-term bond ETF “TLT” hit a record high, which is often indicative of a change in trend. However, CFTC data continues to show enthusiastic buying in the 30-year future, instead of capitulation. Again, it is usually not a low when everyone thinks it is

Similar applies to other tenors across the curve, as well as to JP Morgan’s survey of their Treasury clients. There is just no sign of throwing in the towel

This is equally illustrated by another JP Morgan survey on both equities and bonds. People want to buy stocks, after not having wanted to all year, and they do not want to sell bond duration

So what does the most up-to-date positioning data tell us? Fast money investors are long equities and are long bonds, and getting more long as prices in either decline. No sign of capitulation, this suggests accordingly:

Despite the drawdown so far, the risk in equities appears to the downside, and in yields still to the upside. This corroborates my macroeconomic view as summarised at the start of the section - too much issuance now hurts the economy

Today’s review confirms from a positioning point of view, what I’ve spelled out in several recent posts for the real economy. The economy appears to slow down from its torrid recent growth rate. Whether it will slow so much that we see a recession, I think at this point no one can know (Reflexivity!), but it is a possibility

Conclusion: The market by definition usually does what screws the largest number of participants the most. Having missed the 1H ‘23 bull market, many investors now try to get on board for a year-end rally. This is the “Trap” from today’s post title. Instead, positioning data shows more downside ahead for both equities and bonds

To be clear, said rally into the end of the year remains entirely possible. But its odds are just much higher if markets sells off before and flushes out everyone positioned for it now

In a probabilistic world I have to acknowledge that this analysis only portrays one potential outcome. Many others are possible. This is where I could be wrong:

I could underestimate the negative positioning in the market by emphasising CFTC data. I do this as it gives a coherent view across asset classes, but other data such as prime broker equity hedge fund positioning is somewhat contradictory (see more details in this prior post)

The market is wrong in its trend breakdowns. The US economy including its small cap sector are resilient to these higher long-term Treasury bond yields and price action will revert

Perhaps most importantly, should the Middle East war extend to a much broader conflict, an entirely new playbook could get introduced. US consumption may be supported to not see the economy fail at a critical moment. The Fed would quickly become much more lenient as inflation would be a concern secondary to security

What does this mean for markets?

The following section is for professional investors only. It reflects my own views in a strictly personal capacity and is shared with other likeminded investors for the exchange of views and informational purposes only. Please see the disclaimer at the bottom for more details and always note, I may be entirely wrong and/or may change my mind at any time. This is not investment advice, please do your own due diligence

My own positioning remains the same as discussed in recent posts, all-cash since early September and batting for equity downside via puts

Please note, as some downside has already materialised and the delta on these puts has gone up a lot, I may trim or close these at any time. But for now, I am still holding on

Further, should a major flush occur, I would look to build equity long positions into it, as discussed previously. The market is moving fast now, this washout could occur any day. In particular Small Caps are getting demolished, they are due a good rebound whenever the market is ready for it

Either way, I see a major catalyst ahead next week. On Monday at 3pm EST, the US Treasury will share the amount it intends to raise in Q1 ‘24, and the following Wednesday at 8:30 EST the composition of bills vs coupons (“QRA”)

Market commentary (e.g. Morgan Stanley) expects a positive surprise. In particular, the share of bills is expected to relieve pressure off higher long-term bond yields

I think this misses many important aspects. For anyone interested in the details I recommend John Comiskey’s very good work on the topic

I find a positive surprise less likely for two reasons:

The Fed explicitly acknowledged the positive role of higher long-term yields in curbing inflation. Should the Treasury actively work against that by trying to get these yields down, it’d effectively conduct monetary policy. This is far outside their comfort zone, and further there is also no urgency to do so

As laid out today, the market is long bonds. So whatever the news, positioning favours a disappointed read…

Please keep in mind, as with any government releases, a wide error margin applies in forecasting them, and my read may be off. Should the government choose to issue much less paper than expected, it could - short term - be very positive for markets. Long term not so much. Why? Unless the deficit is cut, that paper needs to be issued another time

The release could also be front-run in the coming days and then be a sell-the-rumour/buy-the-fact event. However, again, the deficit is what it is, without a major change that overhang for risk assets seems unlikely to go away

A few more thoughts:

TIPS - I laid out the case for US TIPS in my last post and continue to find them compelling. As stated, I am still holding off on buying them as I believe nominal bonds could still have downside given their positioning. Perhaps the QRA provides a good opportunity. But either way, these are very attractive on a (to me) logical basis, and I want to deploy capital to them soon. I am looking at the 10-30yr duration as it would provide capital gains in addition to yield, should real rates come down. Obviously, should I be wrong these also come with higher risk of capital losses

Commodities - This sector faces the crosscurrents of a likely slowing US economy juxtaposed against high fiscal spending and Chinese efforts to stimulate its economy. Further, the US slowdown may be services driven as the goods economy has effectively been in a recession for some time already. I continue to think commodity and oil prices go higher over the coming decade, but as cyclical assets they should do so in ebbs and flows that may be quite uncomfortable for many investors

Bitcoin - While I have previously not liked this asset class at all (mainly because I only came to it in the aftermath of Covid-19 when it was completely overstretched and just rife with retail-fleecing scam artists), I have warmed to it recently (see here or here) as I see high odds of the endgame for what’s currently going on being more Central Bank liquidity. The virtual currency is up 30% this month

Tech - Hedge Funds are max long the “Magnificent 7”, so even with good earnings few incremental buyers are around as the last two days show. This last fortress of equities is now cracking, and until these stabilise, equities will struggle. But these companies are still the best in the world, so any major drawdown will be an opportunity to buy them for the long run. Other areas of Tech including e-commerce and payments are extremely oversold, and like Small Caps, are likely to rebound hard whenever the time is right. For a durable rebound in either we may have to wait until January though, as tax loss harvesting may weigh on these beaten down areas until then

Thank you for reading my work, it makes my day. It is free, so if you find it useful, please share it!

DISCLAIMER:

The information contained in the material on this website article is for professional investors only and for educational purposes only. It reflects only the views of its author (Florian Kronawitter) in a strictly personal capacity and do not reflect the views of White Square Capital LLP and/or Sophia Group LLP. This website article is only for information purposes, and it is not intended to be, nor should it be construed or used as, investment, tax or legal advice, any recommendation or opinion regarding the appropriateness or suitability of any investment or strategy, or an offer to sell, or a solicitation of an offer to buy, an interest in any security, including an interest in any private fund or account or any other private fund or account advised by White Square Capital LLP, Sophia Group LLP or any of its affiliates. Nothing on this website article should be taken as a recommendation or endorsement of a particular investment, adviser or other service or product or to any material submitted by third parties or linked to from this website. Nor should anything on this website article be taken as an invitation or inducement to engage in investment activities. In addition, we do not offer any advice regarding the nature, potential value or suitability of any particular investment, security or investment strategy and the information provided is not tailored to any individual requirements.

The content of this website article does not constitute investment advice and you should not rely on any material on this website article to make (or refrain from making) any decision or take (or refrain from taking) any action.

The investments and services mentioned on this article website may not be suitable for you. If advice is required you should contact your own Independent Financial Adviser.

The information in this article website is intended to inform and educate readers and the wider community. No representation is made that any of the views and opinions expressed by the author will be achieved, in whole or in part. This information is as of the date indicated, is not complete and is subject to change. Certain information has been provided by and/or is based on third party sources and, although believed to be reliable, has not been independently verified. The author is not responsible for errors or omissions from these sources. No representation is made with respect to the accuracy, completeness or timeliness of information and the author assumes no obligation to update or otherwise revise such information. At the time of writing, the author, or a family member of the author, may hold a significant long or short financial interest in any of securities, issuers and/or sectors discussed. This should not be taken as a recommendation by the author to invest (or refrain from investing) in any securities, issuers and/or sectors, and the author may trade in and out of this position without notice.

One of the best pieces of work I have read lately.

Great to add your perspective into my thinking.

Thanks for sharing.

Hi Florian. Silly question, I'm sure, but I cannot find those charts on the CFTC site, so I assume that you rendered the charts based on the data the Trading Commission provides. Is that so?

Thank you for the article!